Waterloo has Sun Life, Manulife, and Economical within a 30-minute drive. These 14 investors back insurtech companies that can actually access those distribution channels.

Waterloo has a structural advantage in insurtech that most founders don't use. Sun Life, Manulife, and Economical Insurance are all headquartered here or nearby. That means distribution partners, pilots, and enterprise insurance buyers within a 30-minute drive. Investors know this and factor it into their thesis.

The challenge: insurtech funding globally dropped to decade-low deal counts in Q1 2026. Active investor counts fell to their lowest level since late 2020. That's not a reason to panic - it means money is concentrating in fewer deals. If you're building something with real underwriting logic or genuine claims automation, capital is still available.

University of Waterloo alumni are Canada's second-largest group of insurtech founders after University of Toronto. Investors here don't need you to explain the talent pipeline. They need you to show that you've built something that changes how insurance is bought, priced, or administered. Before you reach out, set up your seed round data room with policy data, loss ratios if applicable, and any distribution agreements.

| Stage | Check size | Sector focus | Website | |

|---|---|---|---|---|

| Intact Ventures | Seed to Series B | $1M-$10M | Insurtech, fintech, mobility | intactventures.com |

| Portage Ventures | Seed to Series C | $1M-$15M | Insurtech, fintech, wealthtech | portageinvest.com |

| Anthemis Group | Seed to Series B | $1M-$10M | Insurtech, embedded finance | anthemis.com |

| MS&AD Ventures | Series A, Series B | $3M-$15M | Insurtech, enterprise | msad-ventures.com |

| Garage Capital | Pre-seed, seed | $200K-$750K | SaaS, AI, insurtech adjacent | garage.vc |

| Panache Ventures | Pre-seed, seed | $250K-$1.5M | B2B SaaS, insurtech adjacent | panache.vc |

| BDC Capital | Seed to growth | $500K-$20M | Cross-sector, insurtech | bdc.ca |

| MaRS IAF | Seed | Up to $500K | Insurtech, health, fintech | marsdd.com |

| OMERS Ventures | Series A to growth | $5M-$25M | Insurtech, fintech, enterprise | omersventures.com |

| Inovia Capital | Seed to growth | $3M-$15M | SaaS, AI, insurtech adjacent | inovia.vc |

| Golden Ventures | Pre-seed, seed | $500K-$3M | SaaS, fintech, insurtech | golden.ventures |

| Northside Ventures | Pre-seed | $100K-$500K | B2B SaaS, fintech, insurtech | northside.ventures |

| Sandpiper Ventures | Seed | $250K-$2M | Insurtech, SaaS, cleantech | sandpiperventures.com |

| Relay Ventures | Series A | $1M-$5M | Enterprise SaaS, insurtech | relayventures.com |

