If you're preparing for a fundraise, an acquisition, a consulting engagement, or any deal where sensitive documents need to change hands, someone is going to mention a data room. What most guides skip is that the term means something different depending on which side of the deal you're on.

Whether you're in M&A, real estate, consulting, legal, or finance - the same basic dynamic plays out. One party is sharing information. The other is reviewing it. Both sides have different goals, different information needs, and different data room setups. Confusing the two leads to either over-sharing sensitive information or under-preparing for due diligence - neither of which helps you close a deal.

This guide covers both sides clearly. By the end, you'll know which type of data room you're building, what goes in it, and how to set it up without overcomplicating things.

What does buy side and sell side mean?

Before getting into data rooms, it helps to be clear on the terms.

The sell side is whoever is offering something - a business, a property, a stake in a company, or a service. If you're a startup founder raising a round, a homeowner selling a property, or a consulting firm pitching a client, you're on the sell side. You're the one sharing documents and making the case.

The buy side is whoever is evaluating and potentially acquiring. Private equity firms, strategic acquirers, institutional investors, corporate clients reviewing a proposal - they're all buy side. They're the ones doing the reviewing and deciding.

The terms come from investment banking and M&A, but the logic applies across industries. In real estate, the seller prepares the data room; the buyer's team does due diligence. In consulting, the firm shares credentials and project materials; the client evaluates them. The roles are the same - one side is offering, the other is assessing.

In any deal context, the key question is simple: are you sharing, or are you reviewing? That determines which type of data room you need and how to build it.

What is a sell-side data room?

