Buying or merging with another company is one of the biggest decisions a business can make. It involves a lot of money, a lot of people, and a lot of moving parts. Done right, an M&A deal can open new markets, bring in new talent, and accelerate growth in ways that would take years to achieve organically. Done poorly, it can cost more than just money.

Yet for something so significant, the M&A process is often misunderstood. People see the headline announcement - "Company A acquires Company B for $2 billion" - but the real story happens long before and after that press release. There are months of preparation, analysis, negotiations, and document reviews that most people never see.

This guide breaks down the full M&A process in plain terms. Whether you are a business owner considering a sale, a finance professional working on a deal, or simply someone trying to understand how these transactions work, this guide covers everything you need to know - from the first strategic discussion to the final closing.

We will also cover where technology fits in, and specifically why a virtual data room (VDR) like Ellty is no longer optional if you want a smooth, secure deal process.

Running an M&A deal? Start your free Ellty data room today and share documents securely from day one. No per-user fees, no surprise charges. |

Overview of the M&A process

M&A stands for mergers and acquisitions. A merger is when two companies combine to form one new entity. An acquisition is when one company buys another. In practice, the word 'M&A' is used loosely to describe both.

These transactions happen across all industries and at all scales. A tech startup getting acquired by a larger platform. A private equity firm buying a regional manufacturing business. Two mid-sized competitors merging to compete better in a crowded market. The structure varies, but the core process follows a similar path.

At a high level, M&A involves:

- Identifying the right target or buyer

- Running financial and legal due diligence

- Negotiating and structuring the deal

- Finalizing agreements and regulatory approvals

- Closing, and then integrating the two businesses

Each of these phases requires careful coordination, a lot of document sharing, and trust between parties. That last point is why secure document management, through a platform like Ellty, becomes critical as soon as serious conversations begin.

The 10-step M&A process

Let us walk through the full process step by step. These steps are not always perfectly linear. Some happen in parallel, and some may loop back, but this is the general sequence most deals follow.

Step 1: Define the strategy

Every M&A deal starts with a question: why are we doing this? A company might want to acquire a competitor, enter a new geography, gain access to technology, or simply grow faster than organic growth allows. Before reaching out to anyone, the acquiring company needs to define what success looks like.

Step 2: Identify potential targets

Once the strategy is clear, the team creates a list of potential targets. This often involves investment bankers, advisors, or internal strategy teams. The list gets filtered down based on size, fit, geography, and other criteria.

Step 3: Initial outreach and NDA

When a shortlist is ready, the acquiring company makes discreet contact with the target. If there is mutual interest, both parties sign a Non-Disclosure Agreement (NDA) before sharing any sensitive information. This is where a platform like Ellty becomes useful immediately. You can gate access to documents behind an NDA directly inside the data room.

Tip: With Ellty NDA gating feature, you can require buyers or investors to sign an NDA before they can view any document in your data room. No more chasing signatures or tracking who has seen what. |

Step 4: Preliminary valuation and Letter of Intent (LOI)

The buyer reviews basic financial information to form an initial view on valuation. If both sides are aligned on range, they proceed to a Letter of Intent (LOI) - a non-binding document that outlines the proposed deal structure, price range, and key terms.

Step 5: Due diligence

This is the most document-heavy phase of any M&A deal. The buyer's team - including lawyers, accountants, and operational experts - reviews everything: financials, contracts, employee agreements, intellectual property, pending litigation, customer lists, and more.

This is exactly why a virtual data room exists. All documents are uploaded to a secure, organized folder structure. Different reviewers get different levels of access. Every action is tracked. No sensitive file gets emailed around.

Step 6: Negotiation and deal structure

Based on due diligence findings, the buyer may revise the offer. Price, payment terms (cash vs. equity vs. earnout), warranties, indemnities, and other conditions all get negotiated in detail. This stage can take weeks or months.

Step 7: Definitive agreements

Once the main terms are agreed, the legal teams draft the final binding contracts. The most important of these is the Share Purchase Agreement (SPA) or Asset Purchase Agreement (APA), depending on the deal structure.

