Most business owners think M&A due diligence is paperwork. It isn’t.

It is the part of the deal where your story gets audited.

Every slide. Every metric. Every contract. Every promise you made during the first call.

If something breaks here, it does not just delay the deal. It changes the price. Or it kills the deal completely.

Large companies expect due diligence to be slow and painful. Businesses usually aren’t ready for it. That gap is where founders lose leverage. Here is the uncomfortable truth. Buyers do not use due diligence to “learn more about your company”. They use it to find reasons to:

- lower valuation

- change deal structure

- introduce earn-outs

- push retention clauses

- delay signing

If you walk in unprepared, you hand them that leverage. For businesses, this matters more than for mature companies for three reasons.

First, your risk profile is higher. You probably have:

- shorter operating history

- concentrated revenue

- fewer long-term contracts

- fast-moving product decisions

- incomplete documentation

That is normal for a business. But it also means every open risk is more visible.

Second, your business is usually founder-driven. If the buyer sees that knowledge, customers, or product decisions sit in your head and not in documents, they see execution risk. They will price that in.

Third, your numbers are usually interpreted more aggressively. A small mistake in revenue classification or churn calculation in a public company barely moves the needle. In a business deal, it changes the whole narrative. One metric mismatch can turn “strong growth” into “unstable revenue quality”.

Most founders only realize this when the buyer’s diligence team starts sending long, uncomfortable questions.

Typical examples:

“Why does your revenue in Stripe not match your financials?”

“Why does this contract say something different from your deck?”

“Why is this IP assignment missing for a former contractor?”

“Why does this customer represent 41% of revenue?”

None of these are rare. What hurts is not that the questions exist. What hurts is being slow and inconsistent with answers. Speed and clarity during M&A due diligence signal one thing to buyers. Operational maturity. And maturity reduces perceived risk. That directly protects your valuation. There is another problem founders underestimate. Diligence is exhausting. It runs in parallel with running the company, closing new customers, managing your team, and negotiating the deal itself.

If you start organizing documents after the LOI, you will work nights for weeks. You will also make avoidable mistakes. The right time to prepare for M&A due diligence is not after a buyer appears. It is before you start talking to buyers. This guide is written for that reality. Not for corporate M&A teams. Not for advisors. For founders.

What is M&A due diligence in business

M&A due diligence is the buyer’s verification process. It is where a potential acquirer validates that your company is legally clean, financially accurate, operationally stable, and commercially defensible.

In simple terms. Your pitch creates interest. Your data must prove it. In business, M&A due diligence is not one activity. It is a coordinated review across multiple areas. For businesses, the scope usually includes five core pillars.

Financial due diligence

This answers one question. Is the revenue real and repeatable?

Buyers look at:

- historical financial statements

- revenue recognition methods

- churn and retention

- customer concentration

- cost structure

- cash position and runway

- forecast assumptions

They are not only checking totals. They are checking consistency. If your MRR report does not match your accounting exports, you will be asked to reconcile every line. Financial due diligence is where most renegotiations start.

Legal and corporate due diligence

This answers a different question. Does the buyer actually get what they think they are buying?

This includes:

- incorporation documents

- cap table and shareholder agreements

- option plans

- IP ownership and assignments

- customer and partner contracts

- employment and contractor agreements

- past and ongoing disputes

For businesses, IP and ownership issues are the most common deal blockers. A single missing IP assignment from an early contractor can pause the entire transaction.

Commercial and customer due diligence

This answers: How stable is the business?

Buyers review:

- customer contracts and terms

- renewal behavior

- termination clauses

- pricing structure

- discounts and special agreements

- pipeline quality

They want to understand how much revenue is truly locked in. Not how much you hope to close.

Product and technology due diligence

This answers: Can this product scale and survive inside the buyer’s environment?

This typically includes:

- architecture overview

- hosting and infrastructure setup

- major dependencies

- internal development processes

- security practices at a high level

- technical debt exposure

For SaaS businesses, this is often done by a technical reviewer on the buyer side. They are not judging code style. They are judging risk.

People and operations due diligence

This answers: Can the business continue without falling apart?

This includes:

- key employee dependencies

- incentive structures

- vesting and retention risks

- internal processes

- outsourced operations

Founders are often surprised how much attention this gets. If too much knowledge sits with one or two people, the buyer will flag it.

From a business perspective, M&A due diligence has one main goal: risk pricing. Not validation. Not learning. Pricing.

Every risk discovered during diligence is translated into one of three actions:

- lower price

- deferred payment

- additional legal protection

That is why founders must stop treating diligence as a formality. It is a negotiation tool. Just controlled by the buyer. There is also a structural difference between startup due diligence and corporate due diligence. In large companies processes are already documented, reporting is standardized, and contracts are centrally managed

In startups:

- documents are scattered

- versions conflict

- ownership is unclear

- reporting definitions change over time

That is not incompetence. It is speed. But during M&A due diligence, speed becomes noise. Your job as a founder is to reduce that noise. Practically, M&A due diligence in business is executed through a secure data room. The buyer’s team accesses your documents. They review them. They ask structured follow-up questions. They track inconsistencies. They request clarifications.

The quality of this workflow directly affects:

- how fast diligence finishes

- how confident the buyer feels

- how aggressive their legal and financial protections become

One more thing founders misunderstand. Due diligence is not only about what you upload. It is also about how you respond. If you answer quickly, consistently and with traceable documents, you look organized. If you answer with ad hoc messages and attachments, you look fragile. That perception carries into final negotiations.

How the M&A due diligence process works step by step

The due diligence process usually starts right after a letter of intent is signed. In reality, it starts much earlier than that. The buyer already has assumptions about your business before the LOI. Due diligence is simply where those assumptions get tested with documents instead of conversations.

For founders, the process can be broken into a small number of predictable phases. If you understand these phases, you can control stress, time, and deal momentum much better.

The first phase is internal preparation. This is where most businesses fail before diligence even officially begins. You gather financials, contracts, cap table files, product documentation, and internal policies. You clean up missing signatures and conflicting versions. You assign internal owners for each document category so questions do not bounce around the team. When this phase is rushed, the entire diligence cycle becomes reactive instead of controlled.

