You have probably heard the term "mergers and acquisitions" on business news or in a boardroom conversation. But if you have never been part of a deal, it can feel like a dense, jargon-heavy world that is hard to understand from the outside.

This guide breaks it all down in plain language. We will cover what M&A actually means, the different types of deals, why companies do them, and how the process actually works from start to finish. And because documents sit at the heart of every deal, we will also explain how a virtual data room (VDR) like Ellty helps teams manage the process safely and efficiently.

Whether you are a founder exploring your exit options, a business development professional, or simply someone who wants to understand how large business transactions work, this guide is for you.

What is a merger?

A merger happens when two separate companies agree to come together and form a single, new entity. It is generally a mutual decision, meaning both companies agree that combining their resources, teams, and operations will create more value than continuing separately.

Think of it like two rivers joining to become one larger, stronger river. Each company brings its own strengths, and together they flow in the same direction.

Who is involved in a merger?

- The two companies entering the agreement (often described as the "acquiring" company and the "target" company, though in a true merger both are considered equal partners)

- Boards of directors from both sides, who must approve the deal

- Shareholders, who typically vote on whether to go ahead

- Legal and financial advisors on both sides

- Regulators, who may need to review the deal if it creates competition concerns

A simple example

One of the most well-known mergers in recent history was the combination of Sprint and T-Mobile in 2020. Both were competing mobile carriers in the United States. Rather than continue fighting for market share, they merged to create a more competitive network that could better challenge AT&T and Verizon.

What is an acquisition?

An acquisition is different. Here, one company buys another company outright. The company doing the buying is called the acquirer. The company being bought is called the target.

After the deal closes, the acquired company may continue to operate under its own name, be merged into the acquirer's existing operations, or be rebranded entirely. The key difference from a merger is that it is not a joining of equals; one company is taking ownership of another.

Who is involved in an acquisition?

- The acquiring company and its leadership team

- The target company and its shareholders (who receive payment)

- Investment banks, advisors, and legal teams

- Due diligence teams who review the target's finances, contracts, and risks

- Regulators, in many cases

A simple example

When Microsoft acquired LinkedIn in 2016 for $26.2 billion, that was an acquisition. Microsoft paid cash for the company, LinkedIn's shareholders received a payout, and LinkedIn continued to operate as a distinct product under Microsoft's ownership.

Key types of M&A

Not all M&A deals are the same. They vary based on the relationship between the companies involved and the strategic goals behind the transaction.

Horizontal M&A

This happens between two companies in the same industry that compete directly with each other. The goal is usually to increase market share, reduce competition, or gain scale. The Sprint-T-Mobile merger is a good example of this.

Vertical M&A

Here, a company acquires another that sits at a different stage of the same supply chain. For instance, a car manufacturer buying a parts supplier. The goal is usually to gain more control over production, reduce costs, or improve delivery times.

Conglomerate M&A

This involves companies from completely different industries. A media company buying a food brand, for example. The goal is usually diversification, reducing the risk of relying on a single market.

Market-extension deals

Two companies that sell the same product or service but in different markets come together. A US software company acquiring a European software company to enter new geography is one example.

Product-extension deals

Companies that serve the same customer base with related but different products combine. A social media platform acquiring a photo-editing app is a classic example.

Type | What it means | Common goal |

Horizontal | Two competitors in the same industry | Scale and market share |

Vertical | Companies at different supply chain stages | Cost control and efficiency |

Conglomerate | Companies in different industries | Diversification |

Market-extension | Same product, different geography | Expanding into new markets |

Product-extension | Related products, same customers | Cross-selling and growth |

Common motives behind M&A deals

Companies do not enter mergers or acquisitions randomly. There is always a strategic reason behind the decision. Here are the most common ones.

Growth

Organic growth takes time. Acquiring another company can deliver customers, products, revenue, and market presence in a fraction of the time it would take to build those from scratch.

Synergies

When two companies combine, they often find they can operate more efficiently together than separately. This might mean sharing a sales team, consolidating offices, or combining technology platforms. These cost savings and efficiency gains are called synergies.

