You got a term sheet. Congratulations - that's real progress. Now comes the part most founders aren't fully ready for: understanding what's actually in it.

Term sheets aren't designed to be founder-friendly. They're written by lawyers, for investors. Most of the language is standard - but "standard" doesn't mean harmless. A few clauses can quietly shift control, dilute you faster than expected, or limit your options in future rounds.

This guide gives you a practical term sheet template you can reference, breaks down every major clause in plain language, and tells you what to watch out for before you sign.

What a term sheet actually is

A term sheet is a non-binding document that outlines the basic terms of an investment deal. It's not the final contract - that comes later in the form of a stock purchase agreement and related legal docs. But the term sheet sets the framework for everything that follows.

Most of what you negotiate happens at the term sheet stage. Once it's signed and you move into legal drafting, changes become expensive and slow. So don't treat the term sheet as a formality. Treat it like the deal itself.

Core structure of a term sheet template

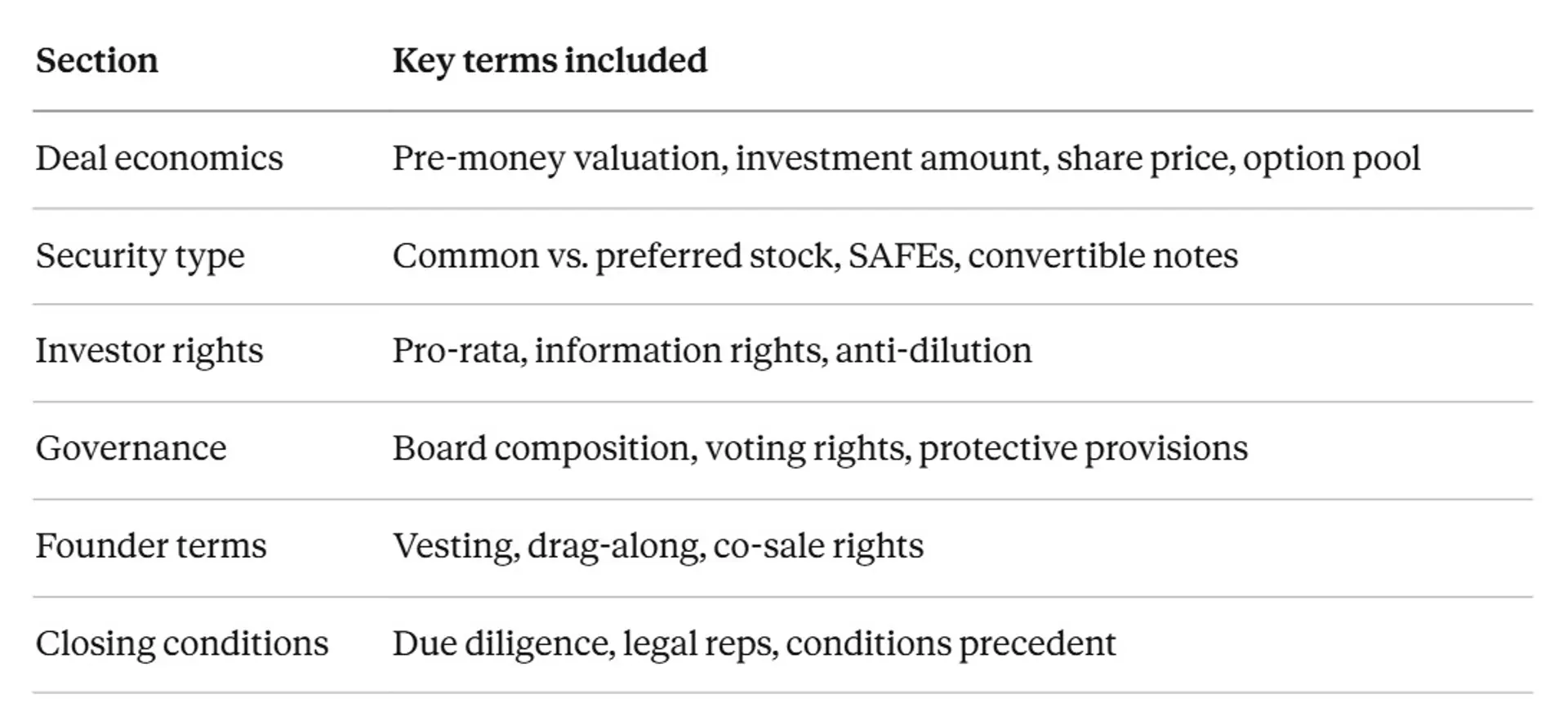

A standard term sheet template covers four main areas:

1. Deal economics - How much money, at what valuation, and in what form.

2. Investor rights - What the investor gets beyond just shares.

3. Governance - Who controls what, and how decisions get made.

4. Legal/closing conditions - What needs to happen before the deal closes.

Here's a high-level view:

Full term sheet template (annotated)

Below is a simplified but representative term sheet template you can use as a starting reference. Real term sheets from VC firms (especially Y Combinator's standard documents) will be more detailed - but this covers the core structure.

TERM SHEET

Company: [Company Name], Inc.

Date: [Date]

Investors: [Lead Investor Name], [Other Investors]