The second phase is LOI alignment and scope definition. After the LOI, the buyer typically sends an initial diligence request list. This is often called a diligence checklist or data request list. It defines what areas they plan to review and how deep they will go. Founders should treat this document seriously because it defines the size of the work ahead. If the list is unusually broad, it usually signals risk sensitivity or internal uncertainty on the buyer side.

The third phase is data room setup and controlled access. This is where you upload and organize all requested materials in a structured data room. Folder structure matters more than founders expect. Review teams are used to standardized layouts. When your folders follow predictable logic, reviewers move faster and ask fewer clarification questions. Access is normally limited to a small group of buyer-side reviewers at first, and expanded only when required.

The fourth phase is primary document review. This is when the buyer team starts opening files, reviewing contracts, analyzing numbers, and mapping inconsistencies. This stage is silent from your side, but activity is high on their side. You should expect a delay between upload and the first real question wave. That delay is not a good sign or a bad sign. It simply means reviewers are working through the material.

The fifth phase is Q&A and follow-up requests. This is the most operationally demanding stage for founders. Reviewers start sending questions tied to specific files or data points. Some questions are simple clarifications. Others uncover structural issues that require explanation, additional documents, or context. How you manage this phase has a direct impact on trust. Centralizing answers and always attaching supporting documents prevents confusion and repeated follow-ups.

The sixth phase is deep-dive reviews in selected areas. Not every category receives equal attention. If the buyer sees potential risk in revenue quality, IP ownership, or technical architecture, they may bring in specialists. This can extend the process and introduce additional document requests. Founders should not interpret this as deal weakness. It is normal risk management, especially in technology and SaaS acquisitions.

The seventh phase is issue resolution and risk negotiation. This is where diligence stops being purely operational and becomes commercial. Any unresolved risks are translated into legal protections, price adjustments, or deal structure changes. Examples include retention bonuses, earn-outs, indemnities, and escrow requirements. This is also where many founders feel valuation pressure for the first time after the LOI.

The final phase is confirmation and closing preparation. At this point, most material questions have been answered. Remaining requests are usually procedural. Legal teams prepare final transaction documents based on the results of diligence. If diligence was clean and well organized, this phase is short. If diligence surfaced unresolved issues, closing can stretch for weeks.

Founders should understand one simple operational truth. The faster you answer clearly and consistently, the faster diligence moves forward. Speed alone is not enough. Your answers must be traceable to documents. When answers are based only on explanations without files, reviewers assume uncertainty.

This is also why disciplined document management matters. When your data room is structured and permissions are controlled, you reduce noise, limit accidental oversharing, and protect sensitive materials. A clean workflow does not make your company safer. It makes your company easier to trust.

Who is involved in M&A due diligence

M&A due diligence is not run by one person. It is a coordinated review across multiple teams on both sides of the deal. As a founder, you should know exactly who is involved and what each group actually cares about. It helps you prioritize answers and avoid over-explaining the wrong things to the wrong people.

On the seller side, the founder is always the central coordinator. Even if advisors are heavily involved, the buyer expects the founder to own accuracy and context. Founders usually act as the bridge between internal teams, external advisors, and the buyer’s review teams. If that coordination breaks, delays multiply very quickly.

A finance lead or external accounting advisor is normally responsible for all financial diligence materials. This person prepares financial statements, revenue breakdowns, reconciliations, and forecast models. They also respond to questions related to revenue recognition, churn calculation, and cost allocation. Founders should avoid answering financial questions directly unless they are supported by reconciled data.

Legal counsel plays a critical role throughout diligence. They review and organize corporate documents, shareholder agreements, IP assignments, contracts, and employment files. They also manage legal risk discussions with the buyer’s lawyers. For founders, legal counsel is not only about protection. It is also about speed. Clean legal documentation reduces negotiation cycles later in the deal.

Operational leaders are often pulled into diligence later than expected. This usually includes heads of sales, product, engineering, and customer success. They are asked to explain how the business actually runs. Their input is especially important during commercial and technical reviews. Founders should prepare these team members early so they are not surprised by sudden review meetings or document requests.

On the buyer side, a deal lead or corporate development manager coordinates the entire diligence effort. This person manages the request list, prioritizes review areas, and keeps the transaction timeline moving. They are also responsible for summarizing diligence results for internal investment or acquisition committees.

The buyer’s finance team or external financial advisors run financial due diligence. They validate reported metrics, revenue quality, cost structure, and forecast assumptions. They are not trying to rebuild your financial model. They are trying to determine how reliable your reported performance is and how it compares to what was discussed during early negotiations.

The buyer’s legal team conducts legal and corporate diligence. They review your corporate structure, ownership, IP, contracts, and compliance posture. Their role is to identify exposure that could create post-acquisition problems. They are also the group that translates diligence findings into contractual protections and representations in the final agreement.

A technical review team is often involved when the target is a technology-driven business. This may include internal engineers, security specialists, or external consultants. Their focus is not feature comparison. Their focus is system architecture, operational risk, and long-term maintainability. Founders should be prepared for high-level technical explanations and documentation, not product demos.

In some transactions, commercial or market advisors are also involved. They analyze customer behavior, competitive positioning, and pipeline sustainability. Their output influences internal confidence in future growth. If your customer contracts and revenue concentration are weak, their feedback becomes important in valuation discussions.

The most common mistake founders make is assuming all reviewers are looking for the same information. They are not. Finance teams care about reconciliation and consistency. Legal teams care about enforceability and ownership. Technical reviewers care about operational risk. Deal leads care about timing and risk aggregation.

Understanding these roles allows founders to respond more effectively. It also helps you route questions to the right internal owner immediately instead of trying to personally answer everything. In diligence, organization is not a soft skill. It is a measurable advantage that directly affects how smoothly your deal moves forward.

What documents buyers usually request

Buyers do not ask for documents randomly. Their request list follows the same internal review workflow almost every time. If you prepare your documents using these categories, you will reduce back and forth and shorten the review cycle.

For a business, the document set is usually grouped into six practical buckets. The exact list changes by deal size and industry, but the structure rarely changes.

Corporate and ownership documents are always requested first. This is where buyers confirm that your company legally exists, is properly structured, and is owned by the people you say it is owned by. You should expect to share your certificate of incorporation, articles of association, board consents, shareholder agreements, option plans, cap table exports, and any past financing documents. If your cap table does not match executed agreements, you will be asked to reconcile it line by line.