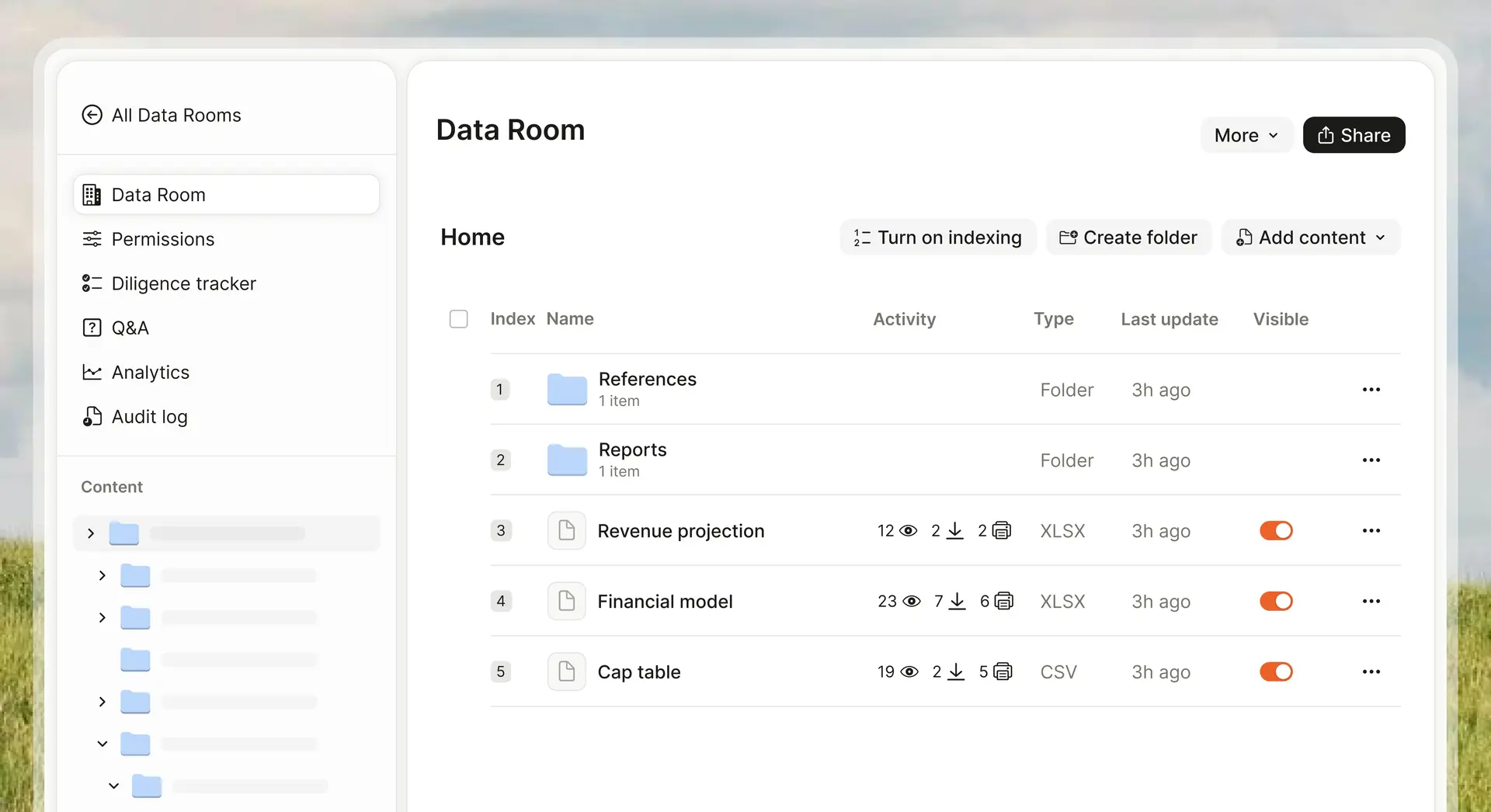

A sell-side data room is where the party sharing information - whether that's a company being acquired, a property being sold, or a firm pitching for a contract - puts all their key documents in one secure place.

You build it. You control it. You decide who gets access, which documents they can see, and when.

The goal is to give the other side enough information to evaluate the deal and move forward - while keeping sensitive details protected if things don't work out. Every document you share is a deliberate choice. You're not handing over everything at once. You're releasing information carefully, as trust builds and the deal progresses.

What goes in a sell-side data room

The exact contents depend on your industry and deal type. An M&A transaction looks different from a real estate sale or a consulting pitch but the principle is the same: share what's needed to build confidence and answer the big questions.

For M&A and fundraising, that typically means financials, legal documents, corporate structure, contracts, and team information. For real estate, it might be title documents, inspection reports, lease agreements, and financial statements. For consulting or professional services, it could be case studies, credentials, proposed scope, and pricing.

You don't need to upload everything on day one. Start with the most commonly requested materials and add more as interest grows. Staged disclosure is standard practice and it protects you.

Who controls the sell-side data room

You do, entirely. You set permissions, decide who sees what, and can require NDA acceptance before anyone views a single document. Different people on the buyer's side can get different levels of access. Their legal team doesn't necessarily need to see what their technical team is reviewing.

Every action inside the data room is tracked. You can see who opened what, and when.

If talks break down, you revoke access immediately. The data room is yours from start to finish.

What is a buy-side data room?

A buy-side data room is less talked about, but just as important - especially in complex deals.

The buy side is whoever is evaluating the opportunity: an acquirer, an investor, a corporate client, or a firm doing due diligence before signing a major contract. During that process, information comes in from everywhere - emails, shared folders, attachments, calls. A buy-side data room pulls it all into one place.

It's an internal workspace. It helps the reviewing team stay organized, track what's been looked at, flag open questions, and keep legal, financial, and commercial teams on the same page.

In larger deals such as private equity acquisitions or big corporate transactions, this is standard practice. The deal team logs everything: documents received from the other side, internal notes, financial models, legal findings, and outstanding items. The buy-side data room becomes the official record of the entire due diligence process.

This isn't limited to M&A. A real estate investor reviewing multiple properties across a portfolio needs the same kind of organized workspace. So does a consulting firm assessing a potential acquisition target on behalf of a client, or a legal team managing a complex transaction across multiple parties.

Buy-side data room use cases

The buy side doesn't control the seller's data room, they request access to it. But they'll often maintain their own parallel workspace to organize what they're learning, track their analysis, and coordinate internally.

Know which side you're on. Set up your sell-side data room on Ellty in minutes - no enterprise contract, no per-user fees. Try it free at ellty.com.

Buy side vs sell side data room: the key differences

Here's the practical breakdown side by side.

If you're preparing for a fundraise, a sale, or pitching for a contract, you're building a sell-side data room. If you're managing due diligence on something you're evaluating or acquiring, you need buy-side infrastructure. Many deals involve both, running at the same time, on opposite sides of the same transaction.

