Investing money is serious business. Whether you are a venture capitalist backing an early-stage startup, a private equity firm acquiring a mature company, or a strategic buyer looking to expand through M&A, you cannot afford to skip doing your homework.

That homework has a name: investment due diligence.

This guide is a complete, practical, and no-fluff walkthrough of what investment due diligence actually means, what you need to check, and how to run the process efficiently, especially when you are managing dozens of documents and multiple stakeholders at the same time.

And if you are wondering how to keep all of that document-sharing organized, secure, and trackable, we will show you exactly where Ellty fits in.

What is investment due diligence?

Investment due diligence is the process of thoroughly researching and verifying every important detail about a company or asset before you invest in it or acquire it.

Think of it like buying a house. You would not hand over the money without a structural survey, a legal title check, and a good look at the neighborhood. Investing in a business works the same way, except the checklist is much longer.

Due diligence covers everything from financial health and legal standing to team quality, market position, technology, and operational efficiency. The goal is simple: before you commit your capital, you want to know exactly what you are getting into.

The process typically involves reviewing hundreds (sometimes thousands) of documents, speaking to the management team, verifying claims made in pitch decks and information memorandums, and stress-testing financial models.

It is not about trying to catch someone in a lie. Most of the time, due diligence is simply about building confidence that what has been presented to you is accurate and identifying any risks you need to price in or negotiate on.

Why is due diligence necessary?

You might be wondering: if the deal looks great on paper and the founders seem trustworthy, why go through all the trouble?

Because deals that look great on the surface sometimes have hidden problems underneath. And by the time those problems surface post-investment, it is usually too late to walk away without taking a significant loss.

Here is why due diligence is non-negotiable:

- Risk Identification: Every investment carries risk. Due diligence helps you find out what those risks actually are, whether it is a pending lawsuit, a customer concentration issue, or a cap table that will cause problems down the line.

- Value Verification: Companies can present their numbers in a flattering light. Due diligence checks whether the revenue is real, recurring, and sustainable.

- Negotiation Leverage: When you find issues during diligence, you can use them to negotiate a better price or ask for protective clauses in the deal terms.

- Fiduciary Responsibility: For institutional investors like VC and PE firms, thorough due diligence is not just good practice, it is a legal obligation to your fund's limited partners.

- Strategic Alignment: You need to confirm that the business you are buying into actually fits your investment thesis, sector focus, or growth strategy.

- Regulatory Compliance: Many deals have cross-border implications or involve regulated industries. Due diligence ensures you are not walking into a compliance minefield.

Skipping or shortcutting due diligence is one of the most expensive mistakes you can make. The time and cost of doing it properly is almost always less than the cost of discovering a problem after the deal closes.

Running a deal right now?

Set up your Ellty data room in minutes and start sharing documents securely. Get started free.

The 4 P's of due diligence

Experienced teams often talk about evaluating an opportunity through the lens of four core dimensions. These are commonly known as the Four P's:

1. People

The quality of the team behind a business is often the single most important factor, especially in early-stage investing. You want to understand who the founders and key executives are, what their track record looks like, how deep the team is, and whether they have the skills and resilience to execute on their plan.

A diverse, experienced, and complementary team is a strong positive signal. Over-reliance on a single individual is a red flag.

2. Performance

This is where the numbers come in. You will look at key performance metrics like Internal Rate of Return (IRR), Multiple on Invested Capital (MOIC), revenue growth rates, margins, churn, and unit economics. Past performance does not guarantee future results, but it tells you a great deal about execution quality.

3. Philosophy

Does the company's vision and operating philosophy align with your investment goals? A business obsessed with short-term cash generation may not suit a growth-focused fund. Understanding the management team's core beliefs about value creation, market approach, and long-term strategy is essential.

4. Process

How does the business actually operate day to day? A well-run company has documented processes, clear decision-making structures, and systems that do not depend entirely on the founder being in the room. A strong process signals scalability.

These four dimensions work together. A company with great numbers but a weak team, or a passionate founder with no repeatable process, will struggle over time. Good diligence evaluates all four.

Types of investment due diligence

Due diligence is not a single activity, it is a collection of workstreams, each focused on a different area of the business. Here is a breakdown of the main types:

Financial due diligence

This is the backbone of any investment review. You are looking at historical financial statements, revenue trends, cost structures, working capital, cash flow, and forward projections. The goal is to verify that the financials are accurate, understand what drives performance, and assess whether the business model is sustainable.