Step 8: Regulatory and shareholder approvals

Depending on the size of the deal and the industry, regulatory approvals may be required. Antitrust authorities in various jurisdictions may need to review the transaction. Shareholders may also need to vote.

Step 9: Closing

Once all conditions are met, the deal closes. Money changes hands, ownership transfers, and the transaction is legally complete. There is usually a closing checklist of dozens of items that all need to be ticked off.

Step 10: Post-merger integration (PMI)

The deal may be done, but the work is not. Integrating two businesses is often harder than buying one. Systems, teams, processes, and cultures all need to be aligned. A poorly managed integration can destroy the value that the deal was supposed to create.

Structuring an M&A deal

How a deal is structured affects everything - taxes, risk, how the seller gets paid, and how the buyer assumes (or avoids) liabilities. There are a few common structures:

Stock purchase

The buyer purchases the shares of the target company. The buyer gets everything - assets and liabilities. This is simpler to execute but carries more risk for the buyer, as they inherit any unknown liabilities.

Asset purchase

The buyer picks and chooses specific assets and liabilities to acquire. More complex legally, but it gives the buyer more control over what they are taking on. Common in smaller deals or when the target has known liability issues.

Merger

Two companies combine to form a new entity, or one is absorbed into the other. Mergers require more regulatory scrutiny and shareholder approvals, but can be structured tax-efficiently.

Payment types

Deals can be paid in cash, stock in the acquiring company, an earnout (payments tied to future performance), or a combination. Earnouts are often used when there is a gap between what the buyer wants to pay and what the seller believes the business is worth.

The structure ultimately depends on the goals of both parties, tax implications, and how much risk each side is willing to carry. Legal and financial advisors play a central role in this stage.

Sharing deal structure documents with advisors and investors? Use Ellty granular permission controls to give each party access only to what they need. Try Ellty free today. |

Rival bidders in M&A

Not all M&A deals are friendly one-on-one negotiations. Sometimes there are multiple buyers competing for the same target. This happens most often in formal sale processes run by investment banks, where the seller runs a structured auction to maximize price.

In a competitive bidding process:

- Multiple buyers receive the same initial information package (called a Confidential Information Memorandum, or CIM)

- Each bidder submits an initial offer, and a shortlist is selected

- Shortlisted bidders get deeper access to due diligence materials

- Final bids are submitted, and the seller selects the preferred buyer

- Exclusivity is granted to the winning bidder to finalize the deal

Rival bidders create pressure that typically drives up the price. But they also create complexity, especially around data room management. The seller needs to control which bidder sees what, ensure no sensitive information is shared prematurely, and track all activity carefully.

This is another place where a well-organized virtual data room is essential. Ellty Room and Room Plus plans include group visitor permissions, meaning you can create separate access groups for different bidders - each seeing exactly what you want them to see, nothing more.

Strategic vs financial buyers in M&A

Strategic Buyer | Financial Buyer | |

|---|---|---|

Who they are | A company in the same or adjacent industry | A private equity firm or investment fund |

Primary goal | Grow market share, acquire technology, eliminate competition, or enter new markets | Generate financial returns by buying, improving, and selling the business |

How they value the business | Standalone value plus synergy premium - often willing to pay more | Based purely on cash flow, margins, and debt capacity - very model-driven |

Due diligence focus | Cultural fit, team retention, operational overlap, and integration feasibility | Financial performance, revenue quality, cost structure, and growth potential |

What they scrutinize most | How the two businesses will work together after closing | Whether the business can stand alone and grow without the seller |

Speed of due diligence | Can move faster if the strategic fit is obvious | Usually thorough and methodical, driven by investment committee timelines |

Post-deal approach | Integrates the target into its existing operations | Keeps the business mostly separate, installs a management team, focuses on growth |

Typical holding period | Long-term, often permanent | 3 to 7 years, then exits via sale or IPO |

Key concern | Will this acquisition actually create the synergies we projected? | Can we hit our return targets and exit at a good multiple? |

Impact on employees | More likely to see role changes, redundancies, or restructuring post-merger | Usually retains the management team and incentivizes them with equity |

Understanding who is buying matters, because it shapes how the deal is valued, what the buyer cares about during due diligence, and what happens after closing.

