Private equity deals move fast. There's a lot of money on the table, a lot of people involved, and very little room for error. That's why due diligence isn't just a box to check before signing. It's the process that tells you whether the deal you're excited about is actually worth doing.

This guide breaks down what due diligence looks like in private equity, what you need to look at, how long it takes, and how to run the whole thing without losing your mind or your data.

What is due diligence?

Due diligence is simply the process of verifying everything before you commit to a deal.

Before a private equity firm puts money into a company, it needs to confirm that what the seller is saying is actually true. Is the business performing the way it claims? Are there any hidden debts, legal issues, or operational problems? Is the management team credible? Are the financials clean?

Due diligence answers all of these questions by doing a deep, structured review of the target company. It covers finances, legal agreements, operations, market position, people, and technology. The goal isn't just to confirm that the deal looks good. It's to understand exactly what you're buying, at what risk, and for what price.

Think of it like a home inspection before you buy a property. You wouldn't sign the paperwork before knowing if the roof leaks or the foundation is cracked. Due diligence does the same thing for businesses.

Why due diligence is critical in private equity

In private equity, you're not buying a share of a public company that you can sell tomorrow if something goes wrong. You're making a concentrated, illiquid bet on a business for the next 5 to 7 years. If something goes wrong after you've closed the deal, you own that problem.

That's why due diligence matters so much.

It protects you from overpaying. If the numbers don't hold up under scrutiny, you can renegotiate the price or walk away entirely.

It surfaces risks early. Legal disputes, customer concentration, regulatory issues, or key person dependency are things you'd rather know about before you wire the money.

It builds the investment case. Good due diligence doesn't just look for problems. It also confirms the growth story, validates the market opportunity, and gives you the data you need to build a post-acquisition plan.

It protects your LPs. When you're deploying investor capital, you have a responsibility to do the work. Skipping or rushing due diligence isn't just bad practice. In some cases, it can be a breach of your fiduciary duty.

Simply put, the deals that go bad are usually the ones where due diligence was rushed, incomplete, or skipped altogether.

How long is the due diligence period in private equity?

There's no single answer to this. The timeline depends on the size and complexity of the deal.

For smaller transactions, due diligence might take 4 to 6 weeks. For mid-market deals, you're typically looking at 6 to 12 weeks. For larger, more complex acquisitions, it can stretch to 3 to 4 months or longer.

Here's a rough breakdown of what affects the timeline:

The size of the business matters. A company with 10 employees and clean books takes far less time to review than one with 300 employees, multiple subsidiaries, and operations across different countries.

The quality of documentation also plays a big role. If the target company has well-organized financial records, up-to-date legal agreements, and clear HR documentation, the process moves quickly. If they're hunting for contracts and reconciling spreadsheets, it slows everything down.

The number of workstreams running in parallel affects pace too. Large deals involve financial, legal, commercial, operational, and technical reviews, often running at the same time with different teams. Coordinating all of that takes time and good systems.

A virtual data room helps significantly here. When documents are organized, permissions are set, and everyone can access what they need without going back and forth, the timeline tightens up considerably.

If you're managing a deal and want to keep due diligence on track, Ellty data room plans start from just $149/month. No per-user fees, no complicated setup - just a clean, secure environment where your deal team can get to work immediately.

Key areas of focus

Private equity due diligence is broad. Here's what a serious review typically covers.

Financial due diligence

This is where most teams start. You're looking at historical financial statements, revenue trends, margin structure, working capital cycles, and quality of earnings. The goal is to separate recurring, predictable revenue from one-time items and understand the real earnings power of the business.

Legal due diligence

Lawyers review contracts, corporate structure, IP ownership, regulatory compliance, litigation history, and any pending claims. A clean legal review gives buyers confidence. Any red flags here, such as a dispute with a major customer or unclear IP ownership, need to be resolved before closing.

Commercial due diligence

Commercial due diligence focuses on the market. Is the industry growing? How strong is the company's competitive position? What does the customer base look like? How dependent is the business on a small number of clients? Commercial due diligence validates the investment thesis.

Operational due diligence

Here you're looking at how the business actually runs day-to-day. Supply chain, manufacturing processes, technology systems, and operational efficiency. You want to identify areas of strength and any bottlenecks that could slow down value creation post-acquisition.

HR and management due diligence

The quality of the team matters. You're assessing leadership, retention risk, compensation structures, employment contracts, and any HR-related liabilities. In PE, backing the right management team is often what makes or breaks a deal.