Legal due diligence

Legal diligence covers the corporate structure, shareholder agreements, key contracts, intellectual property ownership, pending or historical litigation, regulatory licenses, and employment arrangements. This is where you find out if there are any legal landmines hiding under the surface.

Operational due diligence

Here you evaluate how the business actually runs. That includes supply chain, technology infrastructure, internal systems, quality controls, HR practices, and business continuity planning. A business can look financially strong but be operationally fragile.

Market / commercial due diligence

This workstream looks outward. How big is the market? Where does the company sit competitively? What are the key customer relationships? How is the business differentiated? You are testing whether the growth story is credible given the real competitive landscape.

Technical due diligence

Particularly relevant for technology companies. Technical diligence looks at the product architecture, code quality, technical debt, security posture, and scalability of the tech stack. It answers the question: can this product actually do what they say it can?

ESG due diligence

Increasingly important, especially for institutional investors. ESG diligence examines the company's environmental footprint, governance practices, labor standards, diversity policies, and any reputational or regulatory risks related to sustainability.

Tools for investment due diligence

Running due diligence requires more than just good judgment, you need the right tools to manage documents, track communication, analyze data, and maintain security. Here is what a typical due diligence toolkit looks like:

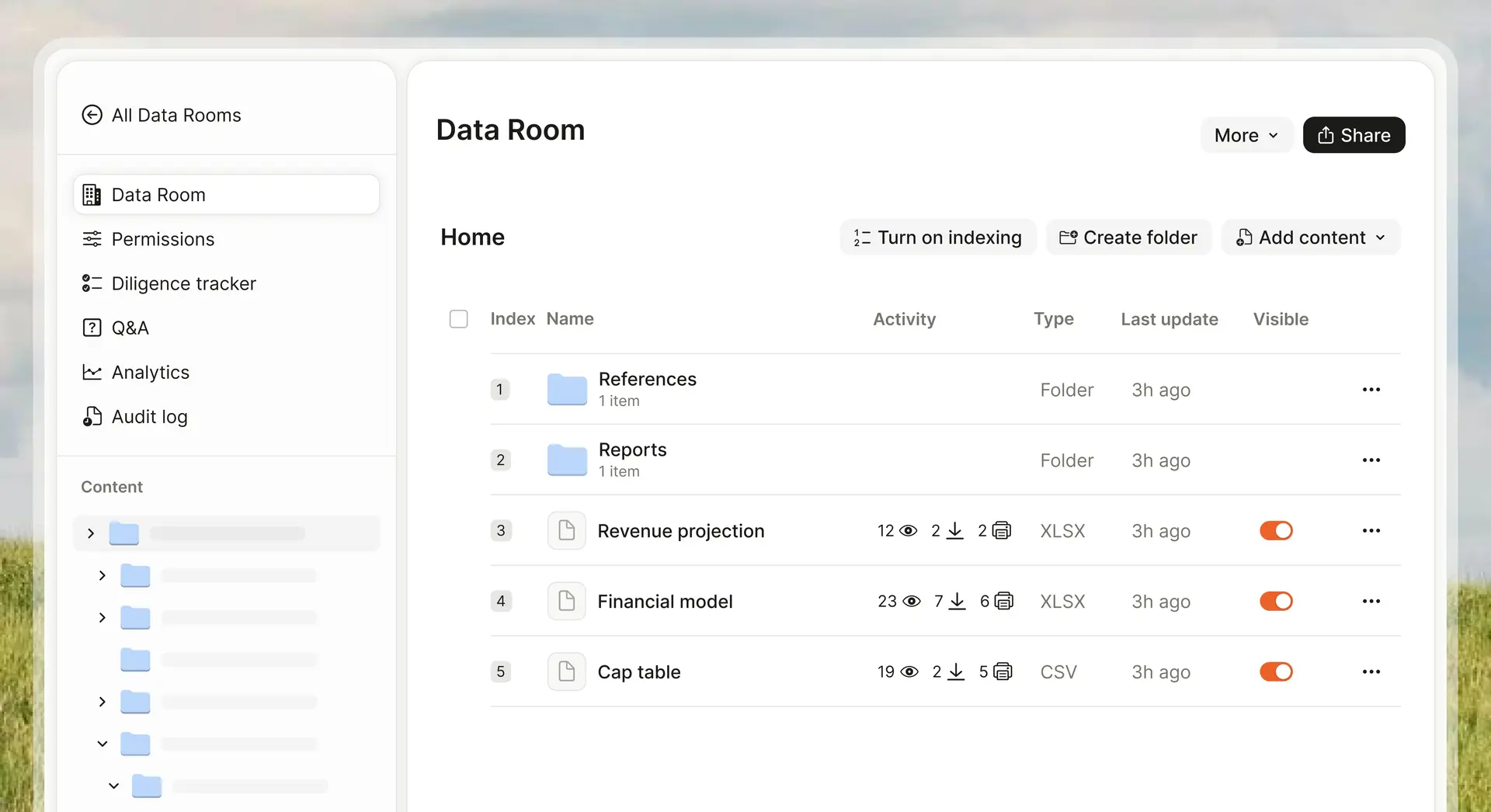

Virtual data rooms (VDRs)

A VDR is the central document-sharing environment for any deal. It is where the target company uploads its documents and the investment team conducts their review. A good VDR gives you access controls, NDA gating, document analytics, watermarking, and audit logs - all in one place.

Financial modelling Tools

Excel and Google Sheets remain the standard for building and stress-testing financial models. More sophisticated deals may use dedicated FP&A tools like Mosaic or Jirav.

Legal review platforms

Tools like Kira or Luminance use AI to extract and flag key clauses from contracts, saving legal teams hours of manual review work.

Reference check tools

Background and reference checking platforms help validate team credentials and surface any reputational concerns about founders or senior management.

Project management tools

Coordinating due diligence across multiple workstreams requires a clear project management structure. Tools like Notion, Asana, or even a shared tracker help keep everything moving.

Of all these tools, the VDR is the one that shapes the entire due diligence experience. It is where most of the work actually happens and where the most sensitive information lives.

How a virtual data room actually changes due diligence

Before virtual data rooms existed, due diligence was done in physical rooms. Seriously. Lawyers and investors would fly to a location, sit in a windowless room, and manually review paper documents. It was slow, expensive, and wildly inconvenient.