Send your insurtech deck the right way

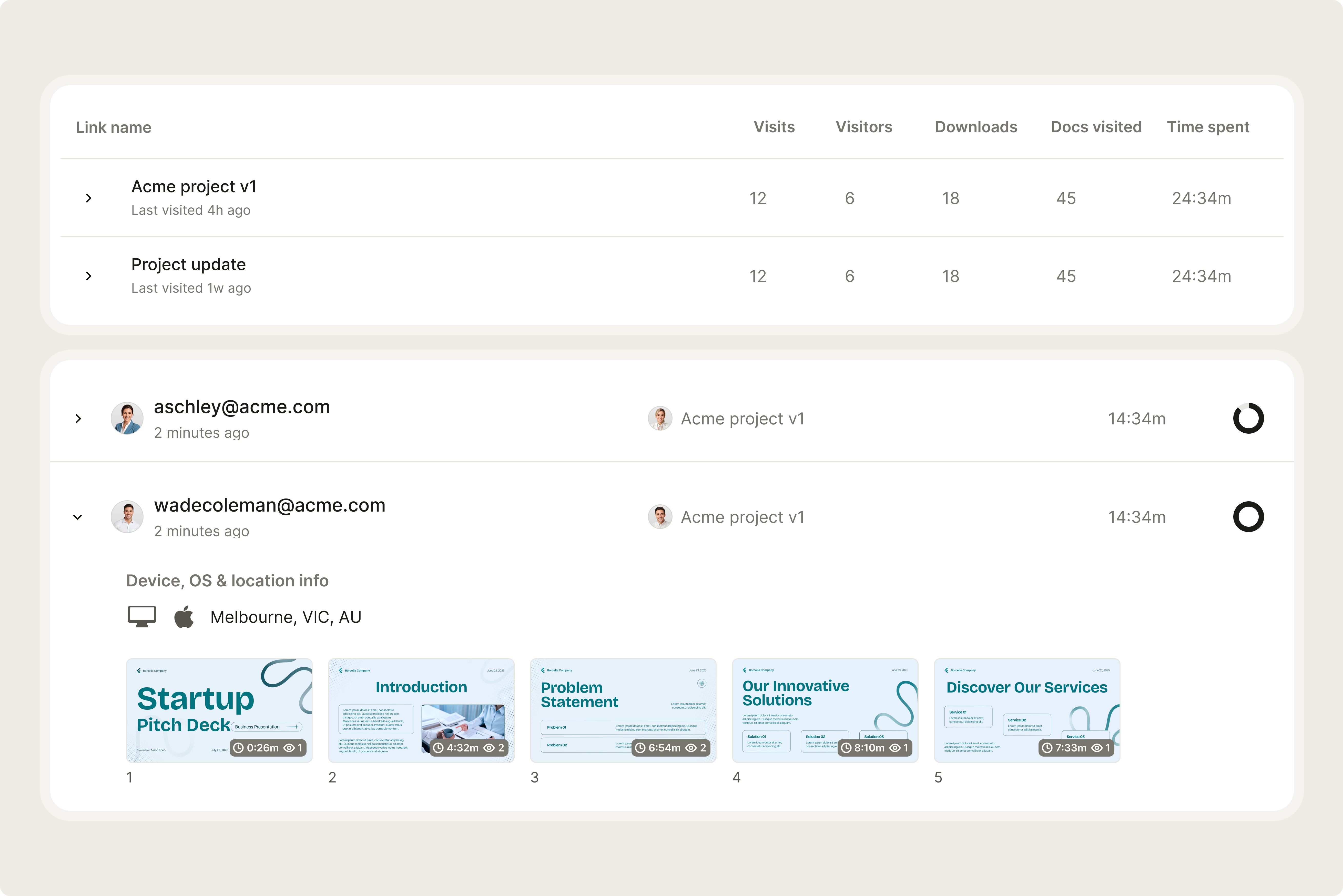

Upload to Ellty. Create trackable links. See which investors open your loss ratio slides versus just skimming the intro.

Start free 14-day trialWhat is a Waterloo insurtech investor?

A Waterloo insurtech investor backs companies building technology for insurance distribution, underwriting, or claims from the Kitchener-Waterloo corridor. They differ from generalist VCs because they understand insurance regulatory timelines, carrier procurement cycles, and what it actually takes to get a distribution deal signed with a major Canadian insurer - not just a letter of intent.

Waterloo's insurtech ecosystem is built around proximity to enterprise buyers. Sun Life and Manulife both have major Waterloo operations. That creates a level of enterprise access that no US tech city can replicate for Canadian insurtech founders. Investors like Intact Ventures and Portage Ventures specifically track this corridor because their LP base includes major insurers.

Typical check sizes range from $200K at pre-seed through $15M at Series A. Corporate CVCs like Intact Ventures add more than capital: they bring distribution relationships with Canada's largest P&C insurer. Read what documents go in a data room before any investor meeting - insurtech due diligence includes regulatory filings and underwriting data that most SaaS founders don't have organized.

The insurance industry is beginning to understand the full potential of agentic AI. The bigger opportunity is connecting broker and policyholder interactions directly to governed, compliant operational execution across the insurer's core workflows.

14 top insurtech investors for Waterloo founders in 2026

1. Intact Ventures

The venture arm of Canada's largest P&C insurer. Their check comes with a direct commercial relationship. If they fund you, you're one conversation away from a distribution pilot with a company writing billions in premiums annually.

