Every day, companies somewhere in the world are making big decisions - buying a competitor, merging with a partner, or acquiring a startup to get ahead in the market. These are mergers and acquisitions, or M&A for short, and they are one of the most powerful strategies a business can use to grow.

But M&A is not a single thing. There are many types of deals, each with its own structure, purpose, and set of challenges. A tech giant buying a smaller startup is a very different deal from two banks merging, even though both are technically "M&A." Getting the type wrong - or not understanding what you are getting into - can cost a company a significant amount of money, time, and reputation.

This guide breaks down every major type of merger and acquisition in plain terms. You will learn what each one is, see real-world examples, understand the challenges that come with each, and find out how the right tools (like a virtual data room) can make the whole process cleaner and more controlled.

Whether you are an M&A professional, a business owner exploring your options, or someone simply trying to understand what these terms mean - this guide is for you.

Need a secure space to manage your deal documents? Try Ellty for free - no setup fees, no surprise costs. |

What is a business merger?

A business merger is when two separate companies come together to form one new entity. In most cases, both companies agree to the deal. Neither company fully absorbs the other - instead, they combine their resources, teams, and operations to create something bigger.

Mergers usually happen when two companies believe they are stronger together than they are apart. They might share customers, operate in similar industries, or have skills that complement each other. The goal is usually to grow faster, reduce costs, or gain a stronger position in the market.

A good example is the merger of Exxon and Mobil in 1999. Two oil giants came together to form ExxonMobil, one of the largest companies in the world. Neither company disappeared - they merged into a new, more powerful combined entity.

In a merger, the process involves a lot of moving parts - legal due diligence, financial reviews, employee transitions, and document sharing between multiple parties. This is where having a secure, organized document environment becomes critical.

What is a business acquisition?

An acquisition is when one company buys another. The buying company (the acquirer) takes control of the target company. Unlike a merger, one side clearly takes ownership. The acquired company may continue to operate under its own name, or it may be absorbed completely into the acquirer.

Acquisitions can be friendly, where the target company agrees to be bought or hostile, where the acquirer pursues the deal even if the target's board resists.

One well-known example is Facebook's acquisition of Instagram in 2012 for $1 billion. Instagram continued to operate as its own platform, but Facebook controlled the business. Today, it operates under Meta.

Acquisitions require significant document exchange between the buyer and the seller, from financial statements and contracts to employee records and IP agreements. Managing this securely, without leaks or unauthorized access, is one of the biggest operational challenges in any deal.

Ellty virtual data room keeps all your deal documents organized, access-controlled, and fully auditable - from first look to final close. |

Different types of mergers and acquisitions with examples

Not all M&A deals look the same. The type of deal depends on the relationship between the two companies, the goal of the transaction, and the industry involved. Here are the most important types you need to know.

1. Horizontal merger or acquisition

This happens when two companies in the same industry, at the same stage of the supply chain, combine. They are direct competitors or operate in the same market.

The primary goal is usually to gain more market share, reduce competition, or achieve economies of scale - meaning the combined company can produce at lower costs than either company could alone.

Example: The merger of T-Mobile and Sprint in 2020. Both were wireless carriers competing in the same space. After the deal, the combined company became a stronger competitor against AT&T and Verizon.

Horizontal deals attract the most regulatory attention because they reduce competition. Antitrust regulators look closely at whether the combined company will have too much market power.

2. Vertical merger or acquisition

A vertical deal happens between companies at different stages of the same supply chain. One company might be a supplier, and the other might be a manufacturer or distributor. They are not direct competitors, they are part of the same value chain.

The goal is usually to control more of the supply chain, reduce dependency on third parties, or cut costs by bringing operations in-house.

Example: Amazon's acquisition of Whole Foods in 2017. Amazon was a retailer and tech company. Whole Foods was a physical grocery chain - a different part of the consumer goods chain. Together, Amazon gained direct access to physical retail and supply chain capabilities.

3. Conglomerate merger

A conglomerate happens when two companies from completely different industries merge. They have no direct relationship - different products, different customers, and different markets. These deals are usually driven by diversification, spreading risk across multiple businesses.

Example: Berkshire Hathaway's many acquisitions over the decades. Warren Buffett's holding company owns businesses ranging from insurance (GEICO) to candy (See's Candies) to railroads (BNSF). These have little to do with each other - that is the point.

Conglomerate deals are complex because the acquirer must manage businesses it may not have deep expertise in. Post-merger integration across very different industries is a common challenge.

4. Market extension merger

Two companies selling the same product or service, but in different geographic markets, combine in a market extension deal. The goal is to enter new markets quickly, without building from scratch.

