Michigan CRE deals carry risks that catch buyers off guard: brownfield liability under Part 201, PA 116 agricultural tax status that collapses on sale, and a transfer tax that applies at both state and county level. This checklist covers every check before you close in 2026.

Michigan is a sprawling industrial and agricultural state. Detroit, Grand Rapids, Lansing, and Ann Arbor anchor distinct commercial submarkets. Each has its own zoning rules, brownfield authority, and deal patterns.

Part 201 of the Natural Resources and Environmental Protection Act is Michigan's environmental liability law. It covers contaminated sites and can bind new owners to cleanup obligations. Former auto plants, foundries, and industrial waterfront parcels carry the highest exposure.

Michigan's PA 116 program freezes property taxes on agricultural land. When a parcel under PA 116 converts to commercial use on sale, the prior years' deferred taxes come due. Out-of-state buyers rarely model this correctly.

Load all property files into your Ellty virtual data room before diligence opens. Each advisor gets a scoped link on day one - no email chains, no version confusion when files update.

Where Michigan property deals actually go wrong

Not every check carries the same weight. The table below sorts risks by impact on deal execution.

| Area | Documents to pull | Michigan red flag | Matters most for | Tier | |

|---|---|---|---|---|---|

| Title and ownership | Title and ownership | Deed, title commitment, 40-year chain-of-title, Register of Deeds search, tax certificate | Michigan tax-reverted parcels are common in Detroit; confirm no open land bank or county forfeiture | All buyers | Dealbreaker |

| Brownfield and Part 201 liability | Brownfield and Part 201 liability | Phase I ESA, EGLE database search, Baseline Environmental Assessment, brownfield plan | Michigan Part 201 binds new owners to cleanup; a BEA filed before closing limits but doesn't eliminate liability | Industrial, former auto, urban infill parcels | Dealbreaker |

| Zoning and land use | Zoning and land use | Zoning certificate, variance history, special use permit, Michigan EGLE wetland permit records | Michigan wetland regulations trigger on parcels near Great Lakes shoreline, rivers, and inland lakes | Development, repositioning, waterfront | Dealbreaker |

| PA 116 agricultural tax status | PA 116 agricultural tax status | PA 116 enrollment certificate, township treasurer records, deferred tax calculation | PA 116 conversion on sale triggers recapture of deferred taxes going back up to 7 years; kills deal economics | Agricultural, semi-rural, suburban edge parcels | Dealbreaker |

| Leases and tenancies | Leases and tenancies | All leases, amendments, rent roll, estoppels, Michigan commercial lease terms | Michigan has no commercial tenant protection statute; verbal lease arrangements in smaller markets are common | Income-producing assets | Price-adjuster |

| Building and physical condition | Building and physical condition | Property Condition Assessment, building permit history, certificate of occupancy, roof and envelope report | Michigan freeze-thaw cycles cause accelerated foundation and envelope failure; older industrial stock most at risk | All asset types | Price-adjuster |

| Service charge and operating costs | Service charge and operating costs | 3y operating statements, Michigan property tax assessments, CAM reconciliations, special assessments | Michigan Proposal A caps annual assessment increases at 5% or CPI; a sale resets taxable value to SEV | Income-producing assets | Price-adjuster |

| Transfer tax | Transfer tax | Michigan real estate transfer tax receipts, county transfer tax stamps, Form 2796 | Michigan state RETT is $7.50 per $1,000 paid by seller; each county adds $1.10 per $500 of consideration | All deals | Price-adjuster |

| Insurance and valuation | Insurance and valuation | Current policies, loss run history, FEMA flood zone certificate, Great Lakes shoreline coverage | Great Lakes and inland lake parcels face high shoreline erosion risk; standard property policies don't cover it | Waterfront, lake-adjacent parcels | Standard check |

| Utilities and access | Utilities and access | Utility connection records, MDOT access permits, private road easements, mineral rights search | Michigan has active mineral rights activity in the UP; severed mineral rights complicate title | Rural, UP, agricultural-edge parcels | Standard check |

| Seller KYC and AML | Seller KYC and AML | Entity docs, deed match, Michigan LARA search, bankruptcy search, judgment lien search | Michigan LLC must be in good standing with LARA before a deed is accepted for recording | All deals | Standard check |

Running due diligence on a Michigan property?

Set up your data room before diligence starts.