Talent acquisition

Sometimes a company does not want the target's revenue or products. It wants the team. This is called an "acqui-hire" and is especially common in the technology sector.

Eliminating competition

If a rival is growing quickly and posing a threat, acquiring them before they become a bigger problem is a strategic move some companies take. Regulators, however, pay close attention to this.

Accessing new technology or IP

Rather than building technology in-house, a company may simply buy the business that already owns it. This is faster and often more cost-effective.

Diversification

Companies sometimes acquire businesses in different sectors to reduce their dependence on a single market. If one industry declines, they have other revenue streams to fall back on.

How the M&A process works

An M&A deal is not a single event. It is a process that often takes months, sometimes more than a year, from first conversation to final close. Here is how it typically unfolds.

1. Strategy and target identification

Before any deal can happen, the acquiring company needs a clear strategic reason for pursuing it. Why this company? Why now? Once that is defined, the team identifies potential targets and begins early research.

2. Initial approach and non-disclosure agreement (NDA)

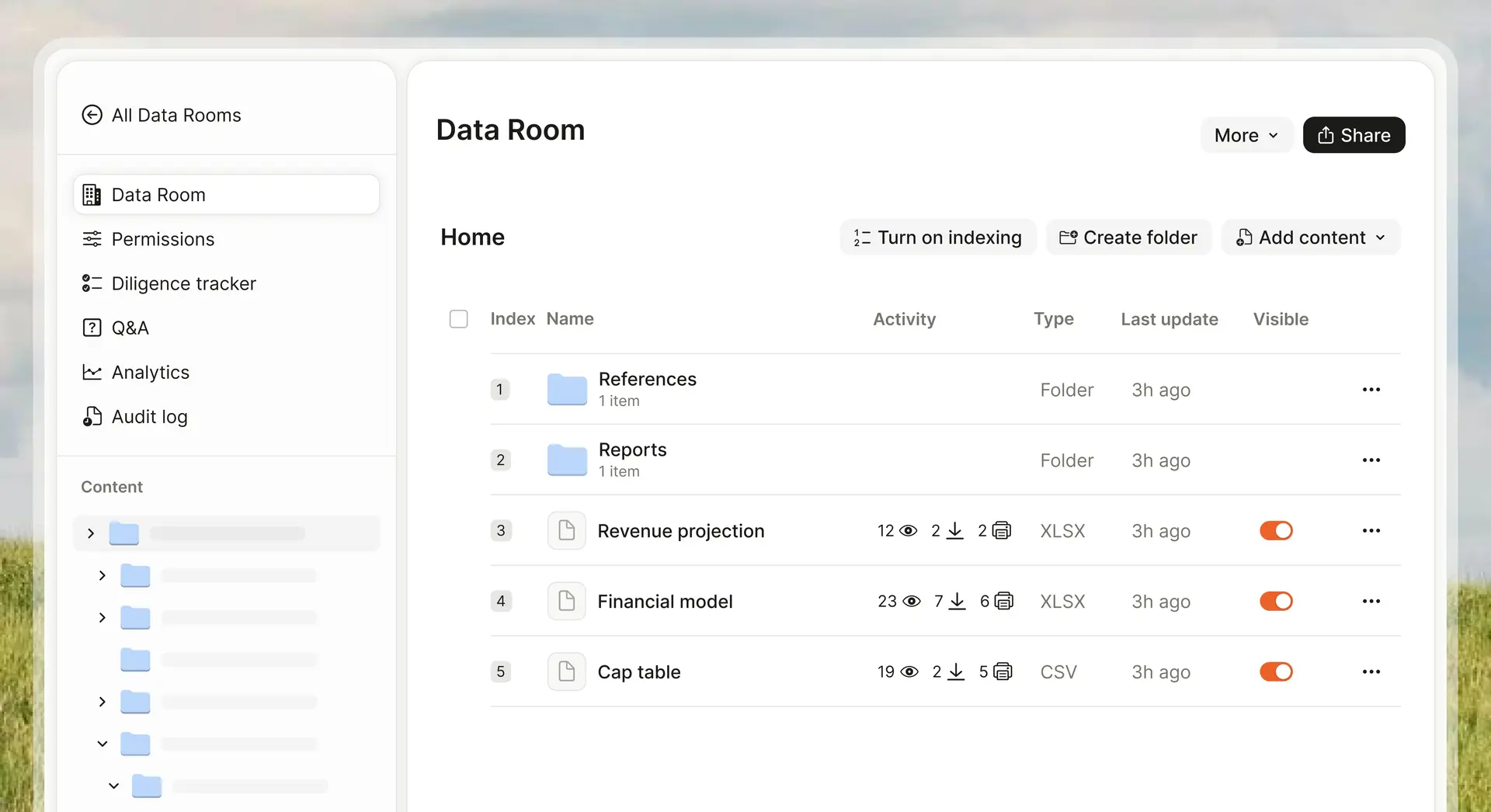

When a target is identified, the acquirer makes an approach. Before any sensitive information is shared, both sides sign an NDA to protect confidential details. This is often where document-sharing tools first come into play.

3. Letter of intent (LOI)

If early conversations go well, the acquirer issues a letter of intent. This is a non-binding document that outlines the key terms of the proposed deal and signals a serious commitment to move forward.

4. Due diligence

This is the most document-intensive phase of the entire process. The acquirer's team reviews everything: financials, legal contracts, employee agreements, intellectual property, customer data, regulatory filings, and more. This is where a virtual data room becomes critical.

5. Negotiation and deal structure

Based on what the due diligence reveals, the two sides negotiate the final terms. Price, payment structure, timelines, warranties, and conditions are all worked through at this stage.

6. Regulatory review

Depending on the size and nature of the deal, regulators may need to approve it. In some jurisdictions, large M&A deals must be reviewed to ensure they do not reduce competition in a harmful way.

7. Closing

Once all approvals are in place and final documents are signed, the deal closes. Money changes hands, ownership transfers, and the integration process begins.

