The Canadian fintech market hit USD $5.5B in 2026, up from $4.38B in 2024. These 15 investors - from dedicated fintech funds to BC's provincial capital - are actively writing checks into Vancouver fintech companies right now.

Vancouver's fintech funding has two clear entry points. The first is specialist fintech capital — Luge Capital, Conconi Growth Partners — that understands regulatory nuance, banking partnerships, and the difference between a real payments moat and a wrap around an existing rails provider. The second is BC generalists — Version One Ventures, Rhino Ventures, TELUS Ventures — that back fintech alongside other sectors when the unit economics are clear.

You don't pitch them the same way. Luge wants to know your banking partner, your regulatory status, and why a chartered bank can't replicate your product in 18 months. Version One wants to see traction and network effects. Know which meeting you're in before you walk in.

Vancouver fintech companies have built real exits. Mogo, the Vancouver digital finance company, has $9.9B in annual payments volume. The Nuvei take-private in 2024 at $6.3B showed Canadian fintech can scale to global scale. Payfare's acquisition by Fiserv in 2025 confirmed the appetite for Canadian payments infrastructure. The capital is following the track record.

Set up your materials before reaching out to any of these 15 investors. Read what documents go in a data room so you're ready when the first partner asks.

| Stage | Check size | Sector focus | Contact | |

|---|---|---|---|---|

| Luge Capital | Pre-seed, Seed, Series A | CA$250K-$2M | Fintech, insurtech, wealthtech | luge.vc |

| TELUS Ventures | Series A, Series B, Series C | $5M-$100M | Fintech, payments, enterprise software | telus.com/en/ventures |

| Version One Ventures | Pre-seed, Seed | $250K-$2M | Fintech, crypto, marketplace, B2B | versionone.vc |

| Rhino Ventures | Series A | $2M-$10M | B2B fintech software, SaaS | rhinoventures.ca |

| Conconi Growth Partners | Pre-seed, Seed | $500K-$3M | Fintech, healthcare, BC tech | conconi.ca |

| InBC Investment Corp. | Seed, Series A | $2M-$15M | Fintech, deep tech, AI | inbcinvestment.com |

| BDC Capital | Seed, Series A | $500K-$5M | Cross-sector fintech, B2B software | bdc.ca |

| Yaletown Partners | Seed, Series A, Growth | $1M-$15M | Fintech software, data, enterprise | yaletown.com |

| Vanedge Capital | Seed, Series A, Series B | $1M-$15M | Hard tech, AI, enterprise software | vanedgecapital.com |

| Pender Ventures | Series A, Series B | $2M-$15M | B2B fintech software, healthtech | penderventures.com |

| Export Development Canada (EDC) | Series A, Series B | $5M-$50M | Export-ready fintech, payments infra | edc.ca |

| VANTEC Angel Network | Pre-seed, Seed | $50K-$500K | BC tech, fintech, digital services | vantec.ca |

| WUTIF Capital (VCC) | Pre-seed, Seed | Up to $500K | BC tech, fintech, SaaS | wutif.com |

| GTMfund | Pre-seed, Seed | $500K-$1.5M | B2B SaaS, fintech software, go-to-market | gtmfund.com |

| Garage Capital | Pre-seed, Seed | $250K-$1M | B2B SaaS, fintech, marketplaces | garage.vc |

Track who opens your fintech pitch

Upload your deck to Ellty and send trackable links. See which Vancouver VCs open your materials and which slides they spend the most time on.

Start free 14-day trialWhat is a Vancouver fintech investor?

A Vancouver fintech investor backs founders building payments infrastructure, lending platforms, wealthtech, insurtech, and financial data companies. They differ from generalist VCs because they evaluate regulatory pathway, banking partnerships, and unit economics of customer acquisition in a compliance-heavy environment.

Check sizes run from $50K angel checks at VANTEC to $100M+ at TELUS Ventures. Most first institutional fintech rounds in Vancouver land between $500K and $3M at seed. Getting to Series A requires demonstrated customer traction, clear gross margin, and either a banking partner agreement or a fintech licence in hand.

Most investors who've been burned by fintech companies will tell you the same thing: the biggest risk isn't the product, it's the compliance cost. If you haven't modelled your FINTRAC, PCI-DSS, or OSC compliance costs into your burn, you're pitching a number investors won't believe.