Finance and tax documents form the backbone of financial due diligence. Buyers normally request historical financial statements, management accounts, revenue and cost breakdowns, bank statements, payroll summaries, and forecast models. Tax filings, VAT or sales tax reports, and any correspondence with tax authorities are also common. If you use multiple tools for revenue and accounting, buyers will expect you to explain how numbers move between systems.

Customers and revenue documents are used to test revenue stability and contract enforceability. This usually includes customer contracts, master service agreements, order forms, renewal schedules, pricing schedules, and any special side letters or custom terms. Buyers often ask for a customer list with contract values, start dates, renewal dates, and churn status. If your revenue is usage based or transactional, you will also be asked for usage and billing data.

Product and intellectual property documents are required to confirm ownership and technical risk. Founders should prepare IP assignment agreements, contractor agreements with IP clauses, product architecture overviews, third-party dependency lists, and open-source usage disclosures. Hosting providers, cloud contracts, and major technology vendors are usually reviewed as part of this set.

HR and operations documents show how dependent the business is on specific people and how employment risk is managed. Buyers usually ask for employee and contractor agreements, compensation structures, option and vesting schedules, and organizational charts. If you rely on outsourced teams, you should also expect to provide those service agreements.

Legal, regulatory, and risk documents are used to surface exposure. This includes compliance policies, privacy policies, security policies, any past disputes, regulatory correspondence, and insurance policies. If your business operates in a regulated space, buyers will request licenses, approvals, and audit reports relevant to your sector.

The practical mistake founders make is mixing these categories together in one large folder or sharing them through email attachments. Review teams expect predictable structure. When documents are not grouped properly, reviewers waste time searching and send unnecessary clarification questions.

M&A due diligence checklist

This checklist is written from a founder’s point of view. It is not exhaustive for every possible deal, but it covers what most buyers will expect in a standard startup acquisition.

Start with company and ownership readiness. You should confirm that your incorporation documents, shareholder agreements, board approvals, and cap table exports are complete and consistent. Option grants and vesting schedules must match what is reflected in your cap table. Any historical changes to ownership, including early advisor equity or SAFE conversions, should be clearly documented.

Prepare your financial and reporting materials next. This includes at least two to three years of financial statements if available, monthly management reports, revenue and expense breakdowns, and a clear bridge between accounting data and operational metrics such as MRR and churn. Your forecast should include written assumptions so buyers can understand how projections were built.

Review your customer and commercial documentation before opening any data room. Customer contracts should be executed, signed, and easy to read. Renewal and termination clauses should be summarized internally so you are not discovering risks for the first time during buyer review. Any special pricing or custom contract terms should be flagged clearly.

Clean up your product and IP ownership files. Every employee and contractor who contributed to your product should have a signed IP assignment. If any early contributors are missing agreements, this should be fixed before diligence starts. You should also prepare a simple architecture overview and a list of major technology dependencies.

Organize your people and operations materials. Employment agreements, compensation plans, and incentive structures should be current and consistent. You should be able to show how key roles are covered and where operational risk sits if someone leaves after closing.

Finally, prepare your legal and compliance materials. This includes privacy and data protection policies, regulatory filings where applicable, insurance coverage, and any past disputes or legal correspondence. Hiding issues does not protect you. Unprepared explanations create larger problems later.

This founder checklist is not about perfection. It is about removing obvious friction. Buyers accept startup risk. They do not accept disorganization.

Financial due diligence checklist

Financial due diligence is usually the most time consuming and the most sensitive part of the entire process. It is also where valuation discussions are most likely to shift. Founders should treat this area with more preparation than any other category.

Below is a practical financial due diligence checklist founders can use before opening a data room.

From a founder’s perspective, the most important preparation step is reconciliation. Your revenue numbers must match across your billing platform, your CRM, and your accounting system. Buyers will almost always test this alignment. If they find gaps, they will assume other numbers may also be unreliable.

You should also be prepared to explain how you define your key metrics. MRR, ARR, churn, and retention are often calculated differently across businesses. During diligence, definitions matter more than labels. Buyers will ask how upgrades, downgrades, refunds, and paused subscriptions are handled.

Forecasts deserve special attention. Most buyers do not expect you to hit your projections exactly. They do expect your assumptions to be reasonable and consistent with historical performance and pipeline reality. If your forecast assumes a dramatic improvement in sales efficiency without evidence, it will be challenged.

Another area founders underestimate is expense classification. Contractors, cloud costs, and marketing spend are often miscategorized during early growth. Buyers look for a clean separation between operating expenses and direct costs because it affects margin analysis and post-acquisition planning.

Finally, founders should prepare a short internal financial narrative before diligence starts. This is not a slide deck. It is a written explanation of how the business makes money, how it spends money, and where future growth is expected to come from. When financial reviewers understand your model quickly, the diligence conversation becomes more focused and far less adversarial.

Legal and compliance due diligence checklist

Legal and compliance diligence answers one simple question. Does the buyer actually get clean ownership of the company and its assets, without hidden obligations or future disputes.

For founders, this section is less about volume and more about precision. One missing document here can pause a deal longer than ten missing operational files.

Start with corporate and ownership records. You should prepare your certificate of incorporation, articles of association or bylaws, board and shareholder resolutions, historical financing documents, option plans, and all amendments. Buyers will compare these documents against your cap table and equity summaries. Any inconsistency between legal documents and what you show in spreadsheets becomes a red flag that must be reconciled.

Move next to shareholder and investor agreements. This includes shareholder agreements, voting agreements, investor rights agreements, SAFEs, convertible notes, and any side letters. Buyers review these to understand veto rights, liquidation preferences, information rights, and approval thresholds for a sale. Founders often underestimate how much these documents affect deal timing and closing mechanics.

Intellectual property ownership is one of the most sensitive areas for startups. You must be able to show that every employee and contractor who contributed to your product signed a valid IP assignment agreement. If your early team worked without proper agreements, this needs to be fixed before diligence starts. Buyers will also request trademark registrations, domain ownership, and patent filings if applicable.

Prepare your customer, partner, and vendor contracts as part of the legal review set. Even though these contracts are also reviewed commercially, legal teams focus on enforceability, assignment clauses, change-of-control provisions, and liability exposure. If a large customer can terminate the contract upon acquisition, that risk will be escalated immediately.