Technology due diligence

For any business that relies on proprietary software, platforms, or IT infrastructure, a technical due diligence is essential. You're looking at code quality, cybersecurity posture, scalability, and any technical debt that could require significant investment down the road.

Virtual data rooms: the backbone of private equity due diligence

If there's one piece of infrastructure that private equity due diligence absolutely depends on, it's the virtual data room (VDR).

A VDR is a secure online repository where the target company uploads documents and the buyer's due diligence team reviews them. It replaces the old physical data room model, where advisors literally had to travel to a location to review printed files. Today, the whole process happens online, securely and efficiently.

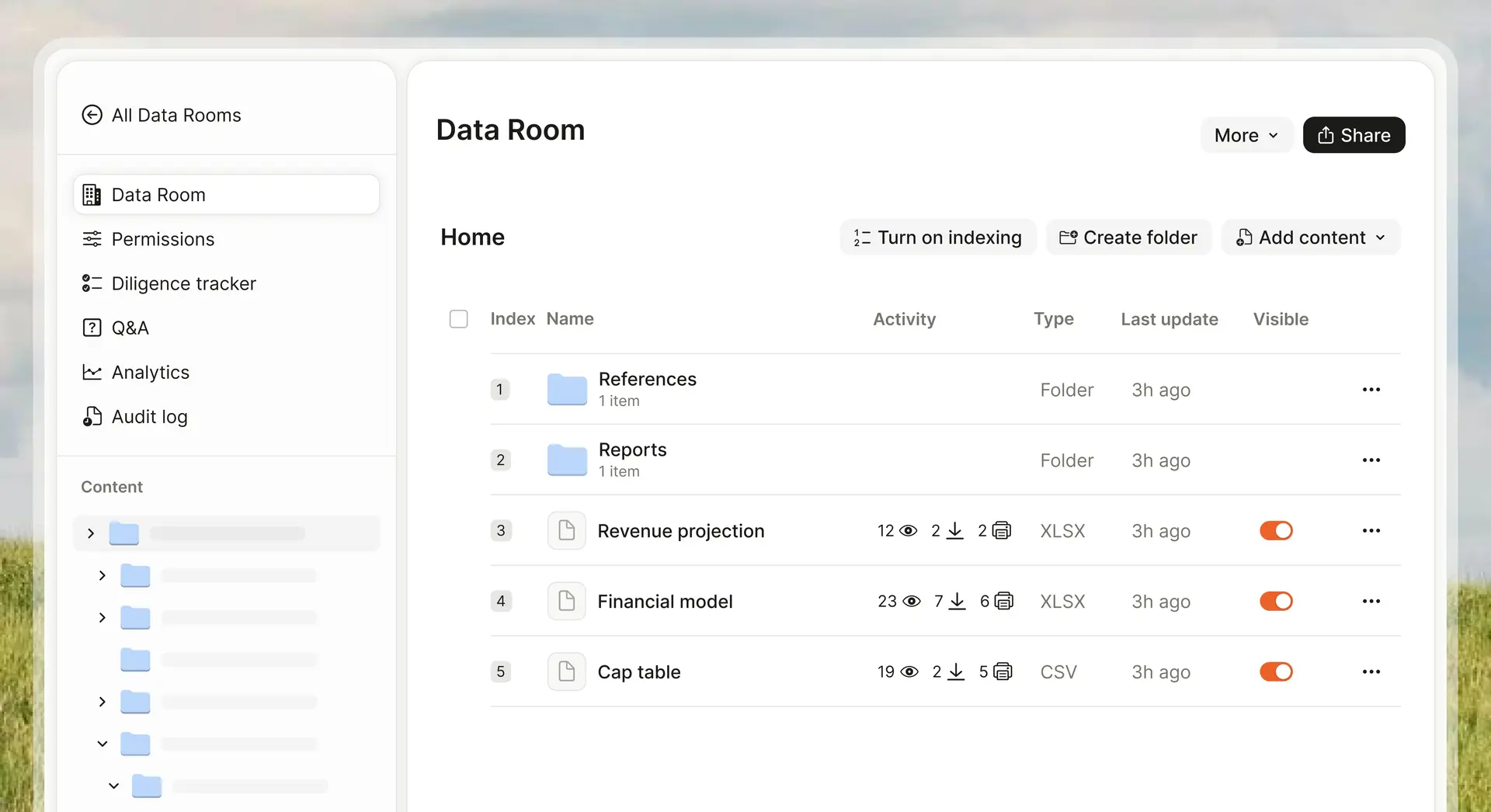

In a proper PE deal, the data room is where hundreds or even thousands of documents live. Financial statements, legal contracts, board minutes, IP agreements, customer contracts, HR files, and more. Different members of the deal team need access to different parts of it. External advisors need to be let in. Unauthorized people need to be kept out.