For context on how these investors review your materials, read how to build a better investor portal. Use Ellty to share your pitch as a trackable link — you'll see who opens your financial model before your next call. For broader Canadian fintech capital, check the Toronto fintech investors list.

$19T AUM in alternative assets. 10% annual growth since 2017. $33T+ projected by 2030. That's the fintech opportunity.

15 top Vancouver fintech investors in 2026

1. Luge Capital

The most active specialist fintech VC in Western Canada. Based in Montreal with strong Vancouver presence, Luge closed Fund II at $96M CAD in September 2024, backed by CDPQ, BDC Capital, Sun Life, Desjardins, and iA Financial Group. They focus on pre-seed to Series A fintech across Canada and the US.

- Recent Deals: Velix CA$2M pre-seed lead (February 2026, fintech OS for logistics); Cybrid US$10M Series A participation (October 2025, stablecoin and fiat payment rails); ProNavigator acquired by Guidewire (November 2025, exit); 44 investments total; $180M+ AUM

- LinkedIn: Luge Capital LinkedIn

- Sector Focus: Payments, insurtech, wealthtech, regtech, banking infrastructure

- Stage Focus: Pre-seed, Seed, Series A

- Location: Montreal / Vancouver

- Website: luge.vc

2. TELUS Ventures

TELUS's corporate VC arm is headquartered in Vancouver with 57 portfolio companies. For fintech founders building payments infrastructure, IoT financial services, or enterprise financial platforms, TELUS can open commercial partnerships with a $20B+ revenue telecom network.

- Recent Deals: Waabi $750M Series C participation (January 2026); CubeWorks investment (November 2025); past portfolio includes Mogo, Taulia (acquired by SAP), and Veracode; 3 new investments in past 12 months; 1 unicorn, 21 acquisitions across portfolio

- LinkedIn: TELUS Ventures LinkedIn

- Sector Focus: Fintech, payments, IoT, enterprise platforms, healthtech

- Stage Focus: Series A, Series B, Series C

- Location: Vancouver, BC

- Website: telus.com/en/ventures

3. Version One Ventures

Boris Wertz's Vancouver seed fund backed Coinbase and Uniswap from early stages. In 2025-2026 Version One is explicitly focused on AI, Web3, and fintech infrastructure. They've made 3 investments in early 2026 and have 6 unicorns in their portfolio. The fastest path to a US fintech follow-on in BC is through Version One's LP and co-investor network.

- Recent Deals: Swoop investment (2026); Moment Energy follow-on (2026); 6 investments in 2025; active Fund VI deployment; portfolio includes Coinbase, Uniswap, Ada; $250M+ AUM; 100+ portfolio companies

- LinkedIn: Version One Ventures LinkedIn

- Sector Focus: Fintech, crypto, Web3, marketplace, B2B software

- Stage Focus: Pre-seed, Seed

- Location: Vancouver, BC

- Website: versionone.vc

4. Rhino Ventures

Vancouver's high-conviction Series A fund with $120M Fund III raised to invest beyond Western Canada. They backed Thinkific and Ontopical. For fintech founders building B2B financial software with SaaS metrics, Rhino is the most accessible local Series A fund in BC.

- Recent Deals: ShopVision seed (September 2025); Ontopical acquisition by SOVRA (August 2025); Thinkific secondary sale June 2025 (Rhino retains ~15% stake); 27 portfolio companies with 2 IPOs and 8 acquisitions; $120M Fund III

- LinkedIn: Rhino Ventures LinkedIn

- Sector Focus: B2B fintech software, enterprise SaaS, digital products

- Stage Focus: Series A

- Location: Vancouver, BC

- Website: rhinoventures.ca

5. Conconi Growth Partners

Vancouver-based early-stage investor focused on fintech and healthcare. They backed Requity Homes (proptech-fintech, $26M raised) and HonestDoor (property valuations). For BC-based fintech founders at pre-seed or seed stage who need a local champion before the national funds show up, Conconi is your first call.

- Recent Deals: Requity Homes participation ($26M total raised, Toronto proptech-fintech); HonestDoor seed participation (Edmonton, property valuation fintech); 2 investments in past 12 months; active BC fintech and healthcare deployment

- LinkedIn: Conconi Growth Partners LinkedIn

- Sector Focus: Fintech, healthcare, BC early-stage tech

- Stage Focus: Pre-seed, Seed

- Location: Vancouver, BC

- Website: conconi.ca

Send your fintech deck with trackable links

Set up an Ellty data room before your first investor meeting. Know exactly who opens your pitch and which slides they review.