You should also include employment and contractor agreements in the legal folder. Buyers review non-compete clauses, confidentiality obligations, IP ownership language, and termination rights. Any missing agreement or inconsistent template between employees usually triggers follow-up requests.

For compliance and regulatory matters, prepare all applicable licenses, permits, approvals, and regulatory filings relevant to your business. If your product processes personal data, you should include your privacy policy, data processing agreements, and internal compliance policies. If you operate in a regulated industry, buyers will expect to see evidence of compliance processes, not only public-facing statements.

Finally, prepare a clear record of disputes and claims. This includes current litigation, past disputes, threatened claims, settlement agreements, and any regulatory inquiries. Founders often hesitate to disclose old issues. Buyers will usually find them during legal review anyway. What matters most is clarity, not perfection.

Commercial and customer due diligence checklist

Commercial and customer diligence focuses on how real and durable your revenue is. It is where buyers test whether growth comes from repeatable demand or short-term wins.

Founders should start by preparing a complete customer list. This list normally includes customer name, contract value, contract start date, renewal date, contract term, pricing model, and current status. Buyers use this to identify concentration risk and renewal exposure. If this list is not aligned with your financial reports, it will immediately be questioned.

You should prepare executed customer contracts and order forms for all material customers. Buyers review pricing, scope, renewal terms, termination rights, service levels, and any special clauses. Contracts signed by email, unsigned PDFs, or missing appendices often trigger requests for clarification and confirmations.

A separate focus area is renewals and churn behavior. Buyers typically ask for historical churn data, renewal rates, and customer retention by cohort. They want to understand how long customers actually stay, not how long contracts are written for. Founders should be ready to explain any unusual churn spikes, paused contracts, or renegotiated deals.

Prepare a summary of your pricing structure and discounting practices. Buyers review standard price lists, enterprise pricing exceptions, reseller or partner pricing, and any revenue share arrangements. If your pricing varies heavily between customers without clear rules, it introduces uncertainty in future revenue forecasting.

You should also prepare pipeline and sales process documentation. This usually includes your sales funnel stages, pipeline definitions, average sales cycle, and close rates. Buyers use this to test whether forecasted growth is realistic and whether your sales engine can scale under new ownership.

Finally, buyers often review customer success and support practices. This includes onboarding processes, support SLAs, escalation workflows, and customer satisfaction indicators where available. If your revenue depends heavily on high-touch service, buyers will treat operational scalability as a commercial risk.

Product and technology due diligence checklist

Product and technology diligence is not a code audit. It is a risk assessment. Buyers want to understand how fragile or resilient your product is in a new ownership environment.

Founders should begin with a high-level architecture overview. This should clearly describe your system components, major services, databases, integrations, and data flows. Buyers do not expect detailed technical documentation. They expect clarity on how the product is built and how its main parts interact.

Prepare a list of infrastructure and hosting providers. This usually includes your cloud provider, monitoring tools, CI/CD platforms, analytics services, and major third-party APIs. Buyers will review dependency risk, contract terms, and switching complexity. If your product relies heavily on a small number of external services, that risk must be transparent.

You should also prepare documentation on your development and release process. This includes version control practices, testing processes, deployment workflows, and rollback procedures. Buyers are not judging engineering culture. They are checking whether your team can safely operate and maintain the product at scale.

A critical section is security and data protection practices at a high level. Buyers often request an overview of access controls, internal permissions, data storage locations, backup policies, and incident response procedures. They are not asking for certifications unless your business depends on them. They are assessing operational maturity and exposure.

Prepare a clear view of your technical debt and known limitations. Founders are usually reluctant to document weaknesses. During diligence, hiding known issues creates much larger credibility problems later. Buyers understand that businesses carry technical debt. What matters is whether it is understood and managed.

You should also be ready to share your product roadmap and development priorities. This is not a commitment document. It helps buyers understand how future investment would be required to support growth, integration, or new market expansion. If the roadmap depends heavily on a small number of individuals, this becomes a people and retention risk.

HR and operations due diligence checklist

HR and operations diligence answers one practical question. Can the business continue to run smoothly after the acquisition.

Founders should begin by preparing a complete employee and contractor roster. This includes role, employment type, start date, location, compensation, bonus or commission structure, and equity participation. Buyers use this to understand cost structure, compliance exposure, and key role dependencies.

You should prepare employment and contractor agreements for every active team member. Buyers review termination rights, notice periods, confidentiality obligations, and IP ownership clauses. Missing agreements or inconsistent templates often trigger legal remediation before closing.

Prepare your equity and incentive documentation. This includes option grants, vesting schedules, acceleration clauses, and any retention or bonus agreements tied to a transaction. Buyers pay close attention to how much equity accelerates at closing and how much retention cost may be required post-acquisition.

Operational diligence also includes your organizational structure and decision flow. Buyers usually request an org chart, reporting lines, and ownership of key processes such as product delivery, sales execution, customer support, and infrastructure management. If too many operational responsibilities sit with the founder, buyers will classify this as execution risk.

You should also document your key-person dependencies. This is not only about senior leadership. It includes engineers maintaining core systems, sales leaders managing major accounts, and operational staff handling critical workflows. Buyers evaluate how easily responsibilities can be transferred or backed up.

Finally, prepare a clear view of your internal policies and operating practices. This includes onboarding processes, performance management practices, security training, and remote or hybrid work policies where applicable. Buyers use this information to assess integration complexity and cultural compatibility.

Founders often underestimate this section because it feels less technical than finance or legal review. In practice, weak operational structure is one of the main reasons buyers introduce retention requirements, management continuity clauses, and post-closing performance conditions.

M&A due diligence example for a SaaS startup

Assume a simple and realistic setup.

The company is a B2B SaaS startup with about $1.5M ARR, 42 customers, and a product sold mainly to mid market and enterprise teams. One buyer signs an LOI after a short commercial discussion and a product demo.

The first request list focuses almost entirely on revenue quality and contracts. The buyer asks for a full customer list with contract values, renewal dates, and contract terms. They also ask for a breakdown of ARR by customer and by plan. At this stage, the buyer is not yet reviewing product or security in depth. They are trying to confirm whether the revenue is stable enough to justify moving forward.

The first issue appears immediately.

The ARR reported in the pitch deck does not match the ARR calculated from the billing platform export. The gap is not huge. It comes from annual prepaid contracts being counted differently in internal reports. This takes three days to reconcile because finance and sales use different reporting logic. The buyer does not accuse the company of misreporting. They simply mark revenue reporting as an area of concern.