Buy-side vs sell-side due diligence: how they differ

Due diligence looks different from each side of the table.

Sell-side due diligence

On the sell side, due diligence is about preparation and disclosure management. You're anticipating what buyers will ask for and getting ahead of it. The goal is to present your company accurately, answer questions efficiently, and avoid surprises that could derail the deal or reduce your valuation.

Sell-side due diligence has a formal term for this: vendor due diligence (VDD). Some sellers commission an independent report on their own business before going to market. This is more common in larger transactions and gives buyers confidence that the information is accurate and verified.

Even without a formal VDD report, effective sell-side due diligence means:

- Organizing your documents before any buyer asks for them

- Identifying potential red flags early and having a response ready

- Knowing your numbers cold - buyers will probe inconsistencies

- Having clean corporate documentation (cap table, shareholder agreements, board minutes)

- Understanding what's in your contracts, especially change of control provisions

Buy-side due diligence

On the buy side, due diligence is investigative. The buyer's goal is to verify what the seller is claiming, identify risks, and build a picture of what they're actually acquiring.

Buy-side due diligence typically covers:

- Financial due diligence - verifying revenue quality, margins, cash flow, and accounting practices

- Legal due diligence - reviewing contracts, IP ownership, litigation risk, and regulatory exposure

- Commercial due diligence - validating market position, customer relationships, and competitive dynamics

- Technical due diligence - assessing product architecture, code quality, infrastructure, and security

- HR due diligence - reviewing key employee arrangements, retention risk, and equity structures

The buy-side team is looking for the gap between what the pitch said and what the documents show. A well-organized sell-side data room narrows that gap and builds trust. A disorganized one raises flags.

Buy-side vs sell-side in investment banking

In investment banking, buy side and sell side describe entire business models, not just deal positions.

Sell-side investment banking refers to the advisory work banks do to help companies sell themselves, raise capital, or execute transactions. If an investment bank is advising your company on an acquisition exit, they're acting as your sell-side advisor. Their data room work involves setting up the seller's data room, managing document uploads, controlling buyer access, and running the formal Q&A process.

Buy-side investment banking refers to advisory work for the acquirer. Buy-side advisors help companies identify targets, run financial analysis, structure bids, and manage the due diligence process. They often maintain the buy-side data room infrastructure.

For most businesses, sell-side advisors are more relevant - they're the ones hired to run your process if you're raising a growth round or preparing for a strategic exit.

Sell-side vs buy-side research

The terms also appear in equity research, which is adjacent but worth understanding.

Sell-side analysts work at investment banks and brokerage firms. They produce research reports on public companies - buy, hold, or sell recommendations - distributed to institutional clients. Their work is a product sold to investors.

Buy-side analysts work at asset managers, hedge funds, and PE firms. They use sell-side research as one input among many, but their job is to make actual investment decisions. Their research is proprietary - it stays internal.

The practical distinction: sell-side research is published, buy-side analysis is private. In M&A due diligence, both types of analysts may be involved on the buyer's team.

Buy-side vs sell-side private equity

Private equity firms operate on both sides depending on the context.

When a PE firm is acquiring a company, they're on the buy side. Their team will be reviewing your sell-side data room, running financial and legal due diligence, and maintaining their own buy-side workspace to organize findings.

When a PE firm is selling a portfolio company - either to a strategic buyer or in a secondary transaction - they flip to the sell side. They'll build and manage the data room, control disclosure, and run the process the same way a founder would in a direct acquisition.

This is why PE-backed companies often have cleaner data rooms than founder-led companies. PE firms have done this many times. They know what buyers look for and how to present a company's financials and legal documentation in the most favorable, accurate light.

If you haven't been through an M&A process before, the quality of your data room is one of the clearest signals of your operational maturity. Buyers notice.

Buy-side and sell-side examples

These examples make the distinction concrete.

Example 1: Series B fundraise

A SaaS startup is raising a $20M Series B. A tier-one VC is in late-stage due diligence. The founder builds a sell-side data room with financials, cap table, customer contracts, and product documentation. The VC's deal team - three partners and two associates - accesses the room, reviews documents, and tracks open questions. The founder monitors who's reading what through the data room analytics. The VC maintains an internal workspace (their buy-side equivalent) to consolidate findings and build their investment memo.