This is exactly what Ellty is built for.

Ellty is a secure document sharing and analytics platform with full data room functionality. It gives PE deal teams the core tools that matter during due diligence: granular access controls, real-time activity tracking, NDA gating, dynamic watermarking, and a clean audit trail. You can see who opened what, when, for how long, and from where.

What sets Ellty apart from the legacy platforms is the pricing model. There are no per-user charges, no per-page fees, and no enterprise contracts that take weeks to negotiate. You pick a plan, get set up quickly, and know exactly what you're paying.

For PE teams, this matters because deal teams are often lean, timelines are tight, and you don't want to spend days setting up infrastructure before you can even start reviewing documents.

Here's how the plans work for different deal sizes:

The Free plan is a good starting point if you're in early conversations and want to see who is opening documents before setting up a full data room. It covers document tracking, real-time analytics, and secure sharing at no cost.

The Standard plan at $69/month gives you unlimited documents, advanced analytics, eSignatures, custom branding, and data room features. It works well for smaller deals and ongoing investor communication.

The Room plan at $149/month is where the full VDR feature set comes in. Granular permissions, NDA gating, dynamic watermarking, and restricted visitor access. Everything you need to run a controlled due diligence process.

The Room Plus plan at $349/month adds group visitor permissions, full audit logs, and support for up to 4,000 assets per data room. Built for heavier document loads and multi-party deals where you need structured access control across different groups of reviewers.

Process and stages

A typical private equity due diligence process moves through several stages.

Stage 1 - Preliminary review

Before the formal process begins, the buyer reviews a Confidential Information Memorandum (CIM) or similar document from the seller. This gives a high-level picture of the business, its financial performance, and the opportunity. If the buyer is interested, they move forward and sign an NDA.

Stage 2 - Data room setup and access

The seller prepares the data room and populates it with requested documents. Using a platform like Ellty, you can set up NDA gating so reviewers must acknowledge the terms before accessing any files. Access is tiered based on role.

Stage 3 - Document review and Q&A

The buyer's team reviews the documents in detail. Questions are submitted through a structured Q&A process. The seller's team responds and uploads additional documents as needed. This back-and-forth is the core of the due diligence process.

Stage 4 - Management meetings

In parallel or after the document review, the buyer meets with the management team of the target company. These conversations help validate what's in the documents and give the buyer a feel for the leadership team.

Stage 5 - Final report and decision

The due diligence findings are compiled into a report. The deal team reviews the findings, assesses the risks, and decides whether to proceed, renegotiate terms, or walk away.

Private equity due diligence checklist

This is a practical checklist covering the key areas you'll want to review. It's not exhaustive, but it covers the essentials.

Financial

- Audited financial statements for the past 3-5 years

- Monthly management accounts for the current year

- Revenue breakdown by customer, product, and geography

- Cost structure and margin analysis

- Working capital analysis

- Capital expenditure history and projections

- Debt schedule and outstanding obligations

- Tax compliance and open assessments

Legal

- Corporate structure and entity documents

- Shareholder agreements

- All material contracts with customers, suppliers, and partners

- Intellectual property ownership and registrations

- Employment contracts and non-competes

- Litigation history and pending claims

- Regulatory licenses and compliance documentation

- Insurance policies

Commercial

- Market size and growth data

- Competitive landscape analysis

- Customer contracts and retention data

- Sales pipeline and forecasts

- Pricing history and strategy

- Customer concentration analysis

Operational

- Organizational chart and headcount

- Key operational processes and systems

- Technology infrastructure and software licenses

- Supply chain and supplier agreements

- Facilities and lease agreements

HR and management

- Management team bios and employment terms

- Employee turnover data

- Benefit plans and pension obligations

- Any HR disputes or open claims

Technology

- IT infrastructure overview

- Proprietary software and code ownership

- Cybersecurity policies and any past incidents

- Data privacy compliance (GDPR, CCPA, etc.)