Example: RBC's acquisition of City National Bank in 2015. Royal Bank of Canada wanted to expand its presence in the US market. City National, based in California, gave it that foothold quickly.

Market extension deals are less about competition and more about expansion. But they do require integrating teams and operations that may have very different cultures and processes.

5. Product extension merger (congeneric merger)

Also called a congeneric merger, this involves two companies in related industries that serve similar customer bases, but with different products. The idea is to offer customers a broader range of products under one company.

Example: Citigroup's formation through the merger of Citicorp (banking) and Travelers Group (insurance and financial services) in 1998. Both served financial customers, but with different products.

6. Acqui-hire

An acqui-hire (acquisition + hire) is when a company acquires another primarily to get its talent - the team, engineers, or specialists - rather than its products or revenue. The acquired company's product may be shut down after the deal.

This type of deal is very common in the technology industry, especially with early-stage startups.

Example: Google has been known to acqui-hire small AI and engineering teams to strengthen its own product teams, often quietly integrating the team while winding down the acquired product.

7. Reverse merger

In a reverse merger, a private company acquires a publicly listed company, usually a shell company with no active business. This allows the private company to become publicly listed without going through the lengthy and expensive process of an IPO.

Example: Ted Turner merged his Turner Broadcasting into a public shell in the 1970s - giving him access to public capital markets without a traditional IPO.

8. Asset acquisition

Instead of buying the whole company, the acquirer only purchases specific assets - intellectual property, a particular product line, equipment, or real estate. The legal entity of the target company may continue to exist.

Asset acquisitions are popular in bankruptcy cases, where buyers want only the valuable parts of a distressed company.

Example: When Sears went bankrupt in 2018, buyers acquired specific store leases and assets rather than the whole company.

9. Stock acquisition

Here, the acquirer buys the majority of shares of the target company, giving them ownership and control. Unlike an asset acquisition, the entire legal entity, including its liabilities, transfers to the buyer.

This is one of the most common acquisition structures for larger deals.

10. Management buyout (MBO)

An MBO is when a company's own management team buys the business from its current owners, often with support from private equity. The management team believes they can run the business better as owners, and the current owners get a clean exit.

Example: Dell Technologies went private through a management buyout in 2013. Michael Dell partnered with Silver Lake Partners to take the company off the public markets and restructure it.

Running a management buyout or acquisition? Ellty data room gives your team full control over document access, NDA gating, and deal-room security - starting from just $69/month. |