Example 2: Strategic acquisition

A larger SaaS company is acquiring a smaller competitor. The target (sell side) builds a data room and shares access with the acquirer's legal and finance teams. The acquirer (buy side) maintains their own deal management workspace where they log diligence findings, track open issues, and coordinate across workstreams. Both sides are using "data rooms," but for completely different purposes.

Example 3: PE-backed exit

A PE firm is running a sale process for one of its portfolio companies. They build a full sell-side data room, including audited financials, a management presentation, a customer pipeline summary, and an information memorandum. Multiple potential buyers access the room in a controlled auction process. Each buyer maintains their own buy-side workspace to compare the target against other opportunities in their pipeline.

What features matter on each side

The feature requirements are different depending on your role.

Sell-side data room features that matter most

Buy-side data room features that matter most

Most VDR platforms are built primarily for the sell side.

How Ellty handles sell-side data rooms

Ellty is built for teams running sell-side processes - fundraising rounds, early acquisition conversations, formal M&A due diligence, a consulting engagement, or any deal where confidential documents need to change hands.

Here's what the platform covers:

Upload and organize documents across folders with clean, intuitive structure. Create trackable sharing links for pitch decks and sensitive materials before you even set up a formal data room. See exactly who opened your document, which pages they read, and how long they spent on each section - in real time.

When you're ready to move, Ellty Data Room plan ($149/month) adds NDA gating before visitors can access any documents, dynamic watermarking on sensitive files, granular permissions by user and folder, and restricted visitor access. The Data Room Plus plan ($349/month) adds group visitor permissions, full audit logs, and support for up to 4,000 assets per data room.

There's no per-user pricing. You pay a flat monthly rate regardless of how many investors or acquirers join the process. That matters when deals involve five or six counterparties, each with a team of two or three reviewers.

Where Ellty works well:

- You want a branded, professional data room without a complex setup or a sales call to get started

- You're running a seed or Series A process with up to a few dozen investors

- You're a consultant, broker, or advisor who shares sensitive documents with clients regularly and wants something more professional than email attachments

- You need NDA gating and watermarking but don't want to pay enterprise prices to get them

- You're managing a real estate transaction and need to share property documents with multiple parties in a controlled, organized way

- You want one platform that handles both pitch deck sharing and full due diligence — without switching tools

- You're a small or mid-sized business going through an acquisition and need a clean, organized room without the overhead of enterprise software

Where you'd want something else:

- Very large, complex transactions managed by bulge-bracket investment banks

- Deals requiring advanced multi-party Q&A workflow management

- Tens of thousands of documents requiring enterprise-scale indexing

Ellty is direct about its scope. It's not trying to replace Datasite for a $500M acquisition. It's built for teams who needs a professional, functional data room fast - without months of onboarding or an enterprise contract.

Common mistakes on each side of the deal

Sell-side mistakes

Waiting too long to set up the data room. Buyers move fast once they're interested. If your documents aren't organized when they ask, you lose momentum and signal that you're not ready.

No staged disclosure. Dropping everything into the room at once is a mistake. Put your change-of-control clauses and detailed cap table mechanics in front of buyers only when you're confident they're serious.

Skipping the NDA gate. Even in friendly deals, require NDA acceptance before granting access. It creates a legal record and forces the counterparty to formalize their intent.

Not reading the analytics. Your data room is telling you something. If a buyer's team has spent three sessions reviewing your customer contracts and hasn't asked a single question about them, find out why. The analytics give you information most founders ignore.

Buy-side mistakes

No internal organization. Receiving documents from a sell-side data room without a structured way to organize and review them leads to missed issues and duplicated work across the team.

Reviewing too fast. Under time pressure in competitive auctions, buy-side teams sometimes rush through legal and financial review. This is how unfavorable contract terms and accounting irregularities get missed.

Not tracking open questions. Every due diligence process generates questions that need answers. If you're not logging them systematically, things fall through the cracks.

FAQ: buy side vs sell side data room

What is the difference between a buy-side and sell-side data room?