Want to organize and share your due diligence documents securely? Ellty Room plan gives you everything you need - NDA gating, granular permissions, and real-time tracking - for $149/month. No per-user fees, no surprises.

Developing an exit strategy

Due diligence isn't only about the entry. Experienced PE firms think about the exit from the very beginning.

Before you close a deal, you should already have a view on how you'll eventually exit. This means thinking about potential buyers, IPO feasibility, and what the business needs to look like in 5 years to attract a premium valuation.

An exit strategy built during due diligence shapes everything that follows. It determines what operational improvements to prioritize. It informs the management incentive structure. It guides how you present the business to future buyers down the road.

Common exit routes for PE-backed companies include strategic sale to a trade buyer, secondary sale to another PE firm, recapitalization, and in some cases, an IPO. Understanding which path is most realistic given the company's size, market, and growth profile should be part of the initial due diligence assessment.

Due diligence findings directly impact exit planning. If you discover that the company is heavily dependent on one customer during due diligence, that's a risk you'll need to address before you can command a premium exit multiple. If you find that the technology infrastructure is outdated, that's a capital investment you need to plan for in your return model.

Good exit planning is just good investing. The firms that consistently generate strong returns are the ones that know what they're building toward before the ink on the acquisition is dry.

Frequently asked questions

What is the difference between due diligence in private equity and in M&A?

The principles are the same, but the focus can differ. In private equity, the commercial and financial due diligence tends to go deeper because the PE firm is making a long-term operational bet on the business, not just a strategic one. There's also more emphasis on management quality and the post-acquisition value creation plan.

What is a virtual data room and why do PE firms use it?

A virtual data room is a secure online platform for sharing and reviewing confidential documents. PE firms use them because due diligence involves sharing thousands of sensitive files across multiple parties, and you need a system that controls access, tracks activity, and keeps everything organized. Ellty offers full VDR functionality with flat-rate pricing, starting from $149/month for the Room plan.

Can due diligence findings change the deal price?

Absolutely. It happens regularly. If due diligence uncovers risks or liabilities that weren't disclosed upfront, the buyer can renegotiate the price downward, request an indemnity, or in some cases walk away. This is one of the main reasons thorough due diligence protects deal value.

What happens if something is missed during due diligence?

That depends on what was missed and whether it was disclosed. If the seller deliberately withheld material information, there may be legal remedies. If it was simply missed due to an incomplete review, the buyer typically bears the consequences. This is why having a thorough, organized process with the right tools matters.

How many people are typically involved in a PE due diligence process?

It varies significantly. A small deal might have a team of 5-10 people across financial, legal, and commercial workstreams. A large transaction can involve 50 or more people across multiple advisory firms. A good data room makes it manageable regardless of team size, and with Ellty flat-rate pricing, adding more users doesn't add more cost.

What documents should a seller prepare before due diligence begins?

At a minimum: audited financials for the past 3-5 years, current year management accounts, a complete contract register, corporate documents, tax records, and any material correspondence relevant to the business. The more organized and complete the data room is from day one, the smoother and faster the process will be.

Is due diligence always done before signing, or can it happen after?

Typically, due diligence is done before signing the purchase agreement, though sometimes a deal is signed subject to completion of diligence. In competitive auction processes, buyers sometimes have to sign with limited diligence and complete the review after signing but before closing. This approach carries more risk and requires strong legal protections.

Final thoughts

Due diligence is not the exciting part of private equity. It's the slow, methodical, detail-heavy work that happens between the initial excitement of a deal and the moment you sign. But it's the work that determines whether you actually make money.

Skipping steps, rushing the timeline, or working with inadequate tools introduces risk that can take years to show up and even longer to recover from.

The firms that do this well share a few things in common. They have a clear process. They use the right technology. They treat due diligence not as a formality but as the foundation of the investment.

If you're looking for a VDR that makes the document side of due diligence more organized, secure, and efficient, Ellty is worth a look. Flat pricing, no per-user fees, and full VDR functionality from $149/month. You can be set up and running in a matter of hours, not weeks.

Author

Anika Tabassum Nionta is a Content Manager at Ellty, where she writes about secure document sharing, virtual data rooms, M&A, due diligence, fundraising, and sales enablement. With over 6 years of writing experience, she helps professionals understand how to share confidential documents securely, track engagement, and manage deals more effectively. Anika holds both a BA and MA in English from Dhaka University. Outside of work, she enjoys reading, exploring new cafes in Dhaka, and connecting with entrepreneurs and dealmakers in her community.