Raising money is one of the hardest things you'll do as a founder. It's not just about having a good idea. It's about knowing who to talk to, when to talk to them, what they want to see, and how to move fast enough to keep momentum alive.

This guide walks you through the entire funding process - from understanding the different types of startup capital to preparing for due diligence. Whether you're about to raise your first check or getting ready for a Series A, you'll find something useful here.

What startup funding actually is

Startup funding is external capital raised to grow your business. In exchange, you typically give up equity (ownership), or in some cases take on debt that you'll repay later.

Investors give you money because they believe your company will be worth significantly more in the future. They're buying a piece of that future value today. Their return comes when you exit - through an acquisition or IPO.

That's the core deal. Everything else is mechanics.

Types of startup funding

Before you decide who to pitch, you need to understand what kind of money exists and where it comes from. Not all capital is the same.

Bootstrapping

You fund the business yourself - from savings, revenue, or both. No external investors, no equity given away.

Bootstrapping works when your business can generate cash early or when you don't need a lot of capital to get to proof points. It keeps you in full control. The tradeoff is slower growth and personal financial risk.

A lot of B2B SaaS companies bootstrap to $1-2M ARR before raising. That gives them real leverage when they do go to investors.

Friends and family

This is often the first external money a founder raises. Someone who knows you personally writes a check because they believe in you, not your metrics.

It's fast and comes with fewer strings attached. But be careful. If things go wrong, it's not just a business relationship at stake. Make it formal - use a SAFE or convertible note, document everything, and make sure they understand the risk.

Angel investors

Angels are individuals who invest their own money into early-stage startups. They're often former founders or executives who have capital to deploy and want to stay close to the startup ecosystem.

Angels typically invest $10K-$250K per deal, sometimes more in syndicates. They're usually faster to decide than institutional VCs and can add real value through introductions and advice.

Finding angels: platforms like AngelList, LinkedIn, founder communities, and warm introductions through your network.

Venture capital

VC firms raise money from limited partners (pension funds, endowments, family offices) and deploy it into startups. They take equity and expect big returns - typically 10x+ on at least some of their investments.

VCs operate on a portfolio model. They know most investments won't work out. They need the ones that do to return the entire fund.

This means they're looking for companies that can plausibly become very large. If your business doesn't have that potential, VC is probably not the right fit - and that's okay.

Accelerators and incubators

Programs like Y Combinator, Techstars, and hundreds of regional accelerators provide funding (usually $100K-$500K), mentorship, and network access in exchange for equity (typically 5-10%).

The real value beyond the check is the network, the pressure to hit milestones, and the signal that comes with getting into a competitive program.

Applications are batch-based, so timing matters.

Crowdfunding

Equity crowdfunding (Republic, Wefunder) lets you raise from a large group of smaller investors. Reward-based crowdfunding (Kickstarter, Indiegogo) raises pre-sale revenue without giving up equity.

Equity crowdfunding works well for consumer products and companies with strong communities. It's slower and more operationally complex than a clean VC round, but it can work.

Revenue-based financing

RBF providers (Pipe, Capchase, Clearco) give you capital in exchange for a percentage of future revenue until a multiple of the original amount is repaid. No equity given up.

It's a good option for companies with predictable recurring revenue that don't want to dilute. SaaS businesses often use it to fund growth without raising a full equity round.

Grants and non-dilutive funding

Government programs, innovation funds, and research grants offer capital without equity. SBIR/STTR grants in the US can be significant for deep tech and biotech. EU Horizon funding is substantial for European startups.

Non-dilutive funding takes time to apply for and win. But it's essentially free money if you're eligible.

Understanding dilution - and why it matters more than your valuation

Most founders fixate on valuation. It's the wrong thing to fixate on.

Dilution is what actually determines how much of your company you own when you exit. You can raise at a great valuation and still get crushed by dilution if you're not careful about how much equity you give away at each stage.

Here's the basic mechanic: every time you issue new shares - to investors, to employees, to advisors - the ownership percentage of existing shareholders goes down. That's dilution. The total value of the company can go up while your percentage goes down, which is often fine. But it becomes a problem when you give away too much too early and have nothing left to work with in future rounds.

A rough rule of thumb for how much equity to give up at each stage:

- Pre-seed: 5-15%

- Seed: 15-25%

- Series A: 15-25%

- Series B: 10-20%

Stack those up and you can see how quickly founder ownership erodes. By Series B, a founder who gave away too much early might be down to 20-30% before any employee options are factored in.

Model your dilution before you agree to any terms. Don't wait until you receive a term sheet to figure out what a deal means for your ownership.

The option pool shuffle

One dilution mechanism that catches first-time founders off guard is the option pool.

Investors will often require you to have a stock option pool in place for future employees - typically 10-20% of fully diluted shares. Here's the catch: investors usually want the option pool created before the round closes, which means it comes out of the pre-money valuation. That dilutes the founders, not the incoming investors.

The size of the option pool is negotiable. Build a realistic hiring plan and defend the pool size you actually need. Don't just accept whatever number the investor puts in the term sheet.

Funding stages explained

Startups go through funding stages roughly aligned with the maturity of the business. Each stage has different expectations, check sizes, and investor types.

Pre-seed

Typical raise: $100K - $1M

What investors want: Strong founding team, credible problem, early signal (prototype, letters of intent, initial users)

Who invests: Friends and family, angels, pre-seed funds, accelerators

At pre-seed, you're selling the vision and the team. You probably don't have significant revenue. Investors are betting on you as a person and on the market opportunity.