Start free 14-day trialThe full Michigan property due diligence checklist

Title and ownership

- Pull the deed and confirm the legal description matches the current ALTA survey exactly

- Order a 40-year chain-of-title from the county Register of Deeds

- Run a tax certificate search; confirm no outstanding delinquent taxes or forfeiture proceedings

- For Detroit and Wayne County parcels: check the land bank database for prior tax reversion

- Verify the parcel ID matches all closing, survey, and tax documents before proceeding

- Confirm no open mechanic's lien claims against recent construction at the parcel

Brownfield and Part 201 liability

- Commission a Phase I ESA per ASTM E1527-21; former auto, foundry, and industrial parcels need extra scrutiny

- Search the EGLE online database for Part 201 facilities, UST records, and open remediation sites

- Confirm whether a Baseline Environmental Assessment has been filed on the parcel before closing

- Check the local brownfield redevelopment authority for any existing brownfield plan on the site

- Budget Phase II ESA at $10,000-$35,000 if recognized environmental conditions appear in Phase I

- Confirm whether Michigan liability protection under Part 201 applies and what conditions must be met

Load EGLE search results and Phase I findings into Ellty before advisors arrive. Each consultant gets a scoped link - track who reviewed every environmental file.

Zoning and land use

- Confirm current zoning from the township or city planning department in writing

- Pull the full variance and special use permit history from the local zoning board of appeals

- Check EGLE wetland permit records; Michigan regulates both inland and coastal wetlands strictly

- Verify all certificates of occupancy for buildings and improvements are current and recorded

- Confirm no open code violations or stop-work orders at the local building department

- For Great Lakes shoreline parcels: check EGLE Critical Dune or shoreline protection designations

PA 116 agricultural tax status

- Confirm whether the parcel is enrolled in the PA 116 Farmland Preservation Program

- Request the deferred tax calculation from the township treasurer before committing to terms

- Understand that conversion on sale triggers recapture of deferred taxes going back up to 7 years

- Confirm whether seller or buyer bears the PA 116 recapture obligation under the purchase agreement

- Check whether the parcel is separately enrolled in a Michigan Natural Resources Trust Fund easement

- For large suburban edge parcels: assume PA 116 enrollment until the township confirms otherwise

Leases and tenancies

- Collect all leases, amendments, and sublease consents before diligence opens

- Cross-reference the rent roll against 3 months of actual bank receipts from the seller

- Confirm estoppel certificates are deliverable before the scheduled closing date

- Identify any month-to-month occupancies or undocumented tenants at the property

- Check for tenant purchase options or rights of first refusal embedded in lease terms

- Flag any verbal lease arrangements common in smaller Michigan markets

Building and physical condition

- Commission a Property Condition Assessment; flag foundation and envelope for freeze-thaw review

- Pull the full building permit history from the local building or inspectional services department

- Verify Michigan mechanical code compliance on HVAC and rooftop equipment

- Confirm ADA compliance documentation for all commercial spaces on the property

- Check roofs and envelopes carefully; Michigan winters cause accelerated deterioration on older stock

- For industrial assets: inspect loading dock structures and slab condition before accepting seller's figures

Service charge and operating costs

- Pull 3 years of operating statements and reconcile against county assessment records

- Check for pending special assessments for road, water, or sewer improvements on the parcel

- Confirm taxable value vs. state equalized value; a sale resets taxable value to SEV under Proposal A

- Audit CAM pass-throughs against lease terms for all multi-tenant assets

Transfer tax

- Calculate Michigan state real estate transfer tax at $7.50 per $1,000 of consideration, paid by seller

- Add county real estate transfer tax at $1.10 per $500 of consideration, also typically seller-paid

- File Michigan Form 2796 (Real Estate Transfer Tax Valuation Affidavit) at closing

- Confirm whether any RETT exemptions apply; certain government or nonprofit transfers qualify

See how Massachusetts due diligence compares if you're buying in multiple states - deed excise tax and environmental liability frameworks differ significantly.

Insurance and valuation

- Pull current insurance policies and a 3-year loss run history from the seller

- Check FEMA flood zone status on all waterfront, riverfront, and low-lying Michigan parcels

- Verify erosion and shoreline coverage on any Great Lakes or inland lake-adjacent property

- Order an independent appraisal scoped to the intended use and lender requirements

Utilities and access

- Verify all utility connections are active and legally transferable at closing

- Check MDOT records for any state highway access permit requirements on the parcel

- Search for severed mineral rights on rural and Upper Peninsula parcels before committing

- Confirm legal road access via recorded easement or dedicated public right of way

Seller KYC and AML

- Confirm seller identity matches the Register of Deeds deed record exactly

- For LLC or corporate sellers: confirm good standing with Michigan LARA before closing

- Run bankruptcy, federal tax lien, and judgment lien searches before committing to close

- Confirm entity authority to sell; Michigan LLCs require manager or member authorization