Start free 14-day trial6. InBC Investment Corp.

BC's $500M provincial fund co-invests alongside every major BC fintech investor on this list. They've backed 38 BC companies including Novarc, Sanctuary AI, and Amplitude Ventures as a fund LP. For BC-based fintech companies, InBC is the first provincial check and brings government relationships relevant to regulatory pathways.

- Recent Deals: UBC Catalyst Ventures Fund co-anchor $10M (March 2026); Vanedge Fund IV $10M LP (March 2025); 38 BC companies in portfolio; $81M invested in FY 2024/25; actively seeking BC-owned fintech deals

- LinkedIn: InBC Investment Corp. LinkedIn

- Sector Focus: Fintech, deep tech, AI, cleantech, life sciences

- Stage Focus: Seed, Series A (also LP in VC funds)

- Location: Vancouver, BC

- Website: inbcinvestment.com

7. BDC Capital

Canada's most active co-investor. BDC backs fintech companies across all stages and co-invests with most funds on this list. For Vancouver fintech founders, BDC is often the bridge check that lets you close a round while your lead investor runs diligence. They won't lead, but they'll move fast on a co-investment.

- Recent Deals: $150M Life Sciences Fund launched April 2026; continuous deployment across BC fintech and software; 384+ total investments; portfolio companies have raised $3.5B+ in additional capital; LP in Luge Capital Fund II

- LinkedIn: BDC Capital LinkedIn

- Sector Focus: Cross-sector fintech, B2B software, enterprise tech

- Stage Focus: Seed, Series A (also pre-seed and growth)

- Location: Vancouver, BC (national mandate)

- Website: bdc.ca

8. Yaletown Partners

Vancouver's $600M AUM generalist fund. Not a dedicated fintech investor, but their Intelligent Industry thesis covers financial data and enterprise platforms. Mogo was in their portfolio, and they've backed enterprise software companies with fintech adjacencies. For fintech companies with a clear enterprise sales motion, Yaletown is worth approaching.

- Recent Deals: GHGSat $47M Series C participation (September 2025); Nanoprecise $38M Series C lead (2025); IGF III $100M first close (July 2025); 20+ exits across software and industrial tech

- LinkedIn: Yaletown Partners LinkedIn

- Sector Focus: Enterprise software, financial data, industrial AI, analytics

- Stage Focus: Seed, Series A, Growth

- Location: Vancouver, BC

- Website: yaletown.com

9. Vanedge Capital

Vancouver's most technical early-stage fund. Vanedge goes deep on enterprise software, AI infrastructure, and analytics — all of which overlap with fintech infrastructure plays. D-Wave and Electronic Arts are in their portfolio. For fintech founders building proprietary financial AI or data infrastructure, Vanedge is a realistic lead.

- Recent Deals: NeuroBionics $10M seed co-lead (December 2025); Mojo Vision $75M Series B Prime participation (September 2025); Fund IV with InBC $10M LP commitment (March 2025); $500M+ AUM across four funds

- LinkedIn: Vanedge Capital LinkedIn

- Sector Focus: Enterprise software, AI infrastructure, analytics, hard tech

- Stage Focus: Seed, Series A, Series B

- Location: Vancouver, BC

- Website: vanedgecapital.com

10. Pender Ventures

Vancouver's Series A specialist. Maria Pacella's $150M AUM fund backed DrugBank and Jane Software. They're not primarily fintech, but Pender backs B2B software with strong unit economics — and fintech B2B with clear NRR fits their thesis. Their most recent investment was Science&Humans in January 2026.

- Recent Deals: Science&Humans $10M Series A (January 2026); Engineered Intelligence Series A (April 2026); Veritree $6.5M Series A co-lead with Garage Capital (May 2025); $150M AUM; InBC and Alberta Enterprise as LPs

- LinkedIn: Pender Ventures LinkedIn

- Sector Focus: B2B fintech software, enterprise software, healthtech

- Stage Focus: Series A, Series B

- Location: Vancouver, BC

- Website: penderventures.com

11. Export Development Canada (EDC)

Underused by fintech founders. EDC writes equity checks alongside debt for Canadian fintech companies with clear US or international expansion plans. For Vancouver payments or lending companies with a US go-to-market strategy, EDC is a realistic co-investor at Series A and above.