The second issue comes from customer contracts.

Out of the top ten customers, four contracts include change of control clauses that allow termination after acquisition. This was never flagged internally. The sales team treated those clauses as standard legal language. For the buyer, those clauses represent immediate churn risk after closing.

This does not kill the deal. But it changes how the buyer views revenue durability.

The third issue comes from intellectual property ownership.

Two early contractors helped build the original version of the product. Their agreements do not contain proper IP assignment clauses. One of them is no longer reachable. The legal team flags this as a real ownership gap and requests remediation before closing.

This becomes the longest delay in the entire process. Product and technology review happens later and is relatively clean. The architecture is modern. Infrastructure is stable. There is some technical debt, but it is documented and understood. The technical reviewer does not block the deal.

The real impact comes during the risk consolidation meeting on the buyer side.

Three points affect valuation discussions:

- revenue reporting inconsistency

- contract termination rights

- IP ownership gaps

The buyer proposes a lower upfront payment and introduces an escrow and a retention package for the founders.

Nothing about this outcome is unusual.

The business is healthy. The product is strong. Growth is real.

But due diligence exposes operational and legal risks that were invisible during early conversations.

What helped this startup in the end was not perfect documentation. It was speed and transparency. All follow-up questions were answered with supporting files. No explanations were given without evidence. That kept trust intact even when issues appeared.

This is what a normal SaaS M&A due diligence process looks like. Not dramatic. Not hostile. Just systematic risk discovery.

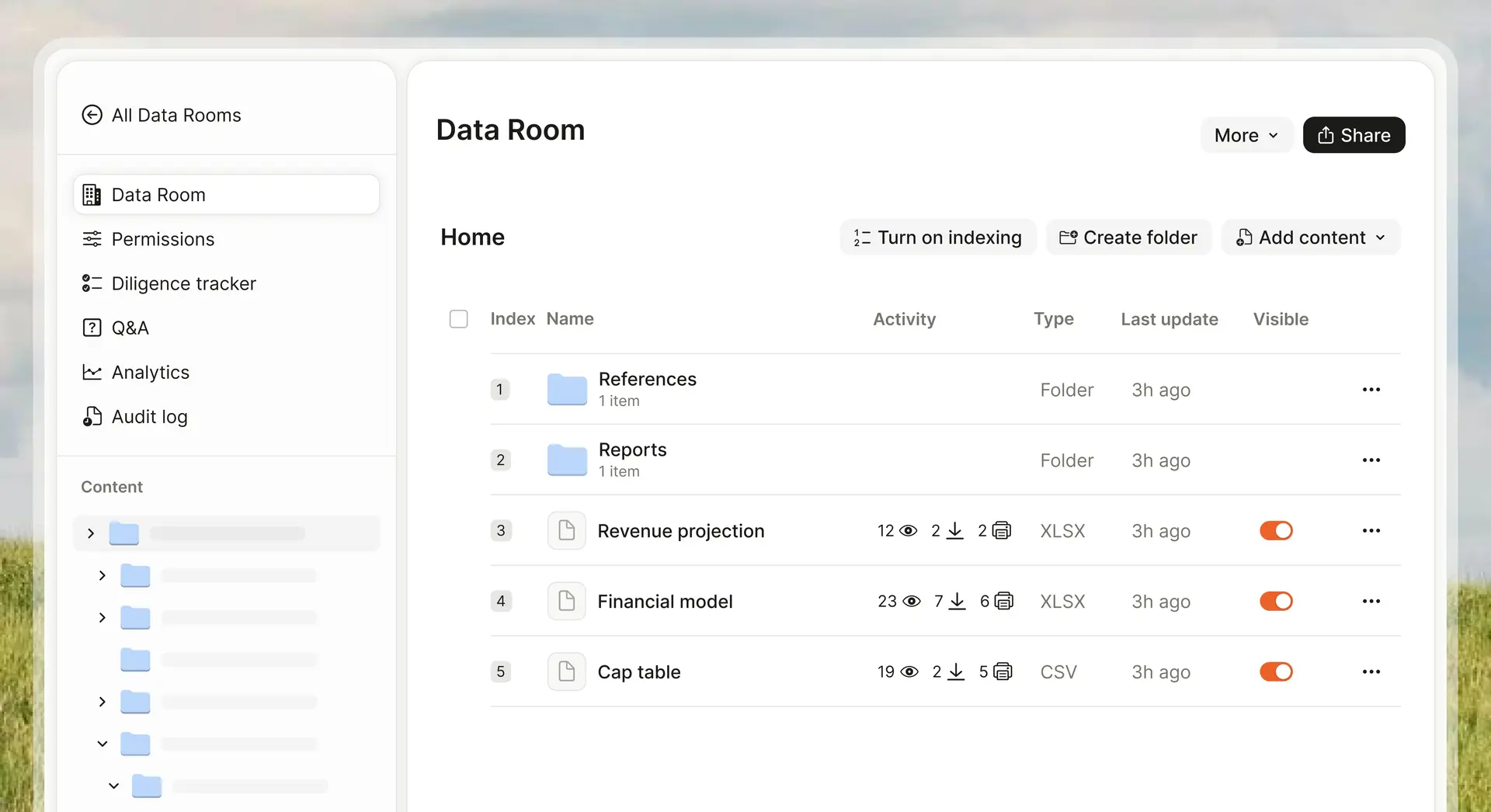

M&A due diligence sample data room structure

A clean data room structure removes unnecessary friction. Most buyers are used to a standard hierarchy. When your folders follow that structure, reviewers can start working immediately without asking where things are. A practical and widely accepted structure for M&A looks like this.

01 Corporate and ownership

This folder contains incorporation documents, bylaws, board and shareholder resolutions, cap table exports, option plans, and financing documents. It is the first place legal and corporate teams open.

02 Financial and tax

This folder contains financial statements, management reports, revenue breakdowns, expense reports, payroll summaries, bank statements, forecasts, and tax filings. Subfolders for each fiscal year help reviewers work faster.

03 Customers and commercial

This folder contains customer contracts, order forms, pricing schedules, renewal summaries, churn and retention reports, and customer lists. If you have enterprise and SMB contracts, separating them into subfolders reduces review time.