Your pitch needs to answer: Why this? Why now? Why you?

Seed

Typical raise: $1M - $4M

What investors want: Product in market, early traction, some evidence of product-market fit

Who invests: Seed funds, angels, micro-VCs

Seed is where you prove the concept works. You have users, maybe early revenue, and data showing people actually want what you're building.

The narrative shifts from "here's our vision" to "here's what we've learned, here's what we know works, here's how we'll scale it."

Series A

Typical raise: $5M - $20M

What investors want: Repeatable growth, clear unit economics, evidence of scalability

Who invests: Institutional VC firms

Series A is a turning point. You're not just proving the product - you're proving the business. Investors want to see that you know how to grow efficiently and that the model works at scale.

Typical milestones before raising a Series A: $1-3M ARR (for SaaS), consistent month-over-month growth, healthy retention numbers.

Series B and beyond

Series B typical raise: $20M - $60M

Series C+: $60M+

At these stages, you're scaling what works. You're hiring aggressively, expanding into new markets, possibly acquiring competitors. The data needs to be very strong.

Most founders reading this guide are focused on pre-seed through Series A. That's where most of the tactical advice below applies.

Bridge rounds - what they are and when they make sense

A bridge round is a smaller financing round raised between two larger rounds. It's designed to extend your runway so you can hit milestones before raising the next primary round.

Bridge rounds are common. Don't treat them as a sign of failure. In 2024, bridge rounds using unpriced instruments accounted for roughly 16-17% of all venture capital raised - and that number has been growing.

You'd raise a bridge if:

- You're close to a major milestone but need a few more months of runway to get there

- The market timing isn't right for a full raise right now

- You want more traction before raising at a higher valuation

Bridge rounds are typically done on SAFEs or convertible notes, with existing investors participating. If your existing investors won't participate in a bridge, that's a signal worth paying attention to.

Be careful about stacking bridges. A company that's raised multiple bridges without a clear path to its next primary round can end up with a messy cap table and investor fatigue. If you're raising a second bridge, ask yourself honestly whether you're extending runway toward a milestone or just delaying an inevitable harder conversation.

Down rounds - what happens and how to handle them

A down round is when you raise capital at a valuation lower than your previous round. It happens. The market has cycles, and companies that raised at peak 2021 valuations have had to navigate this in subsequent years.

Down rounds are painful but survivable. The key is handling them correctly.

What a down round means in practice:

- Existing investors who have anti-dilution protection will get adjusted share prices. This can significantly dilute founders and common shareholders.

- Employee stock options may be underwater - the strike price is higher than the current share price - which can damage morale and retention.

- The narrative is hard. Raising at a down valuation is a public admission that the last valuation was too high.

If you're facing a down round:

Communicate with existing investors early. Don't let them find out when you're already deep in negotiations with a new investor. Get them aligned on the rationale.

Understand your anti-dilution provisions. Broad-based weighted average anti-dilution is standard. Full ratchet anti-dilution (which gives investors the full adjustment benefit) is much more punishing and should have been avoided in earlier term negotiations.

Consider whether a bridge round or venture debt could buy you enough time to raise a flat or up round instead.

If the down round is the right call, do it cleanly. Getting the capital you need to survive and grow is more important than protecting the optics of a valuation number.

Product-market fit - what investors are actually evaluating

Every investor at every stage is trying to answer one underlying question: does this company have product-market fit, or is it on a credible path to it?

Product-market fit (PMF) is when your product solves a real problem well enough that your customers are genuinely disappointed if they can't use it anymore. You feel it in retention numbers, in organic growth, in customers telling other people about you without being asked.

You don't need to have full PMF to raise pre-seed or seed. But you need to demonstrate that you're getting closer to it, and that you understand what signals you're looking for.

Signals that suggest PMF (or progress toward it):

- Net Promoter Score above 40+ for consumer, or strong referral behavior in B2B

- Low churn, especially cohort retention that stays flat rather than declining

- Customers who use the product multiple times per week without prompting

- Organic word-of-mouth acquisition without paid channels

- Users who ask for features that indicate deep, habitual engagement

Signals that suggest you're far from PMF - and that investors will notice:

- High churn in early cohorts

- Customers who signed up but rarely log in

- Needing heavy sales support to retain accounts

- Unclear who your core customer actually is

Being honest about where you are on the PMF journey - and having a clear thesis about how to get there - is more credible than claiming you already have it when you don't.

Accepting the right capital - why not all money is equal

When you're running low on runway, any check can look attractive. This is one of the most dangerous moments in a startup.

Misaligned capital is a real problem. Taking money from investors who don't understand your business, don't share your timeline, or have different exit expectations can create serious conflict down the line.

Before you accept any investment, be clear on:

Their portfolio and stage experience. Does this investor actually understand your sector? Have they backed similar companies before? Do they know what realistic growth looks like in your space?

Their time horizon. Early-stage VCs typically operate on 7-10 year fund cycles. Angels may have shorter or longer horizons. If you're building a 10-year company and your investor wants an exit in 3, that tension will surface.

Their value beyond capital. The best investors have networks, pattern recognition, and experience that genuinely helps. The worst ones take board seats and then have opinions about everything without adding anything.

Their communication style. Talk to other founders in their portfolio. Ask directly: what's it like when things go wrong? How do they show up when a company is struggling?

A smaller check from the right investor is worth more than a larger check from the wrong one. The wrong investors can slow you down, create dysfunction at the board level, and make future fundraising harder.