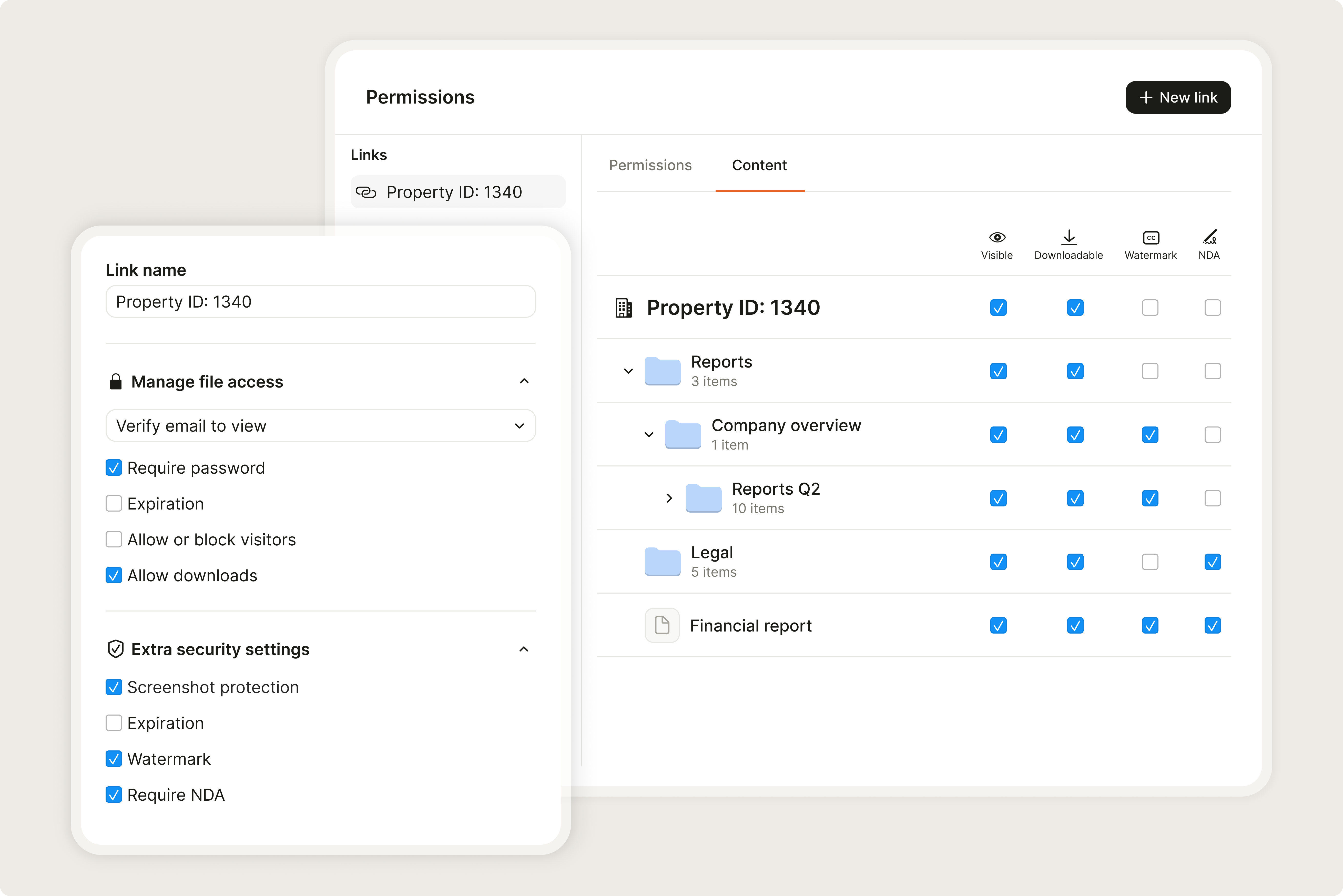

Use Ellty's granular permissions to give each advisor access to only their relevant files. Title counsel sees title docs; the ESA firm sees environmental records - no cross-contamination.

How property due diligence in Michigan works

Step 1 - Title search

Start the title search immediately after contract execution. Michigan uses a race-notice recording system; the first to record a valid instrument wins priority.

Commission a 40-year chain-of-title at the county Register of Deeds. For Detroit parcels: run a land bank database check in parallel - tax reversion is the most common title defect on Wayne County commercial parcels.

Step 2 - Survey and inspection

Order an ALTA/NSPS survey alongside the title search. Confirm the parcel number, legal description, and all easement locations match the deed - and flag any mineral rights severances on rural parcels.

Commission the Property Condition Assessment in parallel. Michigan freeze-thaw cycles make envelope, foundation, and roof review non-negotiable on any building more than 20 years old.

Step 3 - Leases and income review

Pull all leases and flag any verbal occupancy arrangements first. Michigan commercial practice in secondary markets frequently includes undocumented month-to-month tenants that don't appear on the rent roll.

See how Illinois property due diligence compares if you're running multi-state Midwest acquisitions. Transfer tax treatment and environmental frameworks differ between Michigan and Illinois.