04 Product and IP

This folder contains IP assignment agreements, contractor agreements with IP clauses, architecture overview documents, dependency lists, cloud contracts, and any relevant product documentation.

05 HR and operations

This folder contains employee and contractor agreements, compensation structures, option and vesting schedules, organizational charts, and internal operational policies.

06 Legal, compliance and risk

This folder contains privacy policies, data processing agreements, regulatory filings, licenses, insurance policies, dispute records, and any regulatory correspondence.

This structure works because it mirrors how buyer teams are organized internally.

It also prevents one common founder mistake. Uploading everything into a single shared folder and letting the buyer sort it out.

That approach creates confusion and increases review time. It also increases the number of clarification questions you receive.

M&A due diligence template teams can reuse

Founders need one simple internal tool during diligence. A document tracker. Not a project management system. Not a CRM. A single list that shows what is requested, what is ready, and who owns it. A practical template looks like this.

This template does three things at once.

It gives you visibility over progress.

It creates accountability inside your team.

It reduces repeated questions from buyers.

You should maintain this tracker privately. Buyers do not need to see your internal status or remediation notes. What they need is fast access to correct documents. A small but important detail is ownership. Every document should have a single internal owner. When questions arrive, you should already know who is responsible for providing the answer. This tracker becomes even more important when multiple buyer teams are reviewing the same materials. It prevents version conflicts and accidental reuploads.

How to prepare for M&A due diligence before you go to market

Preparation is not about building a perfect data room. It is about removing obvious risks before a buyer finds them.

The first preparation step is cleaning up ownership and IP. Every employee and contractor who contributed to your product should have a signed IP assignment. If any early contributors are missing proper agreements, fix that immediately. This is one of the few areas that can completely block closing if ignored.

The second step is aligning your financial reporting. Your revenue numbers must match across your billing system, your CRM, and your accounting platform. If they do not, build a reconciliation process and document it. You should also define how you calculate MRR, ARR, churn, and retention and use those definitions consistently in internal reports.

The third step is reviewing customer contracts with a commercial mindset. Identify contracts that allow termination upon acquisition, unusual pricing commitments, or heavy service obligations. You do not need to renegotiate everything. You need to understand which contracts introduce post-acquisition risk so you are not surprised during diligence.

The fourth step is organizing your data room structure before any buyer exists. You should already have your core folders created and populated with your most important documents. Waiting for a buyer to request files forces you into reactive document collection and increases the likelihood of mistakes.

The fifth step is preparing your internal team. Your finance lead, legal counsel, and operational leaders should know that diligence will happen and understand what kind of information they will be asked to provide. The worst time to introduce diligence workflows is after the LOI.

The sixth step is preparing your narrative. Not your pitch. Your operational explanation. You should be able to clearly explain how revenue is generated, how costs scale, how customers are retained, and how the product is maintained. This narrative should match your documents. When explanations and files tell the same story, diligence becomes smoother.

Finally, prepare for workload and timing. Due diligence always takes longer than founders expect. It overlaps with normal operations. It creates pressure on key people. If you do not reserve internal capacity in advance, response speed drops and deal momentum suffers.

The goal of preparation is not to eliminate all risk.

The goal is to avoid discovering preventable problems while a buyer is watching.

Common M&A due diligence mistakes founders make

Most diligence problems are not caused by bad businesses. They are caused by weak execution during the process.

The most common mistake is uploading incomplete or draft documents and assuming you can “clean it up later”. Reviewers do not wait for the clean version. They review what they see first. When the first version is wrong, the follow-up conversation becomes defensive instead of factual.

Another frequent mistake is answering questions without attaching proof. Founders explain context in calls or chat messages, but do not link the explanation to an actual file in the data room. Review teams cannot rely on verbal clarification. They need traceable evidence. When answers are not document-backed, the same question returns in a different form.

Founders also overshare sensitive documents too early. This usually happens when there is only one shared folder and no access control strategy. Early-stage reviewers do not need employment contracts, IP schedules, or internal policies. Oversharing increases internal risk and makes later permission tightening look suspicious.

A very common operational failure is losing track of what was already shared and what version was shared. Multiple people upload files from different sources. Filenames are inconsistent. Reviewers comment on an old file while the team refers to a new one. This creates unnecessary friction and erodes confidence.

Another mistake is letting diligence questions flow through private chats and email threads. There is no central record. There is no ownership. When legal, finance, and operations teams work in parallel, this quickly becomes unmanageable.

Founders also underestimate how damaging slow responses are. Long delays signal disorganization or internal disagreement, even when the real reason is workload. Speed does not mean rushing. It means having documents ready and knowing who owns each answer.

Typical mistakes to avoid:

- uploading unsigned or outdated contracts

- sharing inconsistent versions of financial reports

- answering questions without supporting files

- giving full access to all folders on day one

- mixing personal explanations with official records

- letting multiple people upload files without control

- not tracking who requested what and when

None of these are strategic problems. They are execution problems. And they are fully avoidable.

How data rooms actually help during M&A due diligence

A data room is not just a storage folder. In real diligence workflows, it solves three practical problems at the same time: control, clarity, and accountability.

First, a data room gives you controlled access. You decide which folders are visible and to whom. You can open financials without opening HR. You can give commercial reviewers access without exposing legal risk files. This reduces accidental disclosure and keeps early reviews focused.

Second, a data room creates a single source of truth. Every reviewer opens the same file. Every comment refers to the same version. When a document is replaced, you control the update. This removes version confusion, which is one of the biggest time drains in diligence.

Third, a data room creates an activity trail. You can see which documents are opened, how often, and in what sequence. This matters more than founders usually expect. It helps you understand which areas trigger deeper review and where questions are likely to follow.

During active diligence, a structured data room also simplifies Q&A workflows. Instead of re-sending attachments, you reference files already in the room. Reviewers can verify context immediately. This reduces repeated clarification cycles.

From an operational perspective, data rooms help founders in four very concrete ways:

- centralize all diligence material in one place

- enforce consistent folder structure across teams

- allow staged access instead of full exposure

- support traceability of reviewer activity

A shared drive can store files. A data room supports a process. That difference becomes very visible once multiple buyer-side teams start reviewing your company at the same time.

Where Ellty fits in M&A due diligence

Ellty is not built for complex enterprise M&A programs. It is built for teams running straightforward acquisition or strategic sale processes.