You have more leverage than you think when you're picking investors - especially if you've run a competitive process. Use it.

How to prepare for fundraising

Showing up to investor meetings unprepared wastes everyone's time and kills your chances. Here's what you need to have in place before you start.

Know your numbers

You need to know your metrics cold. If you're stumped by a basic question about your CAC, LTV, MRR, or churn rate, that's a red flag for investors.

Common metrics you'll be asked about:

- Monthly recurring revenue (MRR) or annual recurring revenue (ARR)

- Month-over-month growth rate

- Customer acquisition cost (CAC)

- Lifetime value (LTV) and the LTV:CAC ratio

- Gross margin

- Burn rate and runway

- Net revenue retention (NRR) or churn

You don't need perfect numbers. But you need to know what they are and why they are what they are.

Define your funding ask

Be specific. Know how much you're raising, at what valuation (or valuation cap for a SAFE), and what you'll do with the money.

"We're raising $2M to hire 3 engineers and 1 growth lead, giving us 18 months of runway to reach $1M ARR" is a coherent ask.

"We're raising some capital to grow" is not.

Investors want to understand how their money turns into the next milestone that justifies a future round at a higher valuation.

Build your target investor list

Don't cold pitch every VC you can find. Research who invests in your stage, your sector, and your geography. Read their investment theses. Look at their portfolios.

A targeted list of 30-50 right-fit investors is more effective than a spray-and-pray list of 200.

Tools to build your list: Crunchbase, Signal by NFX, Airtable investor databases shared in founder communities, LinkedIn.

Warm introductions are significantly more effective than cold outreach. Work your network. Ask portfolio founders to intro you to investors they have relationships with.

Create your pitch deck

Your pitch deck is usually the first thing an investor sees. It needs to be clear, concise, and compelling.

A standard pitch deck covers:

- Problem - what pain you're solving and for whom

- Solution - how your product solves it

- Market size - TAM/SAM/SOM, credibly calculated

- Product - screenshots, demo, how it works

- Traction - your best metrics and growth trajectory

- Business model - how you make money

- Competition - honest assessment of the landscape

- Team - why you're the people to do this

- Financials - 3-year projections (seed stage) or detailed model (Series A+)

- The ask - how much, at what terms, what it gets you

Keep it under 15 slides. Investors see hundreds of decks. Density and clarity matter more than design.