Step 4 - Environmental review

Run the Phase I ESA and EGLE database search in parallel. Former auto assembly, stamping, and foundry sites across Detroit, Flint, Saginaw, and Muskegon carry Part 201 contamination risk.

Load EGLE search results and Phase I findings into Ellty so lenders and advisors can access them. Track who reviewed which file and when - no open folders, no missed sign-offs on environmental items.

Step 5 - Closing and registration

Michigan closing requires payment of state and county real estate transfer taxes before the deed is presented to the Register of Deeds. Confirm LARA good-standing for any LLC or corporate seller before closing day.

Out-of-state buyers regularly miss the PA 116 deferred tax recapture calculation. Confirm PA 116 status and deferred tax liability before committing to price - it's a direct cost impact on agricultural-edge parcels.

How to set up your Michigan data room in Ellty.

Load Michigan property files before advisors arrive. Give each one a scoped link on day one.

- 1.Create a data room and upload the property filesDrop title docs, leases, EGLE search results, and brownfield records into Ellty. Each folder maps to a diligence area.

- 2.Give each advisor a scoped, secure linkYour title attorney sees title files only. The ESA consultant sees environmental files only. Ellty enforces the scope.

- 3.Track who reviews which documentsSee which files each advisor opened and when. Spot delays before they slow the Michigan close.

What makes due diligence in Michigan different

Part 201 brownfield liability is the first trap for out-of-state buyers. Unlike CERCLA, Michigan's Part 201 applies a tiered cleanup standard. A buyer who files a Baseline Environmental Assessment before closing gets limited liability protection - but only if the BEA is filed correctly and before the deed transfers.

PA 116 deferred tax recapture catches buyers who don't check agricultural enrollment status. A parcel enrolled in the Farmland Preservation Program carries up to 7 years of deferred tax obligations. Those taxes come due in full when the parcel converts to commercial use on sale - a cost that can reach six figures on larger acreage deals.

Michigan's Proposal A property tax reset is the third trap. When a commercial parcel sells, taxable value resets to state equalized value. On properties where taxable value has been capped well below SEV for years, the post-sale tax increase can materially change the deal's operating economics. Buyers from other states who don't model this often overpay.

A purchaser who acquires a facility contaminated prior to their ownership may qualify for liability protection under Part 201 if a Baseline Environmental Assessment is conducted and submitted to EGLE prior to or on the date of purchase. The BEA must document existing contamination at the time of acquisition to establish the baseline.

Timeline and cost in Michigan

Week 1-2 covers kickoff: Register of Deeds title search, PA 116 status check, EGLE database search, land bank check for Detroit parcels, ALTA survey engagement, and Phase I ESA. Budget $3,000-$7,500 for this phase.

Load all files into Ellty on day one and give each advisor a trackable scoped link. That removes weeks of email follow-up from a standard Michigan diligence process.

Weeks 2-4 cover deep review: Phase I ESA delivery, Property Condition Assessment, lease abstraction, brownfield plan review, Proposal A tax reset calculation, and FEMA flood zone check.

Cost for weeks 2-4 runs $5,000-$18,000 depending on Phase I scope and asset complexity. Phase II ESA adds $10,000-$35,000 if recognized environmental conditions surface; budget early on any former industrial parcel.

Weeks 4-6 handle resolution: Phase II if needed, BEA filing coordination if required, PA 116 deferred tax negotiation, title exception resolution, and closing at the Register of Deeds.

Michigan state real estate transfer tax runs $7.50 per $1,000 paid by seller. The county adds $1.10 per $500. Buy-side legal fees typically run $2,500-$7,000 for a standard Michigan commercial close. Costs are fixed-fee from most Michigan title firms; transfer taxes are price-linked.

Michigan deal documents in one secure place

Track who reviews title, leases, EGLE files, and brownfield records in Ellty.

Start free 14-day trialCommon questions about property due diligence in Michigan

- Part 201 of Michigan's NREPA governs contaminated site cleanup. New owners can inherit cleanup liability unless a Baseline Environmental Assessment is filed before the deed transfers.

- A BEA is a Phase I-level assessment submitted to EGLE before or on the date of property purchase. It documents existing contamination and limits but does not eliminate buyer liability under Part 201.

- PA 116 is Michigan's Farmland Preservation Program. Enrolled parcels pay lower taxes, but conversion to commercial use triggers recapture of deferred taxes going back up to 7 years.

- Michigan state real estate transfer tax is $7.50 per $1,000 paid by the seller. Each county adds $1.10 per $500 of consideration, also typically seller-paid at closing.

- Proposal A caps annual property tax assessment increases at 5% or CPI. A sale resets taxable value to state equalized value, which can sharply increase operating costs post-close.

- Standard Michigan deals close in 30-60 days. Part 201 environmental findings, BEA filing, or PA 116 deferred tax negotiations regularly push timelines past 60 days on complex parcels.