- Recent Deals: Quandri $12M Series A co-investor (Jul 2025), Comeryx seed (automated COI platform, 2025-2026), Shepherd $42M Series B through Intact Private Capital (Mar 2026)

- LinkedIn: Intact Ventures

- Sector Focus: Insurtech, fintech, mobility, AI in insurance

- Stage Focus: Seed, Series A, Series B

- Location: Toronto, ON, Canada

- Website: intactventures.com

2. Portage Ventures

Canada's largest dedicated fintech-insurtech fund with $5.7B+ AUM. Backed Angle Health's $134M Series B in December 2025 and closed a $280M continuation vehicle with Goldman Sachs in January 2026. Their LP base includes major Canadian insurers.

- Recent Deals: Angle Health $134M Series B lead (Dec 2025), $280M Goldman Sachs continuation vehicle (Jan 2026), Cata seed (Apr 2026)

- LinkedIn: Portage Ventures

- Sector Focus: Insurtech, payments, wealthtech, lending infrastructure

- Stage Focus: Seed, Series A, Series B, Series C

- Location: Toronto, ON (also Montreal)

- Website: portageinvest.com

3. Anthemis Group

Global insurtech and fintech specialist. One of the most active pure-play insurtech funds globally with 46 seed rounds in the sector. Backs companies transforming insurance from the inside - underwriting platforms, digital distribution, and embedded insurance.

- Recent Deals: 46 seed-stage insurtech investments globally; active 2025-2026 insurtech and embedded finance portfolio

- LinkedIn: Anthemis Group

- Sector Focus: Insurtech, fintech, embedded finance

- Stage Focus: Seed, Series A, Series B

- Location: London, UK (active in North America including Canada)

- Website: anthemis.com

4. MS&AD Ventures

Corporate VC arm of one of Japan's largest insurers and the most active Series A insurtech investor globally with 35+ rounds. They back companies that can eventually distribute through their global insurance network. Worth the longer conversation timeline.

- Recent Deals: Active 2025-2026 Series A insurtech deployment; 35+ global Series A insurtech investments

- LinkedIn: MS&AD Ventures

- Sector Focus: Insurtech, enterprise, next-generation insurance

- Stage Focus: Series A, Series B

- Location: San Francisco, CA (global portfolio including Canada)

- Website: msad-ventures.com

5. Garage Capital

Waterloo's only native VC. They don't have a dedicated insurtech thesis, but if your insurtech company is fundamentally a B2B SaaS business, this is your local seed fund. They backed Cognito Health and other insurance-adjacent companies.

- Recent Deals: Sygaldry seed (Apr 2026), Upside Robotics $7.5M seed co-lead (Feb 2026), Cognito Health $2M seed (insurtech-adjacent, 2024)

- LinkedIn: Garage Capital

- Sector Focus: B2B SaaS, AI, insurtech adjacent

- Stage Focus: Pre-seed, seed

- Location: Kitchener-Waterloo, ON, Canada

- Website: garage.vc

6. Panache Ventures

Canada's most active pre-seed fund. They back AI and SaaS-driven companies including insurtech workflow tools. If you're building insurance workflow software, underwriting AI, or broker automation, they'll take the meeting.

- Recent Deals: Nord Quantique seed (May 2026), InstaSwitch seed (May 2026), active 2025-2026 deployment from $100M Fund II

- LinkedIn: Panache Ventures

- Sector Focus: B2B SaaS, AI, fintech, insurtech adjacent

- Stage Focus: Pre-seed, seed

- Location: Montreal, QC (active across Waterloo corridor)

- Website: panache.vc

Organize your insurtech data room

Set up an Ellty data room with underwriting data, loss ratios, and distribution agreements. Insurtech diligence is document-heavy.

Start free 14-day trial7. BDC Capital

Canada's largest VC by portfolio count. Government-backed but faster than you'd expect. They've backed insurtech companies through multiple stages and have real follow-on reserves.

- Recent Deals: Active across SaaS, health, and insurtech adjacent companies 2025-2026; 700+ portfolio companies total

- LinkedIn: BDC Capital

- Sector Focus: Cross-sector, insurtech, SaaS, health tech, AI

- Stage Focus: Seed through growth

- Location: Ottawa, ON (offices across Canada)

- Website: bdc.ca

8. MaRS Investment Accelerator Fund (IAF)

Ontario government-backed fund writing up to $500K into Waterloo-region insurtech companies. Co-invests with Intact Ventures and Portage on Ontario deals. Small checks but they connect you to major Canadian insurer networks.