Type of Financing: Series [A/B/Seed] Preferred Stock

Section 1: Offering terms

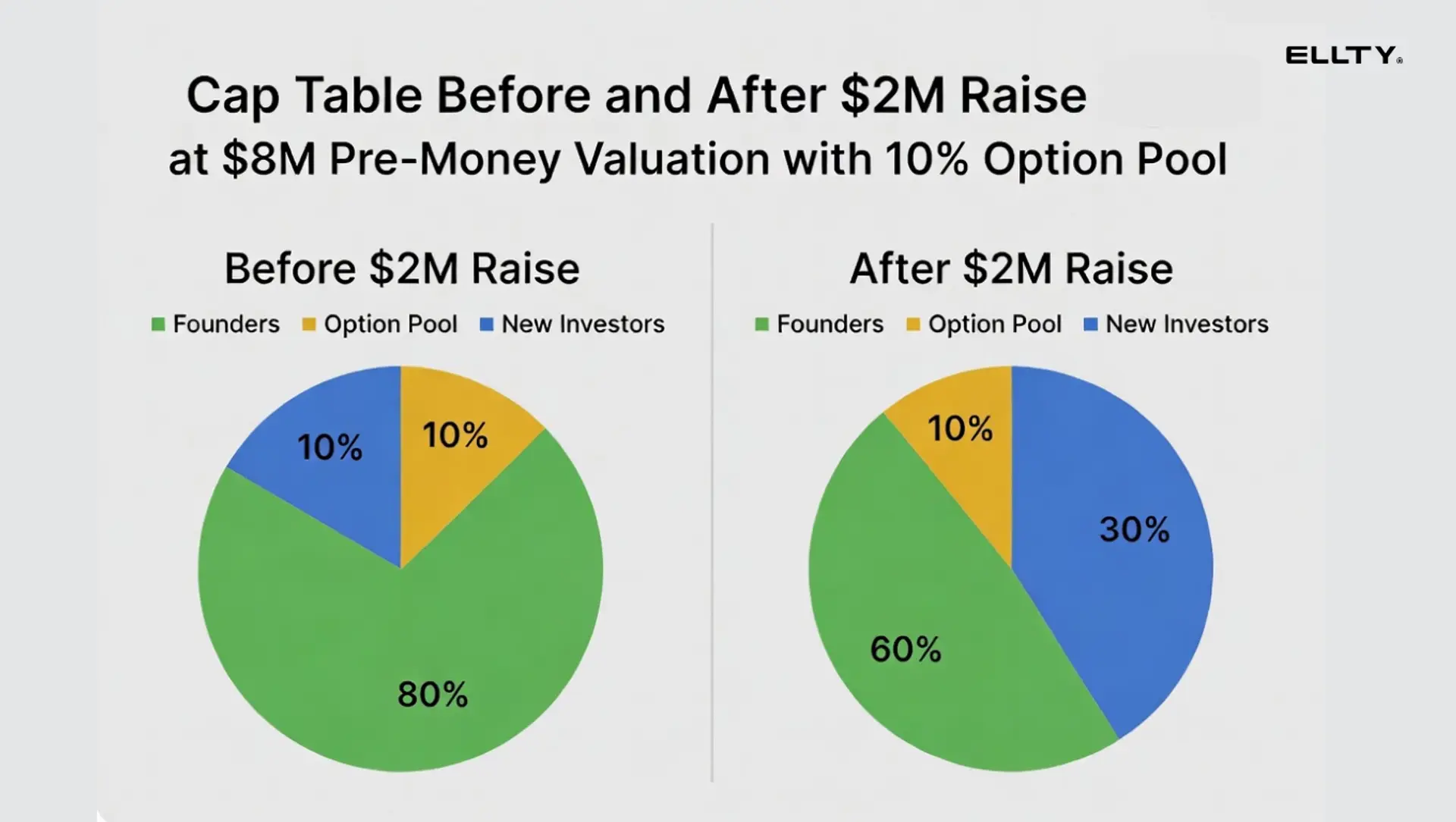

Pre-money valuation: $[X]M

This is the company's valuation before the new money goes in. If you raise $2M on a $8M pre-money, your post-money is $10M and the investor owns 20%.

Amount raised: $[X]M

Post-money valuation: $[X]M (pre-money + amount raised)

Price per share: $[X] (post-money valuation / fully diluted shares)

Option pool: [X]% of post-money fully diluted capitalization

Watch this carefully. Investors often require the option pool to be created before the investment, which dilutes founders - not investors. If they want a 15% option pool, make sure you understand what that does to your ownership.

Section 2: Type of security

Security: Series [A] Preferred Stock

Liquidation preference: 1x non-participating preferred

This is one of the most important clauses. Here's what it means:

- 1x non-participating: Investors get their money back first (1x the investment), then convert to common and share with founders. This is founder-friendly.

- 1x participating: Investors get their money back first AND share in the remaining proceeds. This is less founder-friendly.

- 2x or higher: Investors get 2x their money back before anyone else sees a dollar. Avoid this if you can.

Conversion: Preferred stock converts to common stock 1:1 at investor's option, or automatically at qualified IPO.

Dividends: [Cumulative at X% per year / Non-cumulative / None]

Non-cumulative or no dividends is the standard for early-stage deals. Cumulative dividends can add up fast.

Section 3: Valuation protection