A sell-side data room is built by whoever is sharing information - a company raising capital, a business being acquired, a property being sold, or a firm pitching for a contract. It's a controlled space where you share documents with the other side on your own terms. A buy-side data room is maintained by whoever is doing the reviewing - an acquirer, investor, corporate client, or due diligence team. It's an internal workspace to organize everything they're collecting and analyzing during the process. Both are called "data rooms" but they serve opposite purposes. One is about controlled sharing. The other is about organized reviewing. In many deals, both exist at the same time - on opposite sides of the same table.

Which side builds the data room in M&A?

Both sides can maintain a data room, but the seller typically builds the primary one. The sell-side data room is where confidential documents are shared, access is controlled, and disclosure is managed. The buy side may maintain a separate internal workspace to organize what they're receiving and reviewing.

What is buy-side due diligence?

Buy-side due diligence is the investigative process an acquirer or investor runs on a target company. It covers financial, legal, commercial, technical, and HR workstreams. The goal is to verify what the seller is claiming, identify risks, and determine what the company is actually worth.

What is sell-side due diligence?

Sell-side due diligence is the preparation work a company does before going to market or entering formal due diligence with a buyer. It involves organizing documentation, identifying potential issues, and presenting the business accurately. A formal sell-side due diligence report (vendor due diligence) is sometimes commissioned by the seller before the process begins.

What is buy-side vs sell-side in investment banking?

In investment banking, sell-side refers to banks and advisors that help companies raise capital or sell themselves. Buy-side refers to asset managers, PE firms, and acquirers that deploy capital. A sell-side M&A advisor manages your sale process and data room. A buy-side advisor helps an acquirer identify targets and run diligence.

What is the difference between buy-side and sell-side research?

Sell-side research is produced by investment bank analysts and distributed to institutional clients. It's a product. Buy-side research is produced internally at funds and PE firms to inform investment decisions. It's proprietary. In M&A due diligence, buy-side analysts use both as inputs.

What goes in a sell-side data room?

A typical sell-side data room includes corporate structure documents, financial statements (3 years plus forecasts), legal contracts, IP documentation, employee agreements, customer contracts, and tax records. Documents are staged - start with the most commonly requested materials and add depth as buyer confidence increases.

Do startups need a sell-side data room for fundraising?

Not always. For early seed rounds with a handful of angel investors, a tracked secure link is often enough. For Series A and later, institutional investors typically expect a proper data room with organized documentation and controlled access. The more investors are involved simultaneously, the stronger the case for a formal VDR.

What is vendor due diligence (VDD)?

Vendor due diligence is a report commissioned by the sell side - the company being sold - rather than the buyer. An independent advisor reviews the company's financials, legal structure, and operations and produces a report that buyers can rely on. It's more common in larger transactions and in PE-backed exits. It speeds up the buyer's diligence process and signals that the seller has nothing to hide.

How does Ellty support sell-side data rooms?

Ellty lets teams upload documents, create a structured data room with folder-level permissions, require NDA acceptance before access, add dynamic watermarks to sensitive files, and track exactly who viewed which documents and for how long. The Data Room plan starts at $149/month with no per-user fees. There's also a free plan for teams who want to start with pitch deck sharing and document analytics before a formal data room is needed.

Start building your sell-side data room on Ellty today. Free plan available. No credit card needed. Go to ellty.com.

Final word

The buy side and sell side have different jobs in a deal. The sell side is presenting and protecting. The buy side is investigating and evaluating. Both need organized, secure access to information - but the tools and workflows look different.

If you're a business owner, you're almost certainly building a sell-side data room. Get it organized before buyers ask for it. Use a platform that gives you document-level analytics so you know what they're reading. Gate it with an NDA. And pay attention to what the activity data is telling you.

That's the difference between teams who control their deal process and those who react to it.

Author

Anika Tabassum Nionta is a Content Manager at Ellty, where she writes about secure document sharing, virtual data rooms, M&A, due diligence, fundraising, and sales enablement. With over 6 years of writing experience, she helps professionals understand how to share confidential documents securely, track engagement, and manage deals more effectively. Anika holds both a BA and MA in English from Dhaka University. Outside of work, she enjoys reading, exploring new cafes in Dhaka, and connecting with entrepreneurs and dealmakers in her community.