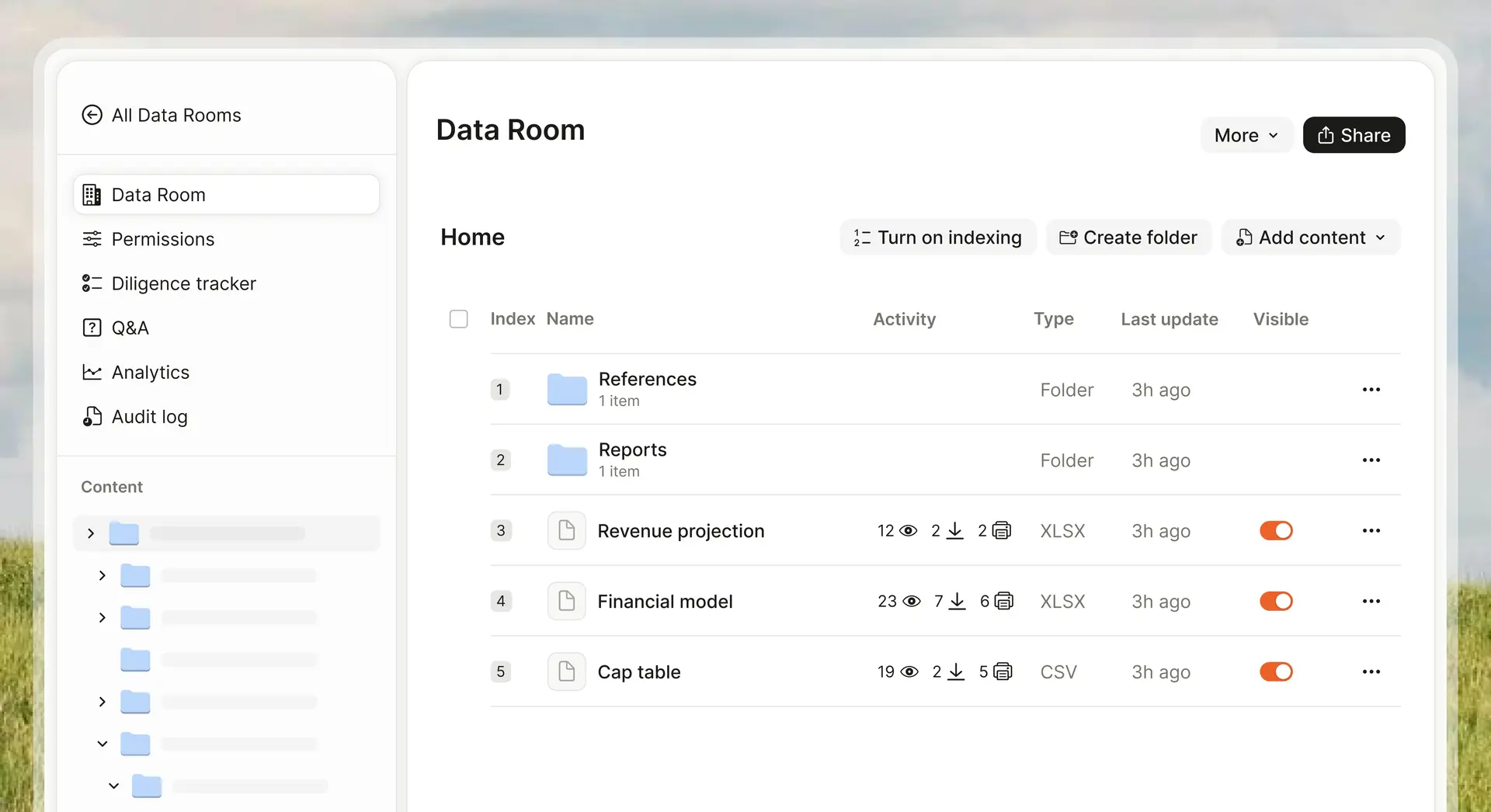

How a virtual data room helps in M&A and why Ellty stands out

No matter which type of M&A deal you are running, one thing is always true: a large amount of sensitive information needs to change hands. Financial statements, contracts, IP filings, employee records, regulatory documents - all of this has to be shared with the right people, in a controlled and secure way.

This is exactly what a virtual data room (VDR) is designed for. And Ellty is built specifically for teams that need serious document control without the complexity and cost of traditional VDR platforms.

What Ellty does for M&A teams

- Access controls: You decide who sees what. Ellty lets you set granular permissions so the legal team sees different documents from the finance team, and buyers only access what they are permitted to review.

- NDA gating: Before anyone views your documents, they can be required to accept an NDA right inside the platform. No back-and-forth emails, no unsigned agreements slipping through.

- Dynamic watermarking: Every document is watermarked with the viewer's details. If a document leaks, you can trace exactly who it came from.

- Real-time activity tracking: You can see who is opening documents, how long they are spending on each file, and which sections are getting the most attention - giving you intelligence you can use in negotiations.

- Full audit logs: Every action taken inside the data room is recorded. This is critical for compliance, dispute resolution, and post-deal review.

- eSignatures: Close faster by collecting signatures inside the same platform, without switching to a separate tool.

Ellty pricing model - transparent from day one

One of the biggest frustrations with legacy VDR platforms is the pricing. Many charge per user, per page, or require lengthy enterprise negotiations before you even get a quote. Ellty does none of that.

- Free ($0/month): Document tracking, real-time analytics, and secure sharing. Great for early conversations and exploratory due diligence.

- Standard ($69/month): Unlimited documents, advanced analytics, eSignatures, custom branding, and full data room features. Ideal for smaller deals and ongoing investor communication.

- Room ($149/month): Granular permissions, NDA gating, dynamic watermarking, and restricted visitor access. This is the tier purpose-built for controlled due diligence.

- Room Plus ($349/month): Group visitor permissions, full audit logs, and support for up to 4,000 assets. Built for larger, multi-party deals with complex access requirements.

You pick a plan, get set up quickly, and know exactly what you are paying, whether you are sharing documents with 3 people or 300. No hidden fees, no per-user charges, and no surprises.