- Recent Deals: Novarc $50M Series B lead (March 2025); GHGSat Series C participation (September 2025); continuous co-investment in BC tech with export potential; national mandate focused on global commercialization

- LinkedIn: Export Development Canada LinkedIn

- Sector Focus: Export-ready fintech, payments infrastructure, financial software

- Stage Focus: Series A, Series B (equity plus debt)

- Location: Ottawa, ON (active Vancouver deal flow)

- Website: edc.ca

12. VANTEC Angel Network

BC's primary gateway for pre-seed fintech capital. VANTEC connects founders with 300+ accredited BC angel investors, many of whom have built or exited financial services companies. For fintech founders who need $250K to $500K before institutional capital shows up, VANTEC is the most structured path in Vancouver.

- Recent Deals: Ongoing cohort-based investment rounds; 300+ accredited angel investors across BC; regular fintech, healthtech, and software investment presentations; connects to national angel networks and family offices; intro pathway to local VCs

- LinkedIn: VANTEC Angel Network LinkedIn

- Sector Focus: BC fintech, digital services, B2B software, healthtech

- Stage Focus: Pre-seed, Seed

- Location: Vancouver, BC

- Website: vantec.ca

13. WUTIF Capital (VCC)

BC's angel co-investment vehicle. WUTIF is a Venture Capital Corporation that co-invests alongside angel investors in BC tech, with a 30% BC Venture Capital Tax Credit for eligible investors. For fintech founders at pre-revenue or early revenue stage, WUTIF bridges you to institutional capital.

- Recent Deals: Ongoing active deployment into BC tech startups; co-invests alongside VANTEC and individual angel syndicates; 30% BC VCC Tax Credit for BC-resident investors; active fintech, digital health, and software co-investments

- LinkedIn: WUTIF Capital LinkedIn

- Sector Focus: BC-based fintech, digital services, SaaS, tech

- Stage Focus: Pre-seed, Seed

- Location: Vancouver, BC

- Website: wutif.com

14. GTMfund

Vancouver-headquartered B2B SaaS fund that closed $54M USD Fund II in February 2025. Their LP network includes VP and C-level GTM leaders from Salesforce, DocuSign, Snowflake, LinkedIn, and Okta. For fintech founders with a clear enterprise GTM strategy, GTMfund's LP network is one of the fastest paths to your first enterprise customer alongside capital.

- Recent Deals: Fund II $78.83M CAD ($54M USD) closed February 2025, oversubscribed; plans to back ~40 startups at $500K-$1.5M each; doubling Canada deployment vs Fund I; Inovia Capital as LP in Fund II; targeted pre-seed, seed, and occasional Series A

- LinkedIn: GTMfund LinkedIn

- Sector Focus: B2B SaaS, fintech software, go-to-market revenue tools

- Stage Focus: Pre-seed, Seed, Series A

- Location: Vancouver, BC / Scottsdale, AZ

- Website: gtmfund.com

15. Garage Capital

Kitchener-based but highly active in Vancouver fintech deals. Garage Capital has backed 200+ portfolio companies valued at $30B+ collectively, with 10 unicorns including Substack. They co-invested with Pender Ventures on Veritree's $6.5M Series A in 2025. For Vancouver fintech companies at pre-seed or seed, Garage's LP network and portfolio connections accelerate US expansion.

- Recent Deals: Veritree $6.5M Series A co-invest with Pender Ventures (May 2025); 200+ portfolio companies; 10 unicorns including Substack; Substack became a unicorn in 2025; active pre-seed and seed deployment; 118 tech company investments

- LinkedIn: Garage Capital LinkedIn

- Sector Focus: B2B SaaS, fintech, marketplaces, AI software

- Stage Focus: Pre-seed, Seed

- Location: Kitchener, ON (active Vancouver deal flow)

- Website: garage.vc

How to approach Vancouver fintech VCs

Cold email conversion with Luge Capital, Rhino, and Pender is under 3%. The fastest entry point is the Fintech Cadence conference, the BC Tech Association's events, or a warm intro from another Luge or Version One portfolio founder.

Don't pitch the regulatory work you plan to do. Pitch what you've already done. If you have a banking partner letter or a money services business registration, lead with that. Most fintech investors in Vancouver have seen enough "regulatory pathway TBD" decks to stop taking meetings with founders who haven't started that work.