- Recent Deals: Active Ontario fintech and insurtech deployment 2025-2026, multiple health insurance and insurtech adjacent companies

- LinkedIn: MaRS IAF

- Sector Focus: Insurtech, fintech, health tech

- Stage Focus: Seed, pre-Series A

- Location: Toronto, ON (with Waterloo connections)

- Website: marsdd.com

9. OMERS Ventures

The VC arm of one of Canada's largest pension funds. Fund IV ($750M) is actively deploying. They've backed insurtech and fintech infrastructure companies and have real growth-stage capacity that most Canadian funds lack.

- Recent Deals: Active deployment 2025-2026 in fintech and enterprise software; $750M Fund IV deploying now

- LinkedIn: OMERS Ventures

- Sector Focus: Insurtech, enterprise SaaS, AI infra, fintech

- Stage Focus: Series A, Series B, growth

- Location: Toronto, ON, Canada

- Website: omersventures.com

10. Inovia Capital

Multi-stage fund with a strong SaaS and AI thesis that extends into insurtech. They co-led Cohere's $500M Series D and are deploying from a new fund in 2026. Good fit for insurtech companies with strong recurring revenue and enterprise customers.

- Recent Deals: Toyo seed $4.3M (Feb 2026), Sentra seed $5M (Jan 2026), Cohere $500M Series D co-lead (Aug 2025)

- LinkedIn: Inovia Capital

- Sector Focus: SaaS, AI, insurtech adjacent, enterprise platforms

- Stage Focus: Seed, Series A, Series B, growth

- Location: Montreal, QC (with Toronto office)

- Website: inovia.vc

11. Golden Ventures

Toronto-based seed fund with SaaS and fintech as core theses. Will look at insurtech SaaS with clear unit economics. Not an insurtech specialist but they write consistently at seed and follow on.

- Recent Deals: Active seed deployment from Fund V ($100M), multiple 2025-2026 SaaS and fintech investments

- LinkedIn: Golden Ventures

- Sector Focus: B2B SaaS, fintech, insurtech adjacent

- Stage Focus: Pre-seed, seed

- Location: Toronto, ON, Canada

- Website: golden.ventures

12. Northside Ventures

Pre-seed fund explicitly backing Canadian insurtech alongside B2B SaaS and fintech. Alex McIsaac was an early investor in QuickFacts (Canadian insurtech) and actively tracks the sector. Writes $100K-$500K at inception.

- Recent Deals: QuickFacts early investment (Canadian insurtech, 2024-2025), Datacurve, Switch (portfolio); 25 investments total

- LinkedIn: Northside Ventures

- Sector Focus: B2B SaaS, AI, fintech, insurtech

- Stage Focus: Pre-seed

- Location: Toronto, ON (Waterloo corridor active)

- Website: northside.ventures

13. Sandpiper Ventures

Atlantic Canada-based fund that co-led QuickFacts' $2M CAD seed in 2025 alongside InsurTech NY and Killick Capital. One of the few Canadian funds actively writing first checks into insurtech SaaS at seed.

- Recent Deals: QuickFacts $2M CAD seed co-lead (2025, Canadian insurtech); active 2025-2026 Canadian seed deployment

- LinkedIn: Sandpiper Ventures

- Sector Focus: Insurtech, SaaS, cleantech

- Stage Focus: Seed

- Location: Halifax, NS, Canada

- Website: sandpiperventures.com

14. Relay Ventures

Toronto-based with a solid enterprise SaaS track record. Writes $1M-$5M Series A checks. Not an insurtech specialist, but they'll look at insurtech SaaS companies with strong enterprise retention and a clear US expansion path.