VDRs changed everything. Here is what a proper virtual data room actually does for your due diligence process:

Centralized document management

Everything lives in one place. Instead of documents being scattered across email threads, Dropbox folders, and WhatsApp messages, a VDR gives you a single organized repository that everyone on the deal team can access from anywhere.

Controlled access

Not everyone on the buy side needs to see everything. A VDR lets you set granular permissions. So your legal advisor can see contracts, your financial analyst can see the financial model, and your technical reviewer can access the tech documentation without any cross-contamination.

NDA gating

Before anyone can access the data room, you can require them to sign an NDA electronically. This creates a clean, enforceable record of who agreed to confidentiality terms and when.

Activity tracking and analytics

This is where VDRs become genuinely powerful. You can see exactly who opened which document, how long they spent on it, and what they looked at most. For sellers, this is incredibly valuable intelligence. For buyers, it helps prioritize what needs follow-up.

Dynamic watermarking

Any document downloaded or viewed can be automatically watermarked with the viewer's name, email, and timestamp. This acts as a strong deterrent against unauthorized sharing.

Audit trails

A complete log of all activity in the data room creates accountability. If something is later disputed, the audit trail tells the truth.

Faster deal execution

Because everything is organized, accessible, and trackable, deals move faster. Q&A rounds that used to take weeks can be managed in days.

Why Ellty is the go-to platform for investment due diligence

There are many VDR solutions on the market. Most of them were built for enterprise procurement teams with six-figure budgets and months to implement. Ellty was built for people who need a professional, secure data room without the enterprise overhead.

Here is what makes Ellty different:

Flat, transparent pricing

Legacy VDR platforms charge per user, per page, or per gigabyte. Those fees add up fast, especially on a busy deal. Ellty charges a flat monthly fee with no per-user charges and no surprise overages. You know exactly what you are paying before you start.

Quick setup

You can have a fully functional, professional data room on Ellty in minutes. No lengthy onboarding, no implementation consultant required. For time-sensitive deals, that matters.

The Right Features at Every Stage

Ellty offers four plans that match different stages and deal sizes:

No per-user charges

Building a deal team means inviting lawyers, analysts, advisors, and reviewers. With traditional VDR platforms, each new user adds to your bill. With Ellty, you can add your whole team without watching the invoice grow.

Document intelligence

Ellty real-time analytics show you exactly who is looking at your documents, what they are spending time on, and what they are ignoring. That kind of intelligence helps you have better conversations and make smarter decisions.

Security built-in

Access controls, NDA gating, dynamic watermarking, and restricted visitor access are all included in the appropriate plans, not sold as expensive add-ons.

Ready to run a cleaner, faster due diligence process? Start with Ellty free plan or explore the Room plan, purpose-built for deal teams.

Investment due diligence checklist

Below is a comprehensive, practical checklist organized by due diligence category. Use this as your master reference for any investment or acquisition process.

Financial documents

- Audited financial statements (last 3-5 years)

- Management accounts for the most recent period

- Tax returns (last 3-5 years)

- Financial projections and underlying assumptions

- Cap table (current ownership structure)

- Details of all debt, loans, and credit facilities

- Working capital analysis

- Revenue breakdown by customer, product, and geography

- Gross margin and EBITDA bridges

- Deferred revenue and backlog

- Cash flow statements and treasury position

Legal documents

- Articles of Incorporation and all amendments

- Shareholder agreements and voting rights

- Board minutes (last 3 years)

- Material contracts (customers, suppliers, partners)

- Employment contracts for senior team members

- IP ownership documentation (patents, trademarks, copyright)

- Licensing agreements (inbound and outbound)

- Litigation history and any pending legal actions

- Regulatory licenses and permits

- Data protection and privacy compliance records

- Real estate leases and property agreements

Operational documents

- Organizational chart

- Key personnel CVs and background information

- HR policies and employee handbook

- Staff headcount by department and role

- Key supplier and vendor agreements

- Technology infrastructure overview

- IT security policies and incident history

- Operations manual or standard operating procedures

- Insurance policies and coverage

- Business continuity and disaster recovery plan

Market and commercial documents

- Market analysis and third-party research reports

- Competitive landscape analysis

- Customer contracts and key account details

- Customer concentration analysis

- Pipeline and sales forecasts

- Product or service roadmap

- Pricing strategy and history

- Net Promoter Score or customer satisfaction data

- Churn rates and retention analysis

- Marketing strategy and channel breakdown

Technical documents (for tech companies)

- Technical architecture documentation

- Code quality and technical debt assessment

- Security audit reports and penetration testing results

- Scalability and infrastructure capacity analysis

- Third-party software licenses and dependencies

- Development roadmap and sprint history

- Uptime and SLA performance records

ESG and governance

- Corporate governance policies

- Board composition and independence

- Environmental impact and compliance records

- Sustainability reporting or ESG policies

- Diversity, equity, and inclusion policies

- Whistleblower and ethics policies

- Related-party transactions

Real-world examples of investment due diligence

Understanding due diligence in theory is one thing. Seeing how it plays out in practice is another. Here are three scenarios that illustrate how due diligence works across different investment types.

Example 1: Series A venture capital deal

A VC firm is considering leading a $5M Series A in a B2B SaaS company. The founders have shared a pitch deck showing impressive ARR growth and a strong net revenue retention figure.

During due diligence, the financial review reveals that a large portion of the reported ARR is made up of a single enterprise contract that is up for renewal in three months. The contract includes a cancellation clause with 30-day notice.

This is a material risk that was not immediately obvious from the headline numbers. The deal still closes, but with a lower pre-money valuation and a milestone clause tied to the contract renewal.

Without diligence, the VC firm would have paid more than the business was worth at that point.

Example 2: Mid-market private equity acquisition

A PE firm is acquiring a manufacturing business for $40M. The business looks healthy on paper - strong margins, growing revenue, solid customer base.

Operational due diligence uncovers that the company's production capacity is nearly maxed out. Growing revenue beyond the current level would require a significant capital investment in new equipment. This was not reflected in the seller's financial projections.

The PE firm adjusts its financial model to account for the capex requirement, renegotiates the price down, and structures an earnout tied to the seller's support during the transition.

Example 3: Strategic acquisition

A large technology company wants to acquire a smaller software firm to add a specific product capability. The acquisition seems straightforward from a commercial perspective.

Legal due diligence reveals that a key piece of the target company's core technology was developed using open-source components with a license that could require the acquirer to open-source their own product if they incorporate the code.

The deal is restructured, the target company rewrites the problematic module before closing, which delays the deal by six weeks but prevents a potentially catastrophic intellectual property issue post-acquisition.

These examples share a common theme: the deal was possible in each case, but the details uncovered during due diligence changed the terms, the price, or the structure in a meaningful way.

How to conduct investment due diligence

Here is a practical, step-by-step walkthrough of how a due diligence process typically runs from start to finish.

Step 1: Define your scope and objectives

Before requesting a single document, be clear about what you are trying to learn. What are the key value drivers of this investment? What are your biggest concerns? What would make you walk away?

Setting clear objectives helps you prioritize your efforts and avoid getting lost in documents that do not actually affect your decision.

Step 2: Set up your data room and NDAs

Create a secure data room and ensure all parties have signed appropriate NDAs before any sensitive information is shared. This protects everyone and establishes clear confidentiality terms from the start.

This is where a platform like Ellty makes immediate practical sense. You can set up a professional data room in minutes, configure NDA gating so no one accesses the room until they have agreed to terms, and start tracking activity from day one.

Step 3: Issue a due diligence request list

Prepare a structured list of everything you need to see. Organize it by category and share it with the target company or their advisors. A clear, well-organized request list sets a professional tone and accelerates the process.

Step 4: Document review

Work through the uploaded documents systematically. Assign specific workstreams to the right team members or advisors. Flag items that need clarification or further investigation. Keep notes.

Step 5: Management interviews

Some of the most valuable due diligence insights come from direct conversations with the management team. These conversations let you probe the assumptions behind the numbers, understand the culture, and assess the depth of leadership.

Step 6: Third-party verification

Where possible, verify key claims independently. Speak to customers. Check references for the founding team. Commission independent market research. Have your lawyers review the contracts. Do not rely solely on documents provided by the seller.

Step 7: Risk assessment and modelling

Compile all findings into a coherent risk register. Identify the risks that are deal-breakers, those that should affect the price or terms, and those you can accept. Update your financial model to reflect what you have learned.

Step 8: Due diligence report

Write up your findings in a structured due diligence report. This document should summarize what you found, flag key risks, note open items, and make a clear investment recommendation. It also serves as an institutional record if questions arise later.

Diligence by investor type: VC vs PE vs Strategic

Not all due diligence looks the same. The depth, focus, and timeline of a due diligence process varies considerably depending on who is doing the investing and why.

Venture capital

VCs invest early, often before there are many hard numbers to analyze. Due diligence for VC is heavily weighted toward team assessment, market opportunity, and product-market fit signals. Financial modelling is still done, but the assumptions are inherently speculative. Reference checks on founders carry enormous weight.

Private equity

PE diligence is highly structured and thorough. Because PE firms are typically acquiring majority or full ownership of mature businesses using leveraged capital, the stakes are high and the scrutiny is intense. Financial and operational due diligence are the core workstreams. Legal and regulatory review is extensive. Management interviews are used to test whether the team can perform under a new owner.

Strategic acquirers

Corporate acquirers doing M&A are often focused on specific strategic objectives, acquiring a technology, entering a market, or eliminating a competitor. Their diligence often goes deeper on IP, integration complexity, customer relationships, and regulatory approvals. The process tends to be the longest and involves the most stakeholders.

Best practices for investment due diligence

Whether you are doing your first deal or your fiftieth, these best practices will help you run a cleaner, faster, and more effective due diligence process.

- Start with a clear scope. Define what matters most before you start requesting documents.

- Use a structured data room from day one. Do not let documents live in emails or shared drives. A proper VDR keeps everything organized, tracked, and secure.

- Assign workstreams to specialists. Do not try to do everything yourself. Use the right lawyers, accountants, and technical advisors for the right areas.

- Issue a comprehensive request list early. The sooner you ask for everything you need, the sooner you can identify gaps and delays.

- Track document engagement. If you are the seller or adviser, knowing who is looking at what helps you understand where the deal is stalling or where concerns are forming.

- Maintain a Q&A log. Keep a record of all questions asked and answers given. This prevents things from getting lost and creates a useful reference if disputes arise later.

- Verify independently wherever possible. Do not take management's word for it on key claims. Speak to customers, check references, and get third-party opinions.

- Document everything. Your due diligence report is not just for the investment committee, it is your institutional memory if anything goes wrong later.

- Do not rush. The cost of a poor investment dwarfs the cost of spending an extra week doing diligence properly.

Common due diligence pitfalls to avoid

Even experienced investors make mistakes in due diligence. Here are the most common ones and how to avoid them.

Moving too fast

Competitive deal pressure sometimes makes investors feel like they need to cut corners to close quickly. Rarely does this pay off. A week of proper diligence is almost always worth it.

Overreliance on management presentations

Management teams are optimistic about their own businesses that is natural. But you cannot base your investment decision on a polished pitch deck. Go behind the deck and verify the underlying data.

Ignoring the cap table

A company with a complicated or messy cap table, lots of convertible notes, conflicting liquidation preferences, or unhappy early investors can create serious problems at exit. Review it carefully and understand the economic reality of your position at various exit scenarios.

Focusing only on financials

Financial diligence is important, but companies fail for operational, legal, and cultural reasons too. Make sure you are looking at the whole picture.

Underestimating integration risk

For acquisitions, the work does not stop when the deal closes. Companies that skip integration planning during diligence often find themselves with a much harder post-close environment than expected.

Skipping customer reference checks

Talking to real customers is one of the most valuable things you can do during diligence. They will tell you things that do not appear in any document.

Inadequate data security

Sharing hundreds of sensitive documents over email or generic file-sharing services is a serious security risk. Using a proper VDR with access controls and audit trails protects both parties.

Frequently Asked Questions

How long does investment due diligence take?

It depends on the deal type and complexity. Venture capital deals at Series A level typically take three to six weeks. Mid-market M&A transactions usually run four to eight weeks. Large enterprise acquisitions or IPO-related diligence can take several months. The more complex the business and the larger the document volume, the longer it takes.

Who typically conducts due diligence?

Due diligence is usually conducted by the investing party and their advisors. That typically includes the investment team, external lawyers, financial advisors or accountants, and technical specialists. Larger deals may also involve market research firms, environmental consultants, and industry experts.

What is a virtual data room and do I need one?

A virtual data room (VDR) is a secure online platform for sharing and reviewing confidential documents during a transaction. If you are involved in any serious investment or acquisition process - yes, you need one. It keeps documents organized, protects sensitive information, and creates an auditable record of who saw what and when. Platforms like Ellty offer professional VDR functionality at a flat, affordable monthly price with no per-user charges.

What documents are most important in due diligence?

The most critical documents tend to be: audited financial statements, the capitalization table, material contracts (especially customer and supplier agreements), intellectual property ownership documentation, shareholder agreements, and any pending litigation disclosures. These items carry the highest risk if they contain surprises.

What is the difference between due diligence for VC and PE?

Venture capital due diligence is typically shorter, lighter on documents, and focused heavily on the team, market opportunity, and early traction signals. Private equity due diligence is more intensive, covering full operational and financial reviews with hundreds or thousands of documents. PE diligence is closer to the scrutiny applied in M&A transactions.

Can due diligence kill a deal?

Yes and sometimes that is the right outcome. Due diligence is specifically designed to surface problems that were not visible upfront. If the diligence process reveals material misrepresentations, undisclosed liabilities, or fundamental problems with the business model, it is perfectly appropriate to walk away. The purpose of diligence is not to find reasons to do the deal, it is to make sure you are making an informed decision either way.

How does Ellty help with investment due diligence?

Ellty is a secure document sharing and analytics platform with full virtual data room functionality. For due diligence, it gives you access controls so you can manage exactly who sees what, NDA gating to protect confidentiality from the start, real-time document analytics to track engagement, dynamic watermarking to deter unauthorized sharing, and full audit logs for accountability. Pricing is flat and transparent from a free plan for early conversations up to the Room Plus plan at $349/month for large multi-party deals. There are no per-user fees and no surprise charges.

Final Thoughts

Investment due diligence is one of the most important things you will do as an investor or deal professional. It protects your capital, improves your decisions, and makes you a better counterparty to work with.

The process does not need to be painful. With a clear checklist, a structured approach, and the right tools in place, especially a proper virtual data room, due diligence can be efficient, thorough, and even a source of competitive advantage.

Ellty was built to make that part of the process as smooth as possible. Flat pricing, quick setup, and all the features that actually matter for a real deal team.

Start your next due diligence process the right way. Set up your Ellty data room today - free to start, no credit card required.

Author

Anika Tabassum Nionta is a Content Manager at Ellty, where she writes about secure document sharing, virtual data rooms, M&A, due diligence, fundraising, and sales enablement. With over 6 years of writing experience, she helps professionals understand how to share confidential documents securely, track engagement, and manage deals more effectively. Anika holds both a BA and MA in English from Dhaka University. Outside of work, she enjoys reading, exploring new cafes in Dhaka, and connecting with entrepreneurs and dealmakers in her community.