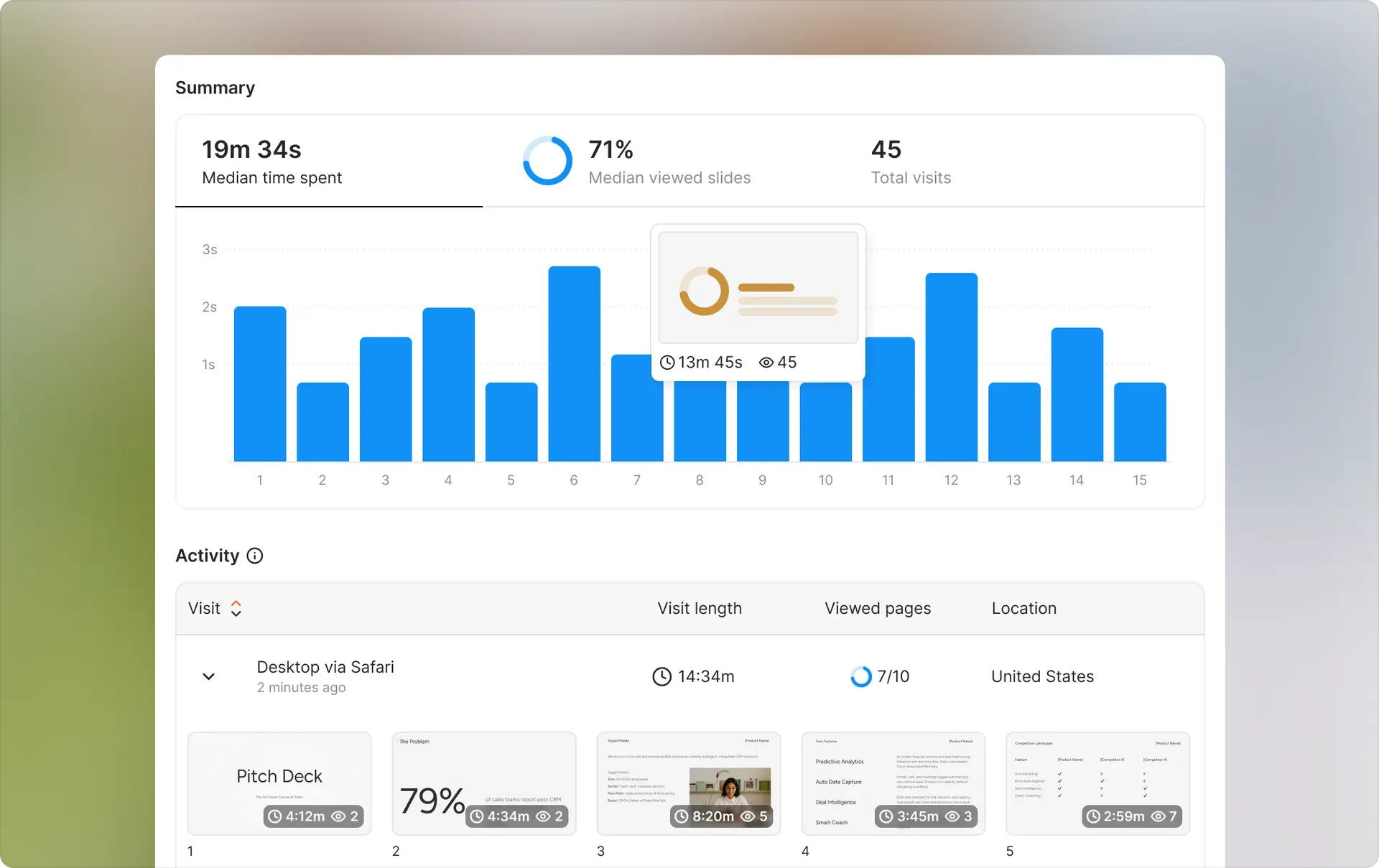

How to track investor engagement with your pitch deck

Sending your pitch deck as a PDF attachment and waiting to hear back is a dead end. You have no idea if it was opened, who read it, or which slides they spent time on.

This is where pitch deck analytics changes the game.

When you share your deck through a platform that gives you tracking data, you learn:

- Did the investor open the deck?

- How long did they spend on it?

- Which slides got the most attention?

- Did they share it with a partner?

- Did they come back to look at it again?

That information tells you a lot. If an investor spent 8 minutes on your traction slide and then forwarded the deck to two colleagues, that's a warm signal - follow up now. If they opened it for 20 seconds and never came back, that tells you something too.

Ellty is perfect for this. You upload your documents, create a trackable link, and share that link with investors. The platform shows you real-time analytics on who viewed the deck, how long they spent on each slide, and when they returned.

You get real-time notifications when someone opens your deck, so you can follow up at exactly the right moment instead of guessing.

Free forever for core tracking and analytics; Standard from $69/month with unlimited documents, eSignatures, and data rooms; Data Room from $149/month with granular permissions, NDA gating, and dynamic watermarking.

There's no per-user pricing, which matters when you're sharing with multiple investors across a round.

How to run a fundraising process

Fundraising is a process, not a series of one-off meetings. If you treat it like a process, you'll close faster and on better terms.

Run a tight timeline

Investors are more interested when they know others are looking. Creating real or perceived momentum matters.

The standard approach: batch your first meetings in a 2-3 week sprint. Get as many first meetings as possible in a short window. This creates parallel conversations and gives you leverage.

Don't drag it out over 6 months with one meeting per week.

First meeting: what to expect

The first meeting is usually 30-60 minutes. It's as much a relationship check as it is a business evaluation. Investors are assessing whether they want to work with you for 7-10 years.

Come prepared to walk through your deck, but don't make it a slideshow presentation. The best first meetings are conversations. Let them guide where they want to go deep.

Be honest about risks. Investors who've been doing this long enough will find the problems anyway. Founders who acknowledge risks proactively and have thoughtful responses build more trust.

Due diligence

If an investor is interested after the first meeting, they'll want to do diligence. This varies significantly by stage and firm, but typically includes:

- Reference calls on the founding team

- Deep dive on metrics and financial model

- Legal review (cap table, corporate docs, IP ownership)

- Customer or user interviews

- Product review or technical audit (for tech-heavy companies)

Early-stage diligence can be light - a few calls and a cap table review. Series A diligence can take weeks and involve multiple people at the firm.

You need to be organized and responsive. Slow diligence kills deals.

Negotiate the term sheet

A term sheet outlines the key economics and governance terms of the investment. It's not a final legal document, but it guides the definitive agreements.

Key terms to understand:

- Valuation/valuation cap - what price are they putting on the company

- Dilution - how much ownership are you giving up

- Pro-rata rights - investor's right to participate in future rounds

- Board seats - governance control

- Liquidation preference - who gets paid first in an exit

- Anti-dilution provisions - investor protection if you raise at a lower valuation later

Get a lawyer who specializes in startup financing. This is not the place to save money with a generalist.

SAFEs vs. convertible notes - what you're actually signing

You'll encounter these two instruments constantly at pre-seed and seed. They're both ways to take investment now without setting a firm valuation. But they're not the same thing.

SAFE (Simple Agreement for Future Equity)

A SAFE is not a debt instrument. There's no interest rate and no maturity date. The investor gives you money now, and in exchange, they get the right to convert that money into equity at a future priced round, at a discount or pre-set valuation cap.

SAFEs are faster and cheaper to execute than priced rounds. They've become the default instrument for pre-seed and seed in the US, largely because Y Combinator standardized the format.

There are two main flavors:

Pre-money SAFE: The valuation cap is calculated on a pre-money basis, meaning the SAFEs themselves are included in the denominator when calculating ownership. This can result in more dilution than founders expect when multiple SAFEs convert.

Post-money SAFE: The valuation cap is based on post-money valuation, so the founder knows exactly what percentage the investor will own at conversion. This is the current Y Combinator standard. It's more founder-friendly in terms of predictability.

When you have multiple SAFEs at different valuation caps outstanding, modeling what happens at conversion gets complicated fast. Use a SAFE calculator or dilution modeling tool before you stack too many.

Convertible note

A convertible note is debt that converts to equity. Unlike a SAFE, it carries an interest rate (typically 4-8%) and has a maturity date (usually 12-24 months). If the note hasn't converted by the maturity date and you haven't raised a priced round, you technically owe the money back - or you need to renegotiate the terms.

Convertible notes are more common when investors want some downside protection. They're slightly more complex and more expensive to execute than SAFEs.