- Recent Deals: Active Series A deployment across Canadian enterprise SaaS in 2025-2026

- LinkedIn: Relay Ventures

- Sector Focus: Enterprise SaaS, insurtech adjacent, mobile-first enterprise

- Stage Focus: Series A

- Location: Toronto, ON (Waterloo corridor active)

- Website: relayventures.com

How to approach insurtech investors in Waterloo

Corporate VCs like Intact Ventures evaluate companies differently than financial VCs. They want to know if your product can run inside their distribution network or improve their underwriting. Lead with the operational case, not the TAM slide. Portage and Anthemis are tired of market size narratives - show your loss ratio, CAC, and policy renewal rates early.

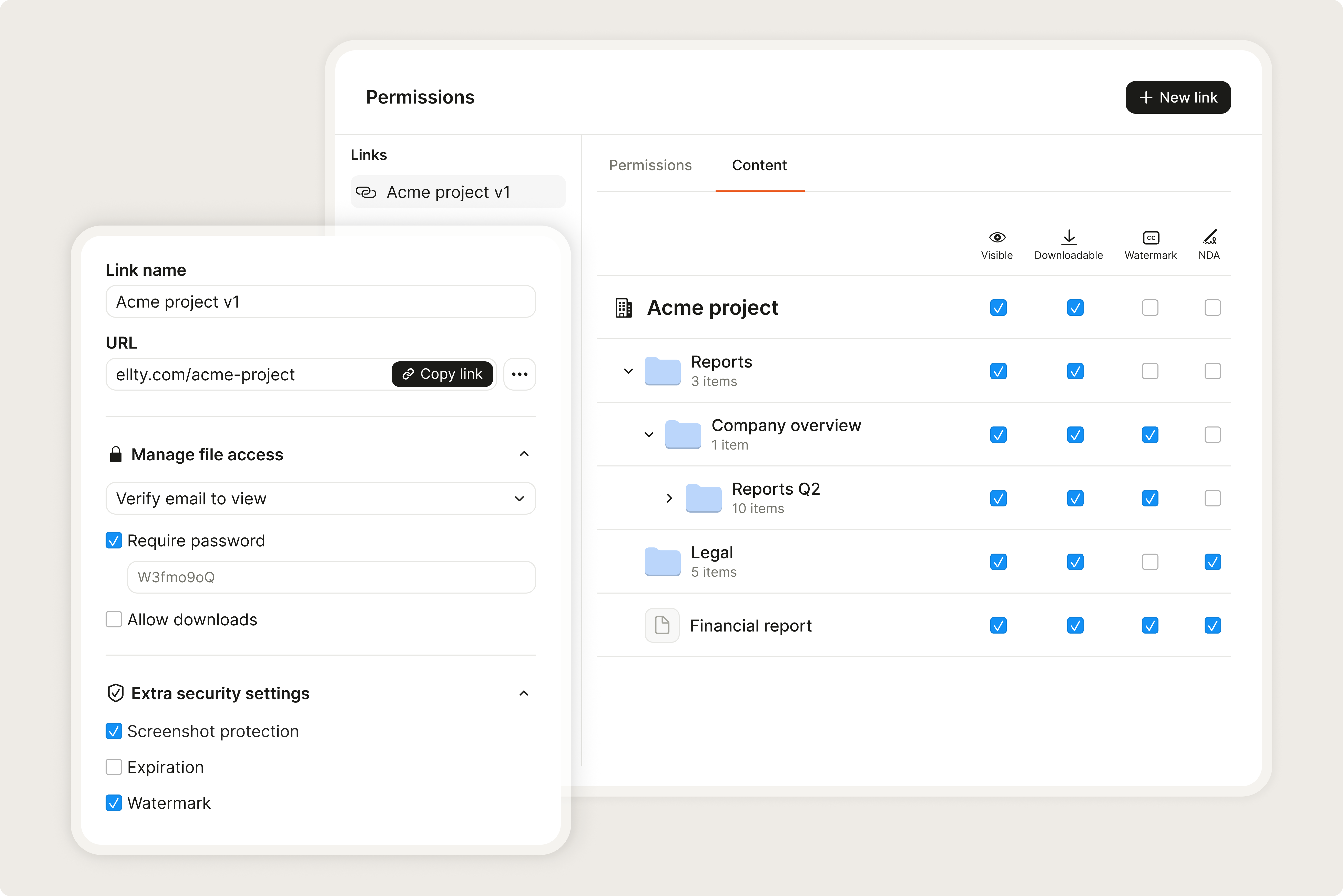

Before any second meeting with an insurtech fund, upload your underwriting data, regulatory approvals, and key distribution agreements to an Ellty data room. Insurtech diligence is document-heavy. Having everything in one place with view analytics means you'll know which investors are actually serious versus just collecting information. Read how investors review a data room - insurtech investors add underwriting data and compliance docs to that standard list.