Common integration challenges by deal type

Deal type | Primary goal | Top integration challenge(s) |

|---|---|---|

Horizontal Same industry, same stage | Market share, reduced competition | Redundant teams and roles, Employee attrition, Antitrust scrutiny |

Vertical Different supply chain stages | Supply chain control, cost reduction | Mismatched operational cultures, System and workflow alignment |

Conglomerate Unrelated industries | Diversification, risk spreading | Managing unfamiliar businesses, Lack of operational expertise, Slow decision-making |

Market extension Same product, new geography | Enter new markets fast | Local regulation and compliance, Cultural adaptation |

Product extension Related products, same customers | Broaden product portfolio | Cross-sell execution, Platform and system integration |

Acqui-hire Talent-focused acquisition | Acquire a specific team or skill set | Retaining key talent post-close, Sunsetting acquired products |

Reverse merger Private goes public via shell | Public listing without an IPO | Regulatory and compliance catch-up, Investor credibility |

Asset acquisition Buying specific assets only | Targeted value, avoid liabilities | Asset valuation disputes, Transferring contracts and IP |

Stock acquisition Buying majority shares | Full ownership and control | Inheriting unknown liabilities, Shareholder approval and negotiations |

Management buyout Management buys the business | Owner exit, insider-led ownership | Debt servicing pressure, Balancing growth vs. repayment |

Closing the deal is only half the job. The real test comes after signing, integrating two businesses into one. Each type of M&A deal brings its own specific challenges.

- Horizontal deals: Removing redundancy without damaging morale. When two companies doing the same thing merge, overlapping teams, tools, and processes need to be consolidated. This is often where employee tension and attrition spike.

- Vertical deals: Aligning completely different operational cultures. A tech company acquiring a logistics firm will find that the two organizations have very little in common in how they work day to day.

- Conglomerate deals: Managing across unrelated industries. The leadership team of the acquirer may not understand the business they just bought, which leads to poor decisions and slow integration.

- Market extension deals: Localizing and adapting. Entering a new geography means navigating different regulations, customer expectations, and sometimes entirely different languages or currencies.

- Product extension deals: Cross-selling and system integration. The promise of these deals is offering more to existing customers, but that only works if the products, platforms, and sales teams actually work together.

- Acqui-hires: Retention. The whole point of the deal was the talent. If key people leave shortly after the deal closes, the entire investment has failed.

- Management buyouts: Financing pressure. MBOs are often leveraged, meaning debt-financed. The new owner-operators must generate enough cash flow to service that debt while also running the business effectively.

Across all deal types, one integration challenge is universal: data and document management. During integration, information needs to flow between teams, systems, and sometimes between companies that are still separating their operations. A structured, permission-controlled environment removes a significant amount of that friction.

How to choose the right type of acquisition for your strategy

Choosing the right M&A structure is not just a legal or financial decision, it is a strategic one. The wrong deal type can result in paying too much, integrating too little, or creating regulatory problems you did not anticipate.

Here are the questions you should be asking before deciding on a deal type:

- What is the primary goal? If the goal is market share, a horizontal deal makes sense. If the goal is supply chain control, go vertical. If the goal is diversification, consider a conglomerate structure. If the goal is talent, an acqui-hire is often the most efficient path.

- How related are the businesses? The more different the two companies are, the more complex integration will be. This does not make the deal wrong - but it means you need more planning and more realistic timelines.

- What is the financial structure? Are you buying shares or assets? An asset acquisition gives you more control over what liabilities you take on. A stock acquisition is simpler but comes with the full legal entity, including its history and obligations.

- What are the regulatory considerations? Horizontal deals in concentrated markets will face the most scrutiny. Knowing this upfront shapes how you structure and time the deal.

- What does post-deal success look like? Before signing, define what a successful integration looks like - customer retention, revenue targets, team stability, technology migration. This informs which deal type and structure serves you best.

There is no universally "right" M&A type. The best choice depends entirely on your specific goals, industry, resources, and appetite for integration complexity.

Before your next deal, get your documents organized and your team aligned. Ellty data room gives you a clean, secure foundation from the first conversation to final close. |

Regulatory and antitrust considerations across M&A types

Every M&A deal has a regulatory dimension. Depending on the type of deal, the industries involved, and the size of the transaction, you may need approval from government authorities before the deal can close.

Horizontal deals face the most scrutiny

Because horizontal mergers reduce competition in a market, antitrust regulators pay close attention. In the US, the Federal Trade Commission (FTC) and the Department of Justice (DOJ) review deals that could harm competition. In the EU, the European Commission handles similar reviews.

Regulators will assess market concentration - essentially asking: if these two companies combine, will consumers have fewer choices and face higher prices? If the answer is yes, the deal may be blocked or only approved with conditions, such as requiring the companies to divest certain assets.

Vertical and conglomerate deals

These deals historically faced less scrutiny, but that has changed in recent years. Regulators are now more alert to vertical deals that could allow a company to lock out competitors - for instance, a supplier that also owns a retailer might give its own retail arm preferential terms, hurting competing retailers.