Strategic buyers

A strategic buyer is typically a company in the same or adjacent industry that sees operational or competitive value in the acquisition. They are buying to grow market share, acquire talent or technology, eliminate a competitor, or enter a new segment.

Strategic buyers often pay higher prices because they factor in synergies - the additional value created when two businesses combine. For example, a company that acquires a competitor can cut duplicated costs and grow revenue faster together than separately.

They care deeply about cultural fit, team retention, and how the target fits into their existing operations.

Financial buyers

Financial buyers - most commonly private equity firms - are buying for financial returns. They typically buy a business, improve its operations and financials over a 3-7 year period, and then sell it for a profit through a trade sale or IPO.

Financial buyers are highly analytical. They focus on cash flow, margins, growth rates, and debt capacity. They are less interested in synergies and more interested in whether the business can stand alone and grow.

Due diligence from financial buyers tends to be extremely thorough, with a lot of attention on detailed financial models, management quality, and market positioning.

Whether you are dealing with a strategic or financial buyer, both will conduct rigorous document reviews. Having everything organized and accessible in a single data room shows professionalism and can speed up the process significantly. |

Analyzing mergers and acquisitions

Before any deal moves forward, both sides do significant analysis. Here are the main frameworks and methods used:

Valuation analysis

The most fundamental question in any type of M&A deal is: what is this business worth? Common valuation methods include:

- DCF (Discounted Cash Flow): Projects future cash flows and discounts them back to present value

- Comparable company analysis: Looks at how similar businesses are valued in the public markets

- Precedent transaction analysis: Looks at what similar businesses sold for in past M&A deals

- Asset-based valuation: Values the company based on its underlying assets, used for asset-heavy businesses

Synergy analysis

For strategic deals, both revenue synergies (selling more together) and cost synergies (cutting duplicated expenses) are estimated. These numbers are often used to justify paying a premium above the standalone valuation.

Risk analysis

Due diligence is essentially a structured risk assessment. What are the known risks? What could go wrong post-acquisition? Legal risks, customer concentration, key person dependencies, pending lawsuits - all of these are evaluated carefully.

Integration planning

The best acquirers think about integration before the deal closes. How will the two teams work together? Which systems will be kept? Who makes which decisions? Deals that do not plan for integration often struggle in the months that follow closing.

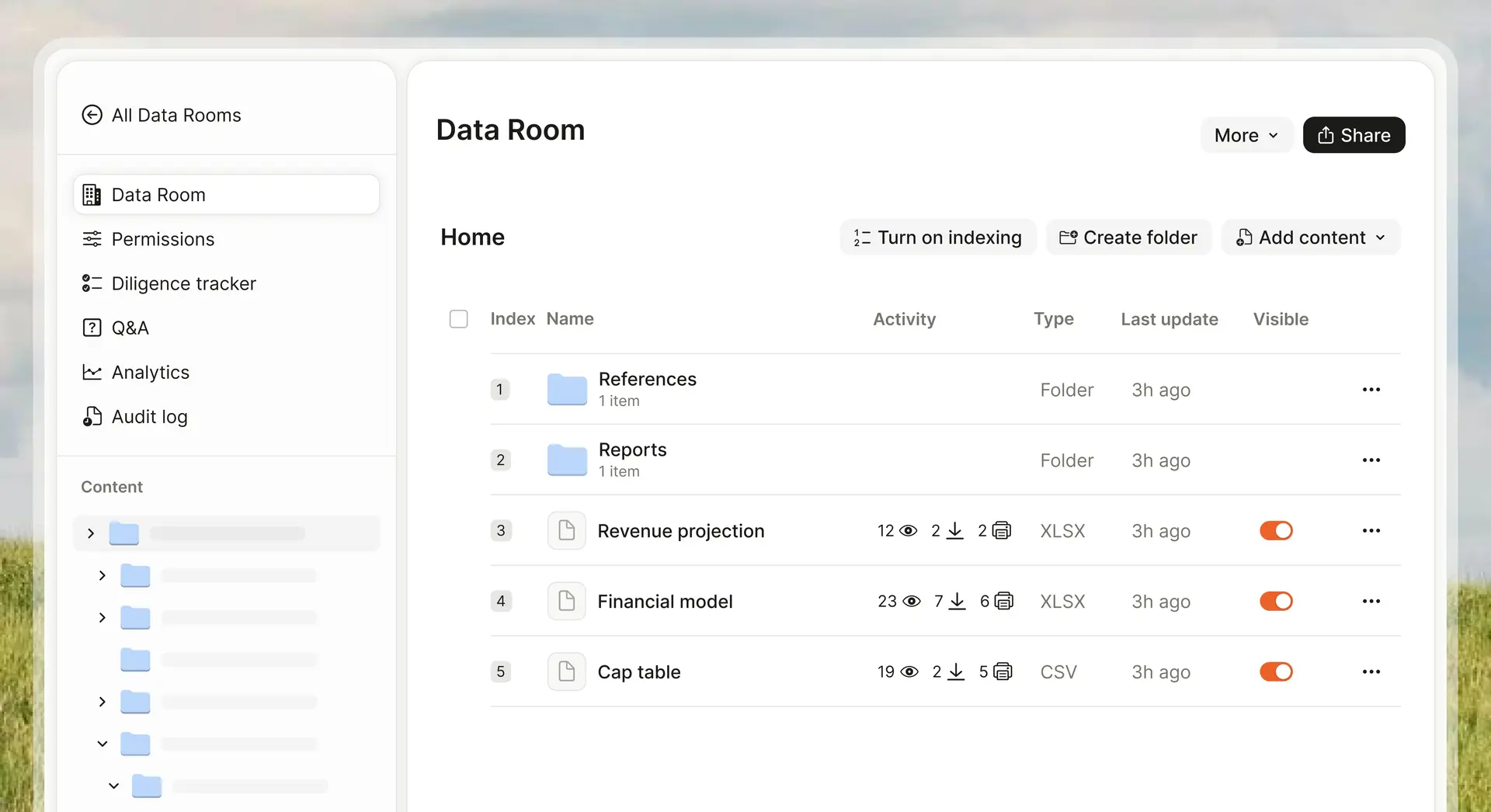

How a virtual data room helps M&A and why Ellty is the right choice

A virtual data room (VDR) is a secure online space where deal-related documents are stored, shared, and managed. Before VDRs existed, due diligence was done in physical rooms. People flew in, reviewed printed documents, and could not take anything with them. Today, all of that happens digitally.

But not all VDRs are equal. Legacy enterprise platforms are often overpriced, slow to set up, and designed for very large corporations with IT teams. For most deal teams, especially at the mid-market level, they are overkill.

That is where Ellty changes the equation.

What Ellty does

Ellty is a secure document sharing and analytics platform with full data room functionality. It is built for anyone who needs to share sensitive documents in a controlled, trackable way, whether you are running an M&A process, raising a funding round, or managing a property transaction.

- Access controls: Decide exactly who sees what. No accidental sharing, no forwarded documents reaching the wrong person.

- Real-time activity tracking: See who opened which document, how long they spent on it, and what they downloaded.

- NDA gating: Require visitors to sign an NDA before they can access any document in the room.

- Dynamic watermarking: Documents are watermarked with the viewer's name and email, discouraging unauthorized sharing.

- Audit trails: Every action is logged, giving you a clean record for compliance and accountability.

- eSignatures: Included in the Standard plan and above, so you can sign documents without switching tools.

Ellty pricing - simple and transparent

One of the biggest frustrations with legacy VDR platforms is pricing. You get a quote, negotiate for weeks, and then get hit with per-user fees and per-page charges that nobody warned you about.

Ellty works differently. Flat plans, no hidden charges, no per-user fees:

- Free - $0/month: Document tracking, real-time analytics, and secure sharing. A good starting point if you are in early conversations and want to see who is opening what.

- Standard - $69/month: Unlimited documents, advanced analytics, eSignatures, custom branding, and data room features. Works well for smaller deals and ongoing client or investor communication.

- Room - $149/month: Granular permissions, NDA gating, dynamic watermarking, and restricted visitor access. Everything you need to run a controlled due diligence process.

- Room Plus - $349/month: Group visitor permissions, full audit logs, and support for up to 4,000 assets per data room. Built for heavier document loads and multi-party deals with multiple reviewer groups.

Whether you are sharing documents with 3 people or 30, the price stays the same. For anyone who needs a professional data room without an enterprise contract, Ellty is the place to start.

Frequently asked questions (FAQs)

What is the difference between a merger and an acquisition?

A merger is when two companies agree to combine and form a new, joint entity. An acquisition is when one company buys another and takes control. In practice, many acquisitions are described as mergers for public relations purposes, even when one company is clearly buying the other.

How long does an M&A process take?

It depends on the complexity of the deal. Smaller transactions can close in 3-6 months. Larger, cross-border deals that require regulatory approvals can take 12-18 months or longer. Due diligence alone can take anywhere from a few weeks to several months.

What is due diligence in M&A?

Due diligence is the process of verifying everything the seller has told the buyer. It covers financials, legal matters, contracts, intellectual property, employees, operations, and more. The goal is to uncover any risks or issues before the deal closes, so the buyer knows exactly what they are getting.

What does a virtual data room do in M&A?

A virtual data room is a secure online platform where all deal documents are stored and shared during due diligence. It allows the seller to control who accesses what, track all document activity, and manage multiple bidders or reviewers in a structured way. It replaces the old practice of physical data rooms and scattered email chains.

What is an LOI in M&A?

An LOI, or Letter of Intent, is a non-binding document that outlines the key terms of a proposed deal - including the indicative price, deal structure, and any conditions. It signals that both parties are serious and want to move into due diligence. While non-binding on price, some elements like exclusivity periods and confidentiality obligations can be legally binding.

How is a company valued in an M&A deal?

Valuation in M&A typically involves multiple methods: discounted cash flow analysis (based on future earnings), comparable company analysis (based on how similar public companies are priced), and precedent transactions (based on what similar companies sold for in past deals). Strategic buyers may also add a synergy premium on top of the standalone value.

Why do some M&A deals fail?

Deals fail for many reasons. Some fall apart during due diligence when unexpected issues come to light. Others fail because the two sides cannot agree on price or terms. Post-merger, deals often underperform because integration is poorly managed - teams do not align, systems do not connect, and the expected synergies never materialize. Having a clear plan at every stage, including the right tools for communication and document management, significantly reduces these risks.

Final thoughts

M&A is one of the most complex and high-stakes activities in business. It touches every part of an organization - finance, legal, operations, HR, and leadership. Getting it right requires good strategy, good advisors, and good processes.

But at its core, a successful deal comes down to trust and information. The buyer needs reliable information to make a confident decision. The seller needs to control how that information is shared. And both parties need a clear record of everything that happened throughout the process.

That is exactly what a virtual data room is designed for. Not as a nice-to-have, but as a fundamental part of how modern deals are run.

If you are preparing for an M&A process - whether as a buyer, seller, or advisor - the right time to set up your data room is before you need it. Get your documents organized, your access controls in place, and your NDA process ready.

Ellty makes all of that straightforward. No complex onboarding, no per-user surprises, and no enterprise contracts. Just a clean, professional data room that works from day one.

Ready to run a cleaner, faster due diligence process? Start your Ellty data room for free today. Upgrade to Room or Room Plus when you are ready for the full feature set. |

Author

Anika Tabassum Nionta is a Content Manager at Ellty, where she writes about secure document sharing, virtual data rooms, M&A, due diligence, fundraising, and sales enablement. With over 6 years of writing experience, she helps professionals understand how to share confidential documents securely, track engagement, and manage deals more effectively. Anika holds both a BA and MA in English from Dhaka University. Outside of work, she enjoys reading, exploring new cafes in Dhaka, and connecting with entrepreneurs and dealmakers in her community.