What insurtech investors check during diligence

Technical due diligence in insurtech is different from standard SaaS. Investors will look at your claims data, actuarial assumptions, or API integration specs depending on what you're building.

At Series A, Portage and MS&AD want regulatory filings or MGA authorization before committing. If you're building a full-stack insurer, expect reinsurance treaty review as part of diligence. If you're building distribution software, customer data agreements and pilot terms matter more than your product demo.

Dead portfolio companies are a red flag in insurtech. If an investor backed three embedded insurance startups that all failed to reach distribution scale, ask why. Most will be honest if you ask directly. Use secure data room sharing to control who sees your underwriting data during any investor process.

Where to find Waterloo insurtech investors before outreach

Communitech's member directory lists most active Ontario investors. The InsurTech Spring Conference brings investors and founders together annually - more useful than generic startup networking events. MaRS Discovery District runs Ontario-specific insurtech programs that connect founders directly to Intact Ventures and Portage.

LinkedIn works for insurtech cold outreach if you reference a specific portfolio company. Intact Ventures portfolio founders are generally willing to describe what working with the fund is actually like. Ask about diligence timelines and whether the LP distribution network was actually activated - not just promised.

Don't pitch Portage or Intact Ventures without a paying financial institution or carrier customer. They're staffed by former banking and insurance executives who recognize immediately whether you've been in real sales conversations with their LP base. "We're talking to Sun Life" is not the same as "Sun Life is paying us." Set up your virtual data room for due diligence before you get to that conversation.

How to pitch a Waterloo insurtech investor

Insurtech diligence is document-heavy. Have your regulatory status and underwriting data organized before investors ask.

- 1.Clarify your insurtech model upfrontState whether you're MGA, B2B SaaS, or full-stack. Investors evaluate them completely differently from each other.

- 2.Lead with distribution, not just technologyName your current carrier or broker partners. Distribution is what insurer CVCs fund, not demos alone.

- 3.Prepare a compliant data room before sharingInclude regulatory approvals, loss ratios if applicable, and reinsurance details in Ellty before any investor views it.

- 4.Research which CVCs match your specific modelIntact Ventures looks at P&C. Portage covers wealthtech and insurtech both. Know the difference before you reach out.

- 5.Get intros through MaRS or Communitech programsBoth facilitate connections to Intact Ventures and Portage specifically. Use their programs before going cold.

How Ellty helps you land a Waterloo insurtech investor

Insurtech investors ask for more documents than most sectors. Get your materials organized in one secure place before any conversation progresses.

- 1.Upload your insurtech data room filesAdd your deck, regulatory status, and underwriting data. Organized folders signal you're ready for diligence.

- 2.Set permissions before sharing sensitive dataRequire email verification. Restrict downloads on compliance documents. Track exactly who views what.

- 3.Know when Intact or Portage partners engageGet notified the moment an investor opens your loss ratio or distribution agreement slides. Follow up with context.

Common questions about Waterloo insurtech fundraising

- Not always. But you need a carrier partner or advisor who does. VCs won't fund pure tech plays without insurance domain credibility on the team.

- Distribution fit with their P&C network. Show them how your product specifically improves outcomes for property and casualty carriers.

- Financial VCs like Portage move faster. Corporate VCs like Intact add more value if distribution is your bottleneck. Start based on what you actually need.

- Longer than SaaS. Expect 10-16 weeks for Series A from first meeting to term sheet. Regulatory review and carrier reference checks add time.

- Before your first meeting. Insurtech VCs ask for compliance docs and loss data fast. Ellty gets you organized in under an hour.

- Yes. Fewer competitors, carrier relationships are accessible, and Waterloo alumni networks provide hiring leverage. Prove it here first.