Conglomerate deals are generally the least likely to face antitrust issues, since the companies operate in unrelated markets. But they can still attract scrutiny if the acquirer is a dominant player in its own industry.

Global deals and multi-jurisdiction filings

If the deal involves companies operating in multiple countries, regulatory filings may be required in each jurisdiction. A deal approved in the US may still face a separate review in the EU, UK, or other markets. This adds time and cost to the process and creates more document management obligations.

Hart-Scott-Rodino (HSR) filings

In the US, transactions above a certain size threshold require a premerger notification under the Hart-Scott-Rodino Act. This gives regulators time to review the deal before it closes. Filing this notification requires detailed financial and business information about both companies - all of which needs to be prepared, reviewed, and shared securely.

A well-organized data room makes regulatory preparation significantly easier. When all the relevant documents are already structured, access-controlled, and audit-logged, pulling together regulatory submissions becomes a much faster process.

Frequently asked questions (FAQs)

What is the difference between a merger and an acquisition?

A merger is when two companies combine to form a new entity, both parties are generally equal partners in the process. An acquisition is when one company buys and takes control of another. In practice, the terms are often used together (M&A), but legally they are distinct structures.

Which type of M&A deal is the most common?

Horizontal acquisitions are among the most common, particularly in industries like technology, financial services, and healthcare. They are popular because they directly increase market share and reduce competition. That said, the most common type varies by industry and economic cycle.

Why do M&A deals fail?

The most common reasons include poor cultural fit, overpaying for the target, unrealistic integration timelines, and failure to retain key talent. Research consistently shows that a large proportion of M&A deals do not deliver the expected value, often because integration planning is underestimated.

What is due diligence in M&A?

Due diligence is the process of thoroughly reviewing a target company before completing a deal. This includes financial, legal, operational, and compliance reviews. The buyer wants to confirm everything the seller has represented about the business is accurate. This process generates a large volume of sensitive documents that need to be shared securely between the parties.

What is a virtual data room and why do M&A deals need one?

A virtual data room (VDR) is a secure online space where deal documents are stored, organized, and shared with authorized parties. In M&A, a VDR is used during due diligence to share financial records, contracts, and legal documents with buyers, advisors, and regulators - all with controlled access and full activity tracking. Ellty is a modern VDR platform built to make this process simpler and more affordable.

How long does an M&A deal typically take?

It varies widely by deal type and complexity. Smaller deals can close in 3 to 6 months. Large, cross-border transactions with regulatory requirements can take 12 to 24 months or longer. Due diligence and regulatory review are typically the most time-consuming phases.

Do all M&A deals require regulatory approval?

Not all deals require formal regulatory approval, but most large transactions do. In the US, deals above the HSR threshold require a premerger filing. Cross-border deals may need approval in multiple jurisdictions. Even deals below formal thresholds may attract scrutiny if they significantly affect competition in a specific market.

Final thoughts

M&A is one of the most consequential things a business can do. The right deal, done well, can transform a company, opening new markets, strengthening competitive position, and creating value that would take years to build organically. The wrong deal, or the right deal executed poorly, can do the opposite.

Understanding the type of deal you are pursuing is the first step to getting it right. Horizontal, vertical, conglomerate, acqui-hire, asset acquisition - each one has its own logic, its own risks, and its own integration demands. The companies that succeed in M&A are the ones that go in with their eyes open.

The operational side of M&A - managing documents, running due diligence, controlling who sees what, and maintaining a clean audit trail - is where deals often quietly fall apart. Information leaks at the wrong moment, documents get lost in email threads, access is not revoked after a potential buyer drops out. These are solvable problems.

Ellty is designed to solve them. From early-stage document sharing with potential partners to full due diligence data rooms for complex acquisitions, Ellty gives your deal team a secure, organized, and trackable environment for every stage of the process. Transparent pricing, no per-user fees, and a platform that your team can actually get up and running without weeks of onboarding.

Ready to run a cleaner deal? Start your free Ellty data room today and see why deal teams choose Ellty for secure, simple, and professional document management. |

Author

Anika Tabassum Nionta is a Content Manager at Ellty, where she writes about secure document sharing, virtual data rooms, M&A, due diligence, fundraising, and sales enablement. With over 6 years of writing experience, she helps professionals understand how to share confidential documents securely, track engagement, and manage deals more effectively. Anika holds both a BA and MA in English from Dhaka University. Outside of work, she enjoys reading, exploring new cafes in Dhaka, and connecting with entrepreneurs and dealmakers in her community.