Anti-dilution: Broad-based weighted average

Anti-dilution protects investors if you raise at a lower valuation in the future (a "down round"). There are two types:

- Broad-based weighted average: Takes into account all dilutive securities. More founder-friendly.

- Narrow-based weighted average: Only considers certain shares. Less founder-friendly.

- Full ratchet: If you raise at any lower price, investors reprice to that lower price. Very aggressive - rare in modern deals, but avoid it.

Section 4: Investor rights

Pro-rata rights: Investors have the right to participate in future financing rounds to maintain their ownership percentage.

This is standard and usually fine. Just know what you're agreeing to - in later rounds, investors with pro-rata can get complicated.

Information rights: Company will deliver audited annual financials within 90 days, unaudited quarterly financials within 45 days.

Inspection rights: Investors may inspect books and records at reasonable times.

Board of directors: Board will consist of [X] members: [X] Common Directors (founders), [X] Preferred Directors (investors), [X] Independent Director(s).

Board composition matters a lot. You want to keep a majority or at least parity as long as possible.

Section 5: Protective provisions

Investors get veto rights over certain actions, including:

- Amendments to the charter or bylaws

- Issuing new preferred stock

- Declaring dividends

- Changing the size of the board

- Selling the company

This is standard. Just make sure the list isn't unusually long or restrictive.

Section 6: Founder terms

Founder vesting: [X]-year vesting schedule, [X]-month cliff, [X]% already vested.