Managing due diligence? Ellty makes it simple. Secure document sharing, real-time access tracking, NDA gating, and dynamic watermarking - all in one clean platform. No per-user fees, no surprises. Start free. |

How a virtual data room helps in M&A and why Ellty stands out

Every M&A deal involves a massive amount of sensitive documentation. Financial records, legal agreements, contracts, board minutes, IP filings, employee data - all of it needs to be shared with the deal team, but in a controlled and secure way.

That is exactly what a virtual data room (VDR) is built for. Instead of emailing documents back and forth (which is slow, disorganized, and carries serious security risks), a VDR provides a single, secure environment where the right people can access the right documents and nothing else.

What a good VDR does during M&A

- Access control: Controls who can see, download, or print each document

- Activity tracking: Shows you when someone opens a file, how long they spent on it, and which pages they reviewed

- NDA gating: Requires potential buyers to agree to an NDA before they can view documents

- Dynamic watermarking: Automatically marks documents with the viewer's identity to deter leaks

- Audit trails: Maintains a clear record of every action taken in the data room

Why Ellty is the right tool for M&A teams

Most legacy VDR platforms are expensive, slow to set up, and priced in a way that penalizes growing deal teams. Per-user charges and custom pricing quotes can add significant cost to an already expensive process.

Ellty takes a completely different approach. It is a secure document sharing and analytics platform with full data room functionality, designed for anyone who needs to share sensitive documents in a controlled, trackable way - without the enterprise contract and the enterprise price tag.

Ellty plans at a glance

Every plan includes flat, transparent pricing with no per-user fees and no surprise charges. Whether you are sharing documents with 3 people or 30, you pay the same amount. For deal teams that want a professional VDR features without the enterprise process, Ellty is the clear choice.

What makes Ellty different from legacy VDR providers No per-user charges. No per-page fees. No weeks-long setup. You pick a plan, get access immediately, and know exactly what you are paying. The Room and Room Plus plans give you everything a controlled due diligence process needs - granular permissions, NDA gating, dynamic watermarking, restricted access, and full audit logs. |

How mergers are structured

The structure of a merger determines how the two companies come together legally and financially. There are a few common approaches.