Valuation cap and discount - what they mean

Both instruments typically include one or both of these terms:

Valuation cap: The maximum valuation at which the investor's money converts to equity. If you raise your Series A at a $20M valuation but your SAFE had a $10M cap, the investor converts as if the valuation was $10M - they get more shares than a new investor paying $20M.

Discount: A percentage reduction on the price per share at conversion. A 20% discount means the investor pays 80 cents for every dollar of stock price at the next round.

Caps and discounts reward early investors for taking more risk. They're standard and expected. Just model what they'll actually cost you before you issue them.

Priced rounds - what changes when you set a valuation

Eventually, your fundraising moves from unpriced instruments to a priced round. This typically happens at Series A, though some companies do a priced seed.

In a priced round, your company is assigned a specific valuation. That valuation determines the price per share for new investors, and everyone's ownership gets calculated against it. The lead investor receives preferred stock, not common stock.

Preferred stock comes with rights that common stock doesn't have:

- Liquidation preference: In an exit, preferred shareholders get paid before common shareholders, typically 1x their investment. This protects investors if the company sells for less than expected.

- Anti-dilution provisions: If you raise a future round at a lower valuation (a down round), anti-dilution clauses adjust the conversion price of the investor's preferred stock to protect them. Broad-based weighted average anti-dilution is the most common and most founder-friendly version.

- Pro-rata rights: The right to invest in future rounds to maintain their ownership percentage.

- Board representation: Lead investors at Series A and beyond often take a board seat.

These terms are negotiable - all of them. But you need to understand what each one means before you negotiate. Your startup lawyer should walk you through every term in the term sheet before you sign anything.

Your cap table - keep it clean from day one

Your cap table is the official record of who owns what in your company. Every share, every option grant, every convertible instrument, every investor - it's all on the cap table.

Investors look at your cap table during diligence. A messy one is a red flag. It signals disorganization, potential legal problems, and can slow down or kill a deal.

Common cap table problems that create real issues:

- Shares issued without proper documentation

- Missing 83(b) elections from early employees or founders

- SAFEs issued at multiple valuation caps without modeling the impact

- Informal equity promises made verbally without paperwork

- An ex-employee or advisor who still holds a significant chunk with no vesting cliff

Set up proper cap table software from day one. Tracking equity on a spreadsheet works until it doesn't, and by the time it doesn't, fixing it is expensive.

What happened here:

- The company issued 2.5M new preferred shares to the seed investor at $0.80/share

- Founder 1 and Founder 2 each went from 40% → 32% - that's the dilution

- The advisor went from 2% → 1.6%

- The option pool shrank proportionally as a percentage of the total

Key things to notice:

- Founders lost 8 percentage points each - not because anyone took shares from them, but because new shares were created

- The option pool didn't expand here - if the investor had required a top-up before closing, founders would have diluted further

- The seed investor holds preferred stock, not common - different rights, different protections

This is a clean cap table. Two founders, one advisor, one investor, one option pool. In reality, by the time you hit Series A, you may have 10–15 SAFEs converting, multiple option grants, and several investors - which is exactly why software beats a spreadsheet.

The pro forma cap table

Before you close any financing round, build a pro forma cap table. This is a forward-looking model showing what your cap table will look like after the deal closes - who owns what, what converted, and what new shares were issued.

Investors will review this before signing. You should have already reviewed it before you agreed to any terms.

At minimum, your pro forma should model: new investor shares, option pool expansion (if any), conversion of any outstanding SAFEs or convertible notes, and the resulting fully-diluted ownership breakdown.

If you have multiple SAFEs converting in the same round, the math gets complex. Model every scenario before you agree to terms.

How much to raise - and when to start

Two questions that don't get clear answers often enough.

How much to raise

The amount you raise should be determined by one thing: how much capital it takes to hit your next fundable milestone, plus enough buffer to handle things taking longer than expected.

Figure out the milestone first. What does "successful" look like in 12-18 months? What metric, if hit, makes your next raise easier and gives you leverage?

Then work backward: what does it cost to get there? Head count, infrastructure, marketing spend. Build a bottoms-up budget. Don't just pick a round size because it sounds right or because you read that "seed rounds are $2-3M."

Add 20-30% buffer. Things always take longer and cost more than planned.

Raise enough for 18 months of runway minimum. 24 months is better. Fundraising takes time and you don't want to be raising the next round with 3 months of cash left.

Don't over-raise either. Taking more money than you need at an early stage means more dilution at a valuation that's lower than it will be later. There's a real cost to raising more than you need.

When to start fundraising

The worst time to raise is when you're running out of money. That's negotiating from weakness. Investors know it. Terms will reflect it.

The best time to raise is when you have momentum - metrics are moving in the right direction, product is working, you don't desperately need the money but it would accelerate growth.

A rough signal for timing:

- Pre-seed: When you have a compelling team and a credible problem, with some early product signal

- Seed: When you have early traction and product in market

- Series A: When you have repeatable growth and clear unit economics

Start building relationships 6-12 months before you want to close a round. Investors who've been watching you hit milestones quarter after quarter are much more likely to say yes than investors meeting you for the first time at a pitch.