Upload your materials to Ellty and send a trackable link before any intro lands. You'll see which investors open your deck and how much time they spend on your unit economics slide. Read why a virtual data room beats physical files for context on how to structure your materials for fintech diligence.

What fintech investors look for in Vancouver in 2026

The first question from every fund on this list is the same: what's your take rate and gross margin? Pure API wrappers on Stripe or Plaid don't qualify as fintech moats in 2026. They want proprietary data, a banking relationship that creates switching costs, or a regulatory licence that competitors can't replicate in six months.

Unit economics have gotten harder to fake. Vancouver fintech investors have seen enough companies with high GMV and negative net revenue to demand a clear margin structure from the first meeting. If your CAC is above your first-year LTV, explain exactly why the next cohort is different - with data.

Fintech M&A is pacing toward a record year in 2026. Well-capitalized fintechs are entering a roll-up cycle. If your company is acquisition-ready within 3-5 years, say that explicitly - most investors on this list are actively tracking which strategic acquirers are building their M&A pipeline. Set up an Ellty data room with your financial model, cap table, and customer contracts before any partner review. Send a unique trackable link per investor so you see who reviews your revenue data. Check common fundraising data room mistakes to avoid the issues that slow down fintech rounds.

How to pitch with a regulatory-ready data room

Fintech investors ask for your compliance documentation in the first follow-up. If your MSB registration, FINTRAC filings, or banking partner agreements aren't organized and ready to share, you're adding weeks to a close that could be days.

The first thing they'll look for is your licensing status. In Canada, this means your FINTRAC registration for money services businesses, your provincial securities registration if relevant, and any OSFI-related documentation. Have these in a secure folder, not in a Google Drive anyone can access.

The second thing is your banking partner agreement or letter of intent. If you're processing payments, they want to know who's holding the float and what the agreement says about termination. Luge's partners have seen enough fintech companies lose their banking relationship mid-raise to ask this on the first call. Use Ellty to build a seed round data room with your compliance documents, banking agreements, and financial model. Share a trackable link with each investor and get notified when they review the regulatory section specifically.

How to pitch a Vancouver fintech investor

Five steps for founders raising from fintech investors in Vancouver in 2026.

- 1.Lead with take rate and gross margin, not GMVOpen every pitch with your unit economics, not payment volume. Vancouver fintech investors filter on margin first - GMV slides come after they believe your numbers.

- 2.Show your regulatory status before they askLead with your MSB registration, banking partner agreement, or fintech licence. Investors will ask - having the answer ready signals execution speed.

- 3.Explain your banking moat specificallyEvery investor will ask why your banking partner won't terminate the agreement. Have a specific answer about switching costs, contract terms, or data exclusivity.

- 4.Build your compliance data room before any introUpload your FINTRAC filings, banking agreements, and financial model to Ellty. Fintech investors request compliance docs within 24 hours of any promising first call.

- 5.Send each investor a unique trackable linkUse Ellty's per-investor links to see who reviews your compliance documents. If a Luge partner reads your banking agreement section twice, follow up specifically on that.