Standard is 4 years with a 1-year cliff. If you've been building for 2 years already, you can negotiate to have some already vested (called "acceleration credit").

Single vs. double trigger acceleration:

- Single trigger: Your shares accelerate if the company is acquired.

- Double trigger: Your shares accelerate only if the company is acquired AND you're fired or leave for good reason.

Investors usually prefer double trigger. You can negotiate for single trigger, but double trigger is a fair compromise.

Right of first refusal (ROFR): Company and/or investors have the right to buy your shares before you sell to a third party.

Co-sale rights (tag-along): If founders sell shares, investors can sell a proportional amount alongside them.

Drag-along: If a majority of shareholders vote to sell the company, all shareholders must sell.

Section 7: Closing conditions

Conditions to close: Legal due diligence, no material adverse change, standard reps and warranties, stock purchase agreement, investor rights agreement, voting agreement.

Exclusivity: Company agrees not to solicit or discuss other financing for [X] days.

Exclusivity periods are usually 30-60 days. Don't agree to more than 60 days - it ties your hands unnecessarily.

The clauses that actually matter most

You can't negotiate everything. These are the ones worth spending time on:

1. Pre-money valuation - Sets your dilution. Know your number before you enter a conversation.

2. Liquidation preference - Go for 1x non-participating. It's the market standard at seed and Series A.

3. Option pool - Understand whether it's being created before or after investment. Before = founder dilution.

4. Board composition - Don't give away board control in your first round if you can avoid it.

5. Anti-dilution - Broad-based weighted average is standard and reasonable. Anything else, push back.

6. Exclusivity period - 30-45 days is fine. Beyond 60 days, negotiate.

Common mistakes founders make with term sheets

1. Focusing only on valuation

Valuation gets all the attention, but a 1x participating liquidation preference or an oversized option pool can quietly cost you more than a slightly lower valuation. Read the full document.

2. Not modeling the cap table

Before you sign, model out what your ownership looks like at the current round, then at a Series A, then at an exit. You need to see the numbers. Tools like Carta or even a basic spreadsheet work fine.

3. Signing under time pressure

Investors sometimes create urgency. "We need this signed by Friday." Don't let that rush you into skipping legal review. A good lawyer can review a term sheet in 24-48 hours. Spend the money.

4. Not asking about reserves

Ask your lead investor how much they're reserving for follow-on. If they're putting in $500K now but have no reserve for your next round, that's worth knowing.

5. Ignoring the no-shop clause

Once you sign the term sheet, you often can't talk to other investors for the exclusivity period. Make sure you actually want to close with this investor before you sign and pause all other conversations.

6. Assuming "standard" means fair

Investors will say "this is all standard." Some of it is. Some of it isn't. Know the difference, or hire someone who does.

Due diligence: what happens after the term sheet

After you sign the term sheet, the investor starts due diligence. This is where deals slow down - or fall apart.

What they'll typically want to see:

- Cap table and corporate documents

- Financial statements (historical + projections)

- Key customer contracts

- IP ownership and assignments

- Employee agreements and equity grants

- Any outstanding legal disputes or liabilities

- Product demos or technical documentation

This is where having a virtual data room matters. Sharing files over email or Google Drive is messy and unsecure. You lose track of who's seen what. Investors get confused. Deals slow down.

A data room gives you a single, organized place to share everything - with full control over access.

How Ellty helps you manage due diligence without the complexity

Once you hit the due diligence stage, you need to share sensitive documents securely - and know who's actually reading them.

Ellty is a virtual data room, and secure file sharing platform built for businesses who don't want to overpay for enterprise software they'll use for 60 days.

Here's what you get:

- Upload pitch decks and docs - Share a trackable link, not an email attachment.

- See who viewed what - Know which pages investors spent time on, which they skipped, and when they viewed.

- Real-time notifications - Get notified the moment someone opens your deck or data room.

- Secure data rooms - Control access to sensitive due diligence documents. No per-user pricing surprises.