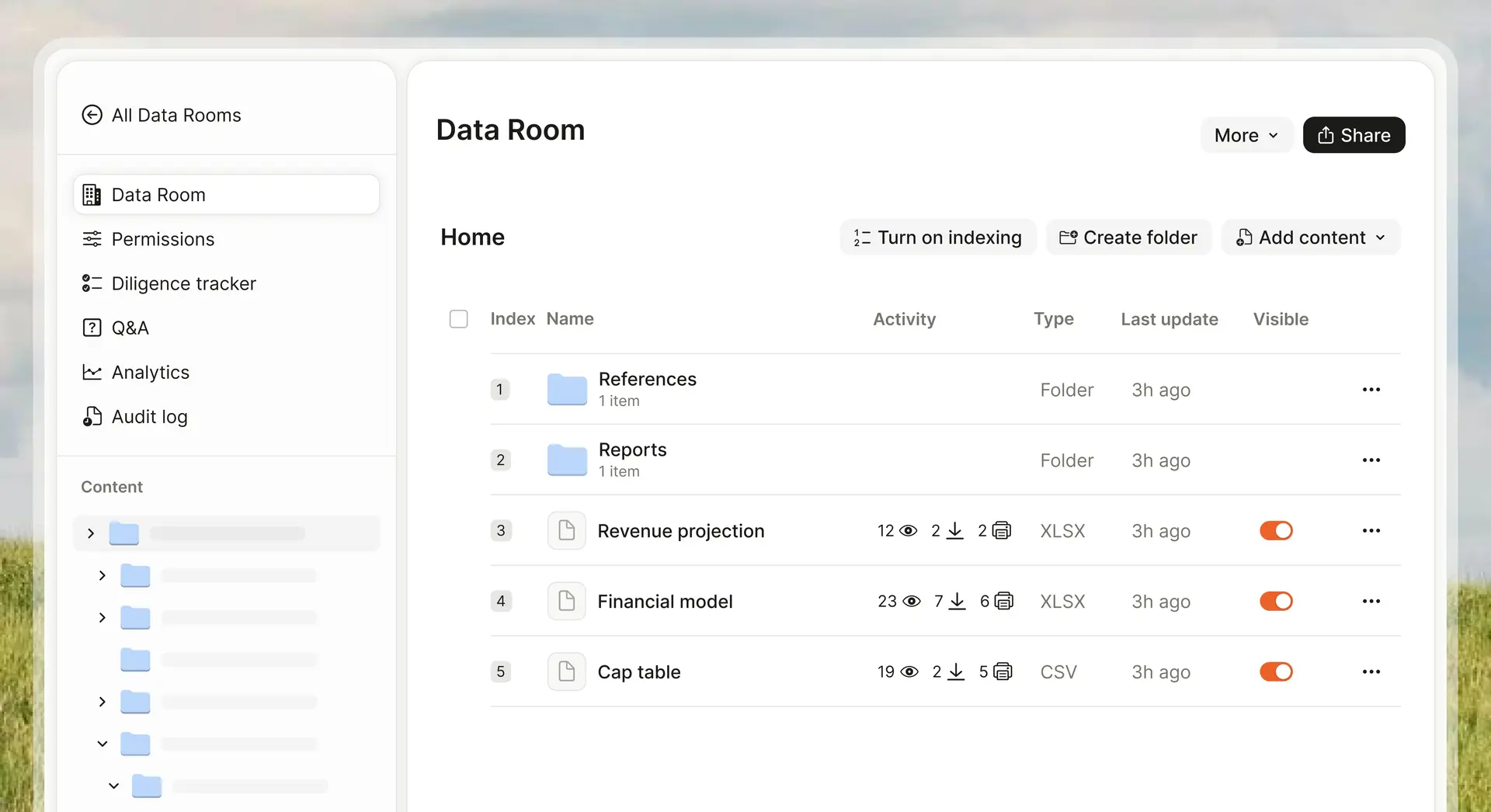

How to run due diligence - the data room

Once a serious investor is engaged, they'll want to review materials beyond the pitch deck. This is where a data room comes in.

A data room is a secure, organized folder of documents that you share with investors during diligence. Having one ready before you need it signals that you're organized and serious.

What goes in a data room

Company and legal

- Certificate of incorporation

- Cap table (fully diluted)

- Shareholder agreements

- Board minutes

- IP assignments and NDAs

Financials

- Historical P&L and balance sheet

- Monthly financial model

- Revenue breakdown by customer or segment

- Burn rate and cash flow projections

Product

- Product roadmap

- Key metrics dashboard

- Customer contracts or LOIs

Team

- Org chart

- Key employee agreements

- Founder backgrounds

Market and strategy

- Competitive analysis

- Market research

- Go-to-market strategy

Controlling access to your data room

Not all investors get access to everything at once. Early in the conversation, you share a limited set of materials. As diligence progresses, you grant access to more sensitive documents.

You also want to know who's looking at what. If a document is downloaded and then turns up at a competitor, you want to know where it came from.

This is where a virtual data room (VDR) earns its value. Traditional VDRs from providers like Intralinks or Ansarada are expensive - often several thousand dollars per deal, with per-user fees that add up fast.

Ellty offers data room features without the per-user pricing model. You can upload your documents, create controlled access links, set permissions, and see analytics on who viewed which files and when. For teams running their first diligence process, this covers most of what you need without the enterprise pricing.

The Standard plan at $69/month gives you the data room functionality, professional document sharing, eSignatures, and detailed investor engagement data under one roof. That's a significant difference from paying $2,000-$5,000 for a traditional VDR on a deal that may or may not close.

That said, if you're raising a large Series B or later round with complex legal requirements, institutional-grade VDRs may offer compliance features that matter at that scale.

How to think about your fundraising pipeline

Fundraising is a sales funnel. Treat it like one.

You have a pool of potential investors. Some will take a first meeting. Some of those will want to go deeper. A smaller number will give you a term sheet. A subset of those will close.