Ellty works well when you need:

- a clean place to upload diligence documents

- controlled access to sensitive folders

- trackable links for decks and financial packs

- visibility into who is reviewing what

- real-time alerts when buyers open files

Ellty offers data room features without per-user pricing. This matters when multiple advisors and reviewers need access for a short period of time.

For early and growth-stage businesses, the typical diligence workflow looks like this:

You share a pitch deck and financial summary.

You move into a structured data room.

You answer follow-up questions based on what buyers review.

Ellty supports this exact flow.

You can upload your pitch deck and supporting files, create trackable links for specific reviewers, and move selected buyers into a secure data room when diligence begins. You can see which pages are viewed, which documents receive attention, and when reviewers return.

For simpler use cases, Ellty provides fast setup and low operational overhead. You do not need to configure complex user hierarchies or long onboarding flows.

Ellty works best when:

- you are running one or a few parallel buyer processes

- your deal team is small

- your diligence scope is focused and structured

- you want visibility into engagement without heavy administration

Ellty is not designed for:

- very large enterprise transactions

- multi-country legal teams managing dozens of internal roles

- deeply customized approval workflows

That limitation is intentional. The platform is built to remove friction for founders, not to replicate enterprise compliance systems.

Ellty plans for M&A due diligence scenarios

Ellty pricing and features fit different stages of the diligence process.

Below is a practical way founders typically use each plan.

- Starter: $0

- Standard: $69 per month

- Data Room: $149 per month

- Data Room Plus: $349 per month

Starter - free forever

This plan works well when you are still in early conversations and want to understand buyer interest.

Typical use cases:

- sharing your pitch deck

- sharing an initial financial overview

- using document tracking

- viewing real-time analytics

- secure sharing links

This is enough when you are not yet running structured diligence.

Standard plan - $69 per month

This plan fits founders who are moving beyond one or two files and need proper structure.

Typical use cases:

- unlimited documents

- advanced analytics on engagement

- eSignatures for simple workflows

- basic data room usage

- custom branding

This is a good fit when multiple documents and reviewers are involved, but access control and legal gating are still light.

Data Room plan - $149 per month

This plan is designed for active M&A due diligence.

Typical use cases:

- granular folder and file permissions

- NDA gating before access

- dynamic watermarking

- restricted visitor access

- three users included

This is the level most founders use once an LOI is signed and structured review begins.

Data Room Plus - $349 per month

This plan supports heavier review activity and more complex reviewer groups.

Typical use cases:

- group-based visitor permissions

- audit logs for review activity

- up to 4,000 assets per data room

This plan works well when multiple buyer-side teams or advisors are reviewing in parallel and traceability becomes important.

Important positioning points for founders:

- Ellty does not charge per user.

- Plans are designed around document volume and access needs, not headcount.

- Setup is fast and requires no technical onboarding.

A simple rule to follow:

If you are still validating interest, start with Starter.

If diligence is active and sensitive, move directly to a Data Room plan.

Do not overbuild your workflow. Your goal during M&A due diligence is not to run a perfect virtual data room. Your goal is to move the deal forward with clarity, control, and speed.

How to set up a due diligence data room in Ellty

Setting up a data room in Ellty is intentionally simple. You are not configuring enterprise workflows. You are creating a clean, controlled space for reviewers to work without friction.

Start by creating a new workspace and naming it after the transaction or buyer group. Do not reuse an internal workspace that already contains operational files. A clean workspace avoids accidental sharing and helps you clearly separate diligence material from daily documents.

Next, create your top-level folders before uploading anything. A practical structure is:

- Corporate and ownership

- Financial and tax

- Customers and commercial

- Product and IP

- HR and operations

- Legal, compliance and risk

Creating the structure first prevents random uploads and saves time later when reviewers start asking for specific files.

Upload documents in batches by category, not by who owns the file internally. Finance uploads finance. Legal uploads legal. Product uploads product documentation. This keeps ownership clear and avoids duplicate versions entering the room.

Once files are uploaded, configure access rules by folder. Early reviewers usually only need access to financial and commercial folders. Legal and HR folders should stay restricted until there is a clear request. This staged access approach reduces risk and keeps the review focused.

If you are using a Data Room plan, enable NDA gating before access. Reviewers should accept the NDA before they see any file. This avoids separate NDA workflows and ensures all reviewers are contractually covered.

For sensitive documents such as cap tables, employment agreements, and pricing schedules, enable dynamic watermarking and restricted visitor access. This does not stop misuse completely, but it creates traceability and discourages casual sharing.

Before inviting buyers, test the room yourself using a separate email address. Make sure the permissions behave exactly as expected. Founders often assume permissions are correct and only discover issues after a reviewer points them out.

A simple setup checklist inside Ellty:

- Create a new workspace for the deal

- Create standard diligence folders

- Upload files by category

- Set folder-level permissions

- Enable NDA gating where needed

- Apply watermarking to sensitive folders

- Test access with a separate account

- Share controlled links with reviewers

This setup is usually enough for early and growth-stage diligence workflows.

When Ellty is not the right choice

Ellty is designed for teams running focused, time-bound diligence processes. It is not designed to replace enterprise governance systems.

You should not use Ellty if your transaction requires:

- dozens of internal approval layers

- complex reviewer role hierarchies across departments

- custom compliance workflows

- region-specific regulatory reporting modules

- deeply integrated document automation pipelines

If your deal involves very large internal legal teams across multiple countries and strict internal policy enforcement, you will likely need a platform built for enterprise governance and compliance.

Ellty is also not a fit if your organization requires:

- extensive internal workflow automation

- mandatory integration with large document management systems

- heavy customization of review processes

That does not mean Ellty lacks security features. It means the product is intentionally focused on simplicity and speed for founders.

Ellty works well when:

- your diligence team is small

- your reviewers are external buyers and advisors

- your main goal is controlled sharing and visibility

- your process needs to move quickly

If your main problem is organizational complexity inside your own company, not buyer access, Ellty will feel too lightweight.

How to use analytics during M&A due diligence

Most founders treat analytics as a curiosity. During diligence, analytics are operational tools. Ellty shows who viewed which document, which pages were opened, and how long reviewers stayed on each file. This tells you where attention is concentrated and where questions are likely to follow.