Statutory merger

One company absorbs the other entirely. The acquired company ceases to exist as a separate legal entity, and its assets and liabilities transfer to the acquiring company. This is the most straightforward structure.

Subsidiary merger

The acquired company becomes a wholly owned subsidiary of the acquirer. It keeps its own legal identity, brand, and operations but is now under the acquirer's ownership. This is common when the target has strong brand recognition that the acquirer does not want to disrupt.

Consolidation merger

Both companies dissolve and form an entirely new entity. Neither the acquirer nor the target continues under their original name. Instead, they create something new together. This is less common but is used when both parties are seen as equal in the deal.

Vertical vs. horizontal mergers - what is the difference?

This is one of the most commonly asked questions about M&A, so it is worth giving it extra clarity.

Horizontal merger

Two companies in the same industry combine. They typically sell similar products or services and compete for the same customers. The main benefit is scale - by joining together, the combined business has more market power, more resources, and less direct competition.

Example: Two regional banks merging to create a larger national bank.

Vertical merger

A company acquires another that sits earlier or later in its supply chain. Rather than competing with each other, these companies were previously in a supplier-customer relationship. By merging, the acquirer gains control over a key part of its production or distribution process.

Example: A clothing retailer acquiring a fabric manufacturer.

Key insight Horizontal mergers tend to attract more regulatory scrutiny because they reduce the number of competitors in a market. Vertical mergers can also raise concerns but are generally viewed differently, since they do not directly eliminate a competitor. |

How M&A deals are financed

Once the price is agreed, the acquiring company has to figure out how to actually pay for it. There are several ways deals are financed, and often a combination of methods is used.

Cash

The acquirer pays the target's shareholders in cash. This is straightforward and often preferred by sellers because they receive immediate, certain value. It requires the acquirer to have significant cash reserves or access to credit.

Stock (share exchange)

Instead of cash, the acquirer offers its own shares to the target's shareholders. This is common when the acquirer does not want to deplete its cash reserves. The risk for sellers is that the value of shares can go up or down after the deal closes.

Debt financing

The acquirer borrows money to fund the acquisition. This is known as a leveraged buyout (LBO) when the acquired company's own assets and cash flows are used as collateral for the borrowing. Private equity firms frequently use this approach.

Earn-out arrangements

Part of the payment is deferred and tied to the future performance of the acquired company. If the company hits certain revenue or profit targets after the deal closes, the sellers receive additional payments. This structure helps bridge disagreements over valuation.

M&A valuations - how is a company priced?

One of the most complex parts of any deal is agreeing on what the target company is actually worth. Buyers and sellers often have very different views on this, and valuation is one of the most common sources of deal friction.

Here are the main methods used to value a company in an M&A context.

Comparable company analysis (comps)

This looks at how similar publicly traded companies are valued and applies those multiples to the target. If companies in the same sector typically trade at 10x their annual earnings, that benchmark provides a starting reference point.

Precedent transaction analysis

This looks at what acquirers have paid for similar companies in past M&A deals. It helps establish market norms and provides a reality check on whether a proposed price is reasonable.

Discounted cash flow (DCF)

This method projects the target's future cash flows and discounts them back to what they are worth in today's terms. It is considered the most rigorous approach but is highly sensitive to the assumptions behind the projections.

Asset-based valuation

This adds up the fair market value of everything the company owns - its assets - and subtracts what it owes. It is more commonly used for companies being broken up or in distressed situations, rather than for healthy operating businesses.

How M&A affects shareholders

If you own shares in either company involved in a deal, the transaction will almost certainly have an impact on those shares. Here is what typically happens.

Shareholders in the target company

Target company shareholders usually benefit most directly. Acquirers typically offer a premium above the current market price to convince shareholders to sell. This premium can range anywhere from 10% to over 50% in some competitive situations. Shareholders vote on whether to accept the deal, and if a sufficient majority agrees, the sale proceeds.