The conversion rates are brutal at every stage. Expect them to be. A realistic funnel for a seed round might look like:

- 50-80 investors contacted

- 20-30 first meetings

- 8-12 who want to dig deeper

- 3-5 who are seriously interested

- 1-2 term sheets

- 1 lead who closes

That math means you need top-of-funnel volume. You can't run a 10-investor process and expect to close. Build the list, work the network, run the meetings.

Track every interaction. Know where every investor is in the process. Follow up consistently. When one investor shows strong interest, use that to create urgency with others.

The moment you have a term sheet - even one you might not want - the whole dynamic changes. Other investors who were slow-walking the process suddenly get moving. A term sheet creates real or perceived scarcity. That's not a trick; it's just how competitive processes work.

Don't let investors string you along indefinitely. If someone has been "very interested" for 6 weeks and keeps asking for more information without making a decision, ask them directly: are you in a position to move forward in the next 2 weeks? The answer will tell you whether to keep investing time in the relationship.

Common mistakes founders make when fundraising

Learning from other people's mistakes is faster than making your own.

Raising too early

Investors invest in de-risked bets. Every milestone you hit before you raise - more customers, more revenue, more product validation - makes you a less risky bet, which means better terms and less dilution.

The temptation is to raise as soon as possible. Resist it if you can keep the lights on.

Talking to the wrong investors

Pitching a growth-stage VC when you're pre-revenue wastes both of your time. Do your research. Know who invests at your stage.

Underpricing the round

Being overly conservative about valuation can hurt you. Under-pricing means more dilution. It also signals that you don't fully believe in what you're building. Know what comparable companies at your stage have raised at and calibrate accordingly.

Overpricing the round

The flip side: setting an unrealistic valuation means either you won't close or you'll create a down round problem later. Talk to advisors and other founders to calibrate.

Not following up

Investors are busy and easily distracted. If you had a good meeting and you're waiting for them to come back to you, they probably won't. Follow up. Share an update. Create a reason to stay in conversation.

Neglecting existing investors

If you have angels or seed investors, keep them updated throughout the process. They're part of your network and can make introductions. They'll be more supportive if they feel included.

Ignoring the legal structure

How your company is structured (Delaware C-Corp vs. LLC vs. S-Corp) matters for fundraising. Most institutional VCs won't invest in LLCs. If you're not already a Delaware C-Corp, get that sorted before you start pitching.

How to pitch well

Pitching is a skill. It gets better with practice.

Tell a story

Data without narrative is just numbers. The best pitches connect the dots between the problem, the solution, the team, and the market in a way that feels inevitable.

Start with the problem. Make the investor feel it. Then show how your solution specifically addresses it.

Be direct about risks

Every business has risks. Investors know this. If you pretend yours doesn't have any, you lose credibility. Identify the top 2-3 risks yourself, and be ready to explain how you're mitigating them.

Know your competition honestly

"We have no competitors" is almost always wrong and always a red flag. Show that you understand the landscape. Explain why you're positioned to win in a specific way.

Practice with people who'll push back

Don't just practice with your co-founder who'll nod and agree. Find advisors, experienced founders, or even friendly investors who'll ask tough questions and poke holes in your story.

Follow up with something useful

After a meeting, don't just send a thank-you email. Send something that adds value - a new customer win, a key metric update, an article relevant to something you discussed. Give them a reason to open your email.

Building investor relationships before you raise

The best time to start building relationships with investors is before you need money.

Follow investors whose work you respect. Read their writing. Comment thoughtfully on their content. Attend events where they speak. Build a relationship so that when you do reach out with a pitch, it's not cold.

Many investors are more likely to take a meeting with someone they've interacted with over time than with a cold email, no matter how polished.

If you're not in a position to raise right now, you can still send short update emails to investors you've met: "Thought you'd find it useful to know we hit $50K MRR last month. Would love to reconnect in Q3 when we're ready to raise." That's not annoying. That's smart.

How to handle a no

Most pitches end in a no. That's not failure - it's the process.

When you get a no, try to get a specific reason. "It's not a fit right now" is not useful. Ask: "Is it a stage issue, a market issue, or something specific to the business?" If they'll tell you, that's valuable information.

Don't burn bridges. The VC who passes today may introduce you to someone who invests. The one who passes on your seed might be right for your Series A. Stay professional.

Keep a record of every conversation, every feedback point, and every follow-up. Treat it like a sales process - because it is.

After you close the round

Closing a round feels like the finish line. It's not. It's the starting gun.

Send a proper announcement

Update your team, your advisors, and your network. A round announcement on LinkedIn or a press release can drive inbound attention from future investors, talent, and customers.

Update your cap table immediately

Get your equity management sorted (Carta, Pulley, or similar) so your cap table stays clean. This will matter at every future round.

Establish reporting cadence with investors

Set up a regular investor update - monthly for most early-stage companies. Keep it short: what's working, what's not, what you need. Investors who are informed are more likely to help when you need it.

Start thinking about the next round

What are the milestones that will make your next raise easier? Define them now. Every decision you make about how to deploy capital should be oriented toward hitting those milestones.

How Ellty fits into your fundraising process

Fundraising generates a lot of document sharing. Pitch decks go out to dozens of investors. Data room materials go to the ones who are serious. Keeping track of who has what - and who's actually engaging with it - is a real operational challenge.

Ellty is designed to solve that specific problem without the complexity or cost of enterprise software.

Pitch deck sharing: Upload your deck, create a trackable link, share with investors. You'll know when they open it, how long they look at each slide, and if they come back. Real-time notifications mean you can follow up when the iron is hot.

Data room: For diligence, you can upload multiple documents, control who has access, set permissions, and monitor viewing activity. No per-user fees means you're not watching the meter as more stakeholders join the process.

Pricing:

- Free: $0 - document tracking, real-time analytics, secure links, 10 GB storage, free forever

- Standard: $69/month - unlimited documents, eSignatures, full data room functionality, advanced analytics, custom branding

- Data Room: $149/month - granular permissions, NDA gating, dynamic watermarking, restricted visitor access, 3 users included

- Data Room Plus: $349/month - group visitor permissions, audit logs, 4,000 assets per data room

You won't need an enterprise contract or a procurement process to get started. Setup takes minutes, not days.

Ellty works well for teams running their fundraise who want professional-grade pitch tracking and data room functionality without paying for features they don't need.

FAQ: how to raise funding

Q: How long does it take to raise a seed round?

A: On average, 3-6 months from the time you start actively pitching to the time money hits the bank. That includes finding the lead investor, negotiating terms, and completing legal docs. Some founders close in 6 weeks. Others take 9 months. Having your materials ready before you start significantly compresses the timeline.

Q: How much equity should I give up at seed?

A: Most seed rounds dilute founders by 15-25%. If you're giving up more than 25% at seed, think carefully about whether the terms are reasonable or whether you're undervaluing the company. The goal is to have enough equity left to motivate the team and give yourself room for future rounds.

Q: Do I need a warm introduction to get a VC meeting?

A: Not always, but it helps a lot. Most top-tier VCs get hundreds of cold pitches per month. A warm intro from someone they respect moves you to the top of the pile. That said, some investors do read cold pitches - especially those with a strong online presence or open application processes (like YC).

Q: What's a SAFE and should I use one?

A: A SAFE (Simple Agreement for Future Equity) is a convertible instrument that lets investors put money in now and convert to equity at a future priced round. It was invented by Y Combinator and has become standard for pre-seed and seed deals. It's simpler and cheaper than a priced round. Most early-stage founders should use SAFEs unless there's a specific reason to do a priced round.

Q: What's the difference between pre-money and post-money valuation?

A: Pre-money valuation is what the company is worth before the investment. Post-money is the pre-money valuation plus the new investment. If you raise $2M at a $8M pre-money valuation, the post-money is $10M, and the investor owns 20%. This matters for calculating dilution. Post-money SAFEs (the current Y Combinator standard) fix the valuation cap on a post-money basis, which makes dilution easier to calculate upfront.

Q: How do I know if my valuation is too high or too low?

A: Research comparable companies at your stage - similar industry, similar metrics, similar market. Platforms like Crunchbase and PitchBook (if you have access) show historical round data. Talk to other founders who recently raised. Advisors and angels familiar with your sector can give you a calibrated range. No formula is perfect, but being within the market range is the goal.

Q: Should I use a pitch deck template?

A: A template is a fine starting point, but your deck needs to tell your specific story. Generic templates often lead to generic decks. The structure matters (problem, solution, market, traction, team, ask) but how you fill each section is where the work is. Don't let a template constrain what needs to be communicated.

Q: How do I run due diligence if I've never done it before?

A: Start by building your data room before you need it. Get your corporate docs, cap table, financial model, and key contracts organized. When an investor asks for diligence materials, you send them a controlled link - not a Dropbox folder with 47 disorganized files. Tools like Ellty let you do this without enterprise pricing. As the process gets more advanced, work closely with your lawyer, who will help you understand what you need to produce and what's reasonable to share at each stage.

Q: Do I need to raise VC funding?

A: No. VC is one path. It's the right path for businesses that need large amounts of capital to grow fast and have the potential to become very large companies. It's not right for every business. Revenue-based financing, bootstrapping, angels, grants, and crowdfunding are all legitimate alternatives depending on your business model and growth goals. Raise from VCs if and when their incentives align with yours.

Q: What should go in investor updates after I close the round?

A: Keep it short and consistent. Monthly is standard for early-stage. Cover: MRR/ARR and growth rate, burn and runway, top 3 wins, top 3 challenges, and one specific ask if you need help. Investors who get regular honest updates are more likely to make introductions, open doors, and come back for the next round. Don't make it a highlight reel - they'll see through it. Be honest about what's hard.

Wrapping up

Raising funding is hard. It takes longer than you think, there are more nos than yeses, and the process is opaque in ways that are genuinely frustrating for first-time founders.

But it's also learnable. The mechanics are not complicated. The tactics in this guide are used by founders at every stage, at every kind of company. None of this is secret.

What separates the founders who close is preparation, persistence, and process. Know your numbers. Build the right relationships early. Run a tight process when you're actively fundraising. Be honest with investors and with yourself.

The rest is execution.

If you're in the middle of a raise and want to track who's actually reading your deck, Ellty offers a free plan to get started - no credit card, setup in a few minutes. When you're ready for diligence, the Business plan at $50/month covers data room features without the per-user fees that make traditional VDRs expensive.

Good luck.

Author

Anika Tabassum Nionta is a Content Manager at Ellty, where she writes about secure document sharing, virtual data rooms, M&A, due diligence, fundraising, and sales enablement. With over 6 years of writing experience, she helps professionals understand how to share confidential documents securely, track engagement, and manage deals more effectively. Anika holds both a BA and MA in English from Dhaka University. Outside of work, she enjoys reading, exploring new cafes in Dhaka, and connecting with entrepreneurs and dealmakers in her community.