The first practical use is prioritization. If reviewers spend most of their time inside revenue reports and top customer contracts, you should expect financial and commercial questions next. That allows you to prepare reconciliations and supporting documents before the questions arrive.

The second use is review progression tracking. When a new reviewer group receives access, analytics help you see whether the review has actually started. Silence does not always mean disinterest. It often means the team has not opened the material yet.

The third use is identifying sensitive focus areas. If legal documents suddenly receive high activity, it usually means legal teams are now involved. This is often the point where contract and IP questions begin. Preparing legal counsel and internal owners in advance saves time.

Analytics also help during multi-buyer processes. When two buyers are reviewing in parallel, you can see which buyer is actively progressing and which one is stalled. This gives you a realistic signal about deal momentum without relying on verbal updates.

Practical ways founders use analytics during diligence:

- identify which documents trigger repeated views

- detect when new reviewers join the process

- anticipate follow-up questions by review behavior

- decide which internal owners should prepare next

Analytics do not replace communication. They reduce surprises.

Security and access control considerations for founders

Security in diligence is not about perfect protection. It is about sensible risk control while still allowing reviewers to work efficiently.

The first rule is staged access. Do not open your entire data room on day one. Start with financial and commercial materials. Expand access only when reviewers explicitly request additional areas. This limits unnecessary exposure and makes access changes easy to justify.

The second rule is folder-level permissions. Reviewers should only see what they are reviewing. Legal reviewers do not need product documentation. Commercial reviewers do not need employment agreements. Granular permissions reduce confusion and reduce accidental disclosure.

The third rule is NDA gating before access. Every reviewer should accept the NDA before opening files. This keeps the process clean and avoids chasing signed PDFs by email.

The fourth rule is watermarking for sensitive documents. Cap tables, pricing schedules, contracts, and employee information should be watermarked. This does not prevent copying, but it establishes accountability and discourages casual redistribution.

The fifth rule is restricted visitor access. For sensitive reviews, restrict download and sharing options where appropriate. Founders often default to full access for convenience. During diligence, convenience should not override risk management.

If you are using a Data Room Plus plan, audit logs become important. Audit logs allow you to trace access patterns and document activity during heavier review periods. This is especially useful when multiple buyer-side teams and advisors are involved.

A practical access control checklist for founders:

- start with limited folder access

- enable NDA gating before sharing

- watermark high-risk folders

- restrict downloads for sensitive files

- review access permissions weekly

- remove access immediately when a reviewer leaves the process

The most common mistake founders make is treating security as a one-time setup task. Access control must evolve with the deal. As diligence progresses, new reviewers join, scopes change, and priorities shift. Your data room permissions should follow the same rhythm as the transaction itself.

M&A due diligence FAQ

How long does M&A due diligence usually take for a business?

For most businesses, due diligence takes 3 to 8 weeks. Early-stage or small acquihire-style deals can move faster, while revenue-generating SaaS or multi-entity companies usually take longer because financial, legal, and customer reviews run in parallel. The biggest factor is not company size. It is how prepared your documents are and how quickly your team can answer follow-up questions.

What documents should I prepare before LOI?

Before an LOI, you should already have a light but clean version of your data room ready.

At minimum, prepare your:

- cap table and shareholder structure

- latest financial statements and revenue breakdown

- customer list and major contracts

- IP ownership and key product documentation

- incorporation and governance documents

Founders who wait for the LOI to organize files almost always lose momentum once diligence begins.

What is a financial due diligence checklist?

A financial due diligence checklist is a structured list of financial documents and analyses buyers use to validate your numbers.

It typically includes:

- historical P&L, balance sheet and cash flow

- revenue by product, plan and customer segment

- deferred revenue and contract liabilities

- churn, retention and expansion metrics

- payroll and major operating expenses

- tax filings and outstanding liabilities

The goal is not only to verify revenue, but to confirm how predictable and scalable your business really is.

Do I need a data room for a small acquisition?

Yes, even for a small deal. A data room is less about deal size and more about process discipline. Without a central workspace, files get shared through email, versions get mixed, and access control becomes messy very quickly. For small acquisitions, a simple and well-structured data room is usually enough and saves founders a lot of operational friction.

How much access should I give buyers at the start?

At the start, give access only to:

- financial overview materials

- high-level commercial and customer information

- basic corporate and ownership documents

You should not open HR files, full contracts, or sensitive IP materials on day one. Staged access protects your company and also keeps the buyer focused on the right questions at the right time.

What usually kills a deal during due diligence?

Most deals fail because of trust gaps, not small data errors.

Common deal killers include:

- revenue numbers that cannot be reconciled

- unclear ownership of IP or code

- undisclosed legal or compliance issues

- customer concentration risk that was hidden or minimized

- founders being slow or inconsistent in responses

Once a buyer feels information is being withheld or reshaped, confidence drops very quickly.

Can analytics really help during diligence?

Yes, when used correctly. Analytics show which documents are being reviewed, how often they are opened, and where reviewers spend the most time.

This helps founders anticipate upcoming questions, prepare internal owners early, and identify whether a buyer is actively progressing or stalling. Analytics are not for pressure tactics. They are for better operational planning during the review cycle.

Is a free data room enough for early-stage discussions?

For early conversations and pre-LOI discussions, a free data room is usually enough.

You mainly need:

- clean folder structure

- controlled access

- a single source of truth

Once legal, HR and contract reviews begin, most founders quickly benefit from stronger access control, NDA gating and activity tracking.

How should founders handle multiple buyers at once?

You should use one master data room structure and manage access separately for each buyer group.

This allows you to:

- keep documents consistent

- avoid maintaining multiple versions of the same file

- control which buyer sees which folders

- track review activity independently

Trying to duplicate full data rooms for every buyer almost always leads to version errors and operational overload.

Start organizing your due diligence now. Don’t wait for an LOI. Set up a clean data room. Track buyer activity. Keep control of access.

Author

Anika Tabassum Nionta is a Content Manager at Ellty, where she writes about secure document sharing, virtual data rooms, M&A, due diligence, fundraising, and sales enablement. With over 6 years of writing experience, she helps professionals understand how to share confidential documents securely, track engagement, and manage deals more effectively. Anika holds both a BA and MA in English from Dhaka University. Outside of work, she enjoys reading, exploring new cafes in Dhaka, and connecting with entrepreneurs and dealmakers in her community.