Ellty pricing: Free forever for core tracking and analytics; Standard from $69/month with unlimited documents, eSignatures, and data rooms; Data Room from $149/month with granular permissions, NDA gating, and dynamic watermarking.

Ellty works well when you're running a seed or Series C fundraise, need to share docs with multiple investors simultaneously, and want visibility into investor engagement without paying for a platform designed for 10,000-employee companies.

A quick note on SAFE vs. priced round term sheets

Not every early-stage deal uses a term sheet in the traditional sense. YC's SAFE (Simple Agreement for Future Equity) is designed to skip most of the complexity.

The differences:

If you're raising a SAFE, your "term sheet" is essentially just the SAFE document with a valuation cap and/or discount rate. Much simpler. Much faster. Worth considering for early rounds.

FAQ: term sheet questions founders actually ask

Q: Is a term sheet legally binding?

Mostly no. The deal terms themselves aren't binding - you can still walk away. But some provisions usually are binding: the no-shop/exclusivity clause, confidentiality, and any break-up fees if included. Read those sections carefully.

Q: How long does it take to go from term sheet to close?

Typically 4-8 weeks for a priced round. SAFEs can close faster - sometimes 1-2 weeks. Due diligence is usually the bottleneck.

Q: Should I hire a lawyer to review a term sheet?

Yes. A startup lawyer who does this regularly can review a term sheet in a day and flag anything unusual. Expect to pay $1,500-$3,000 for a review. It's worth it.

Q: Can I negotiate a term sheet?

Yes, and you should. Valuation, option pool sizing, board composition, and liquidation preference are all negotiable. How much leverage you have depends on how much competition there is for the deal and how badly the investor wants in.

Q: What's the difference between pre-money and post-money valuation?

Pre-money is what the company is worth before the investment. Post-money = pre-money + investment amount. If a VC invests $2M at an $8M pre-money valuation, the post-money is $10M and they own 20%.

Q: What's a "fully diluted" cap table?

Fully diluted means counting all shares that could exist, including issued shares, option pools, warrants, and convertible notes. Investors almost always calculate ownership on a fully diluted basis.

Q: What happens to my term sheet if the investor does due diligence and finds something they don't like?

They can walk away or renegotiate the terms. This is why it's important to be transparent upfront. Surprises in due diligence kill deals or create bad relationships with your investor.

Q: What's a down round, and why does it matter?

A down round is when you raise at a lower valuation than your previous round. It triggers anti-dilution protections for previous investors, which dilutes founders and existing common shareholders. It also signals distress - avoid if possible.

Q: Do I need a term sheet for a SAFE investment?

Not necessarily. SAFEs are simple enough that many founders just sign the SAFE directly without a separate term sheet. But some investors still send a brief term sheet first. Either approach is fine.

Q: What should I do before sending investors my due diligence documents?

Organize everything into a secure data room. Don't email sensitive files. Make sure you know who has access to what. Track engagement so you know which investors are serious. That's exactly what Ellty is built for.

Wrapping up

A term sheet is your first real negotiation with an investor. It sets the tone for the entire relationship that follows.

Don't be intimidated by it - but don't be casual about it either. Understand every clause. Model your cap table. Get legal advice. And when due diligence starts, have your documents organized and ready.

The founders who raise fastest aren't the ones with the best pitch. They're the ones who are prepared.

Ready to run a cleaner fundraise?

Ellty helps you share confidential documents, track investor engagement, and manage due diligence docs in one place - starting at $0.

This guide is for informational purposes only and does not constitute legal or financial advice. Always consult a qualified startup attorney before signing any investment documents.

Author

Anika Tabassum Nionta is a Content Manager at Ellty, where she writes about secure document sharing, virtual data rooms, M&A, due diligence, fundraising, and sales enablement. With over 6 years of writing experience, she helps professionals understand how to share confidential documents securely, track engagement, and manage deals more effectively. Anika holds both a BA and MA in English from Dhaka University. Outside of work, she enjoys reading, exploring new cafes in Dhaka, and connecting with entrepreneurs and dealmakers in her community.