How Ellty helps you land a Vancouver fintech investor

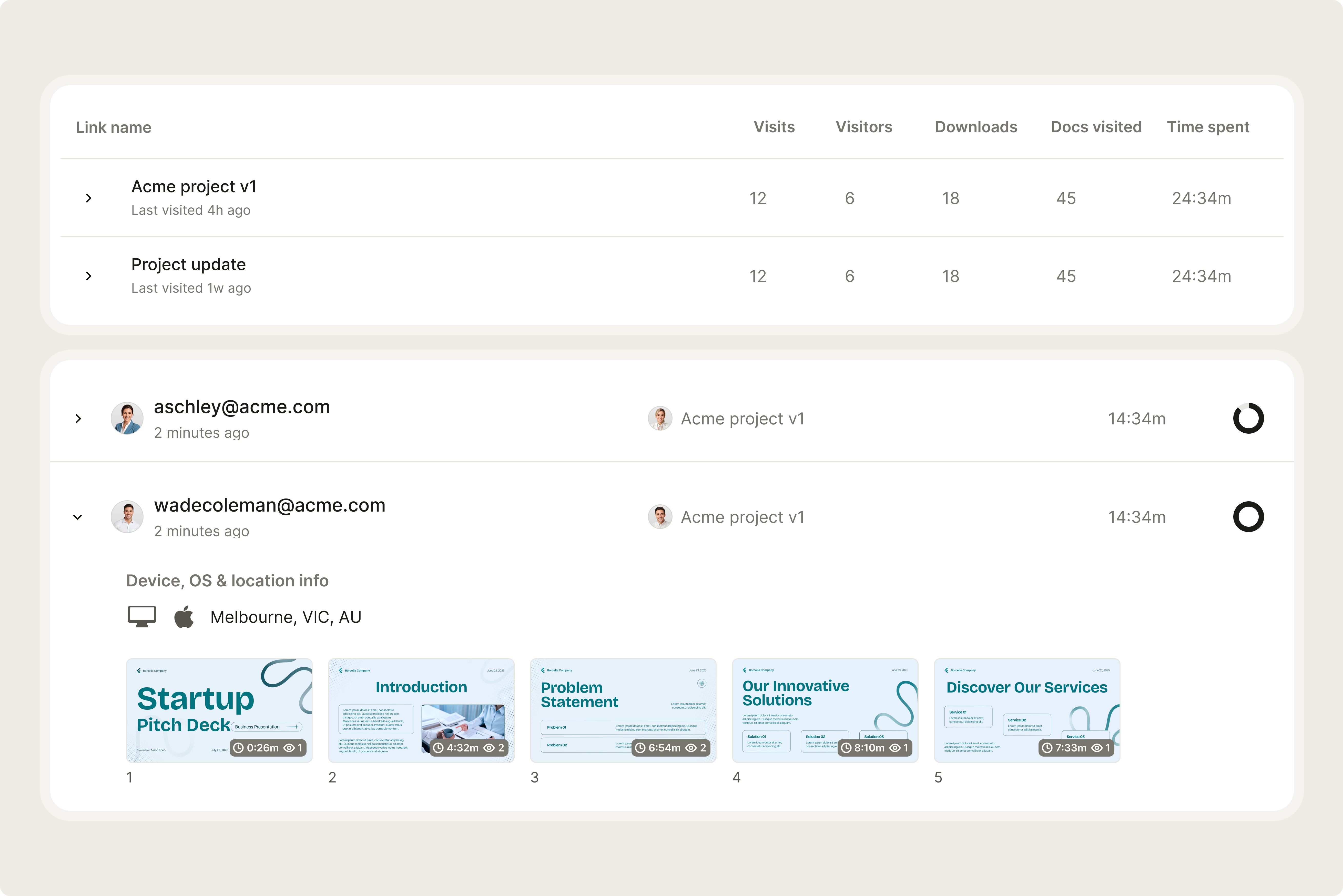

You've found the right 15 investors. Now get your materials in front of them fast. Upload your fintech pitch documents to Ellty and send a unique trackable link to each investor you contact.

- 1.Build your fintech data room with all compliance filesCreate an Ellty data room and upload your pitch deck, compliance docs, and financial model. Vancouver fintech investors request regulatory documentation within hours of any promising first call.

- 2.Set permissions to protect sensitive financial dataRequire email verification before any investor accesses your cap table or banking agreements. Use screenshot protection for proprietary financial model assumptions.

- 3.Get real-time alerts when investors review your materialsKnow which investors open your data room and how long they spend on each file. If a Luge partner spends time on your banking agreement, follow up on that section directly.

Common questions about Vancouver fintech investors

- InBC, WUTIF, and VANTEC require BC presence. Luge, BDC, and Version One fund Canadian fintech companies regardless of location. Having a Vancouver office helps with InBC and tax credits.

- Usually 10-16 weeks from first meeting to wire. Regulatory complexity can add time. Set up an Ellty data room before your first intro so compliance diligence doesn't slow your close.

- Take rate, gross margin, and your banking partner agreement. Most Vancouver fintech VCs filter on unit economics before any market size discussion. Have clean numbers ready from day one.

- Yes, but Luge and BDC prioritize Canadian companies. Version One and Garage Capital fund globally. If you're US-based, explain your Canadian market entry plan or regulatory advantage clearly.

- Before your first investor conversation. Upload your compliance documents and financial model to Ellty and send trackable links - you'll know which investors are engaged before any follow-up.

- Directly, yes. Founders with MSB registration, banking partner LOIs, or licence applications in progress close rounds faster. Luge partners will ask about your regulatory status on the first call.