Shareholders in the acquiring company

The impact is less predictable here. In theory, a well-executed acquisition should increase the long-term value of the combined business. In practice, acquiring company share prices often dip in the short term after a deal is announced - partly because the acquirer is paying a premium, and partly because investors are uncertain about whether integration will go smoothly.

Institutional and activist investors

Large investors sometimes play an active role in pushing for or against M&A deals. Activist shareholders may campaign for a sale if they believe a company is undervalued, while others may oppose a proposed acquisition if they think the price is too high.

Frequently asked questions

What is the difference between a merger and an acquisition?

A merger involves two companies combining as equals to form a new entity. An acquisition is when one company buys another outright. In practice, the line is sometimes blurry. Many deals described as "mergers" are functionally acquisitions because one company is clearly the dominant party.

How long does an M&A deal take to complete?

It varies considerably. A smaller deal between private companies might take three to six months from initial conversations to close. Larger, more complex transactions, especially those requiring regulatory approval, can take a year or more.

What is due diligence, and why does it matter?

Due diligence is the investigative process where the acquirer thoroughly examines the target company before committing to a deal. It covers financials, legal contracts, intellectual property, customer relationships, regulatory compliance, and much more. It is critical because it helps the acquirer understand exactly what they are buying and identify any risks or hidden problems before it is too late.

What is a virtual data room, and do I need one for M&A?

A virtual data room (VDR) is a secure online platform for sharing confidential documents during a deal process. For any serious M&A transaction, a VDR is essentially essential. It gives you organized, controlled access to documents, tracks every action taken, and provides the audit trail that both sides need. Ellty offers full data room functionality starting at $149/month with no per-user fees.

What does "synergy" mean in the context of M&A?

Synergies refer to the efficiencies and additional value that are created when two companies combine. Cost synergies might mean eliminating duplicated roles or offices. Revenue synergies might mean cross-selling each company's products to the other's customer base. Synergies are often used to justify the premium paid in a deal.

Can an acquisition fail? What are the risks?

Yes, many acquisitions fail to deliver on their initial promise. The most common reasons include overpaying for the target, cultural clashes between the two workforces, poor integration planning, and deals motivated more by ambition than sound strategy. Research consistently shows that a significant proportion of M&A deals destroy rather than create value for the acquirer's shareholders.

What is a hostile takeover?

A hostile takeover happens when an acquiring company bypasses the target's management and board and makes a direct offer to the target's shareholders. This is the opposite of a friendly acquisition, where both sides agree to negotiate. Hostile takeovers are more common in public markets and often involve extended battles for control.

Final thoughts

Mergers and acquisitions are, at their core, about one thing: creating value. Whether that is achieved through scale, efficiency, new technology, or access to new markets, the underlying logic of M&A has not changed much over decades.

What has changed is how deals are executed. The tools available today, especially secure, trackable document sharing platforms, have made it possible for smaller teams to run professional, organized processes that previously required large investment banks and enterprise software budgets.

If you are approaching a deal of any size, the foundation you lay during due diligence will determine how smoothly everything else goes. A clean data room, clear document organization, and full visibility over who is reviewing what will save you time, reduce risk, and project professionalism to every party involved.

Ellty was built for exactly this. No enterprise contracts. No per-user fees. No complex onboarding. Just a clean, professional data room that you can set up and start using right away.

Start your M&A process with Ellty Secure document sharing, NDA gating, dynamic watermarking, and full audit logs. Plans start free, with full data room features from $149/month. Flat pricing, no surprises. Get started in 5 minutes. |

Author

Anika Tabassum Nionta is a Content Manager at Ellty, where she writes about secure document sharing, virtual data rooms, M&A, due diligence, fundraising, and sales enablement. With over 6 years of writing experience, she helps professionals understand how to share confidential documents securely, track engagement, and manage deals more effectively. Anika holds both a BA and MA in English from Dhaka University. Outside of work, she enjoys reading, exploring new cafes in Dhaka, and connecting with entrepreneurs